Swipe card, scan QR? Buying on UPI may be about to get cheaper

Credit card payments involve MDR, which UPI does not. If the plans go through, the UPI user will pay ₹98, while the credit card user pays ₹100, implying a ₹2 discount for the former.

Scanning that UPI code to make a purchase may become cheaper than swiping your credit card, if a consumer affairs ministry effort on payment transaction fees bears fruit.

The government is working on a plan that will pass on the cost benefits of its popular unified payments interface (UPI) to consumers and incentivize its use in one go, three people familiar with the discussions said. Ministry officials will soon meet industry stakeholders to take the plan forward, one of the three people said on the condition of anonymity.

Every time a credit card is swiped, the merchant pays a fee of 2-3% to the bank and a payment gateway such as Visa or MasterCard, called the merchant discount rate (MDR). Most merchants do not pass on the fee to the customer, but absorb it themselves.

To illustrate, in a ₹100 credit card payment, the merchant keeps ₹98, and passes on ₹2 as MDR. In UPI, the merchant retains the entire ₹100, since UPI has no MDR. The disparity is stark in e-commerce platforms, which charge the same amount regardless of payment mode. At retail outlets, while most merchants absorb MDR, some pass it on to customers.

Also read: Govt approves 187 startups for tax exemption under revamped Section 80-IAC framework

If the plans go through, the UPI user will pay ₹98, while the credit card user pays ₹100, implying a ₹2 discount for the former.

The ministry will consult e-commerce leaders, banking service providers, National Payments Corp. of India (NPCI), Department of Financial Services (DFS), consumer groups and others before finalizing the way forward, the third person added. Plans are still early and more details are expected after the stakeholders' meeting likely in June, this person said.

Queries emailed to the consumer affairs ministry remained unanswered.

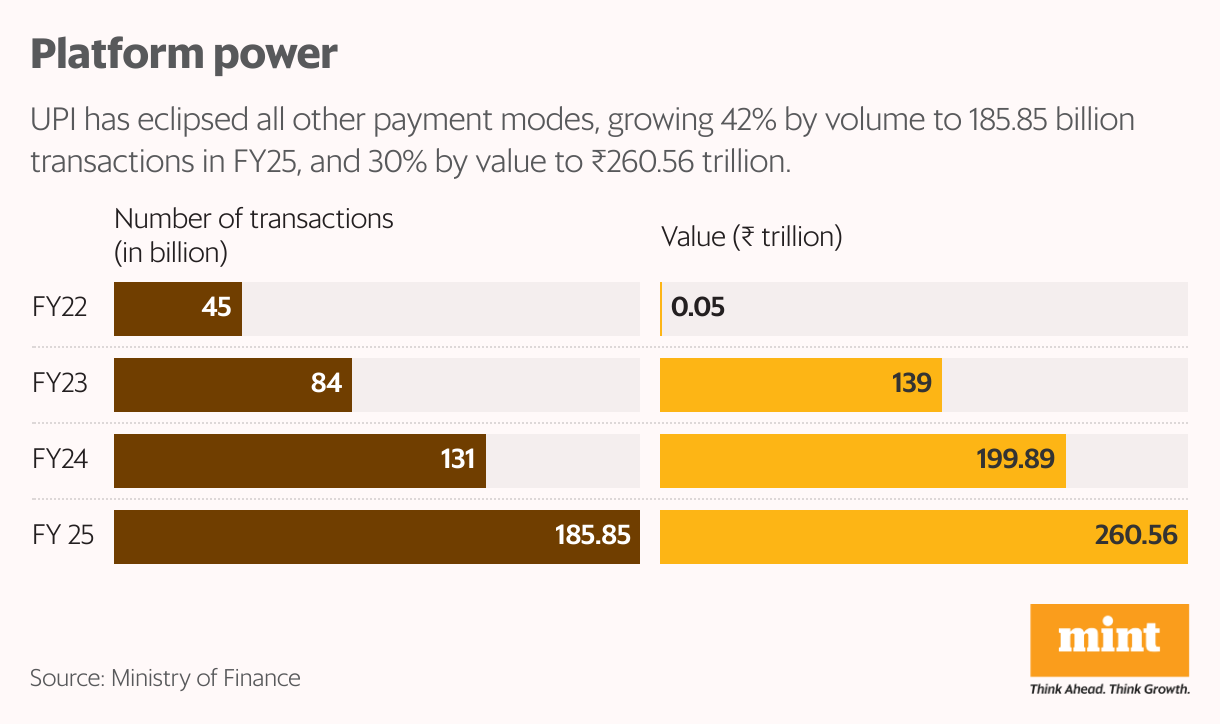

The radical plan comes at a time UPI has eclipsed all other payment modes, growing 42% by volume to 185.85 billion transactions in FY25, and 30% by value to ₹260.56 trillion. Between FY20 and FY25, UPI transaction volumes expanded at a compound annual growth rate (CAGR) of 72%. Between FY22 and FY25, about 260 million new users and 55 million new merchants joined UPI platform. Around 450 million used UPI in 2024.

Industry experts said the move opens space for more nuanced pricing. Vivek Iyer, partner and financial services risk leader at Grant Thornton Bharat, said, “Market infrastructure initiatives like UPI have democratized payments because of zero MDR. But other channels that incur costs and offer better customer experience can still justify MDRs. Differential pricing should be possible, especially when better service or personalization is part of the offer."

Also read: India could use Apple’s exit to spur hi-tech manufacturing push: GTRI

Iyer added that e-commerce platforms can adopt a layered strategy. “For luxury purchases, the choice of payment channel may not affect buyer behaviour, but for regular purchases, price sensitivity is much higher. So, there’s scope to design differentiated offerings around that."

He emphasized that zero MDR on UPI should continue, given its broader economic impact. “UPI enables the inclusion of many commercial activities in the formal economy. It serves a national interest and should remain focused on that goal for a few more years."

With countries like Singapore, the UAE and France showing interest in adopting UPI, those involved believe that aligning domestic policy to reflect its cost advantages for consumers could strengthen India’s digital public infrastructure and cement its leadership in inclusive fintech innovation.

“Consumers currently pay the same whether they use a card or UPI, despite the cost structure being different," said the second person, who is involved in the discussions. “If UPI is cheaper and simpler, we are looking at ways to make that benefit visible to users."

Business owners typically negotiate MDR charges before signing up for card swipe machines, based on the transaction value they expect from customers. High MDR is one of the primary reasons merchants prefer UPI to card-based payments.

“The move will definitely benefit consumers greatly. They would be rewarded for using UPI as their mode of payment," said Ashim Sanyal, chief executive officer of Consumer Voice, a consumer rights organization.

Finance minister Nirmala Sitharaman recently underscored the need to target one billion UPI transactions per day within the next 2-3 years and stressed on accelerating the internationalization of UPI through interoperable frameworks and expanding global payment acceptance.

Also read: Goods trade deficit widens to a five-month high of $26.42 billion in April

The Reserve Bank of India wants credit and debit card issuer banks to provide customers with options to choose from multiple payment networks—such as Visa, MasterCard and RuPay—at the time of issue. The popularity of UPI has pushed banks to issue RuPay cards that facilitate UPI transactions. RuPay credit cards attract MDR of 1-2%.

According to experts, merchants set product prices which remain the same for all payment modes. The only benefit passed to consumers in the form of lower prices is when a merchant accepts only UPI payments.

Meanwhile, the Payments Council of India, representing various non-banking payment players, has unsuccessfully lobbied the government to introduce MDR on UPI and RuPay debit cards, pointing out the cost of operating back-end systems. It has proposed MDR for RuPay debit cards for all merchants and an MDR of 0.3% for UPI, applicable only to large merchants with annual sales above ₹20 lakh. The council says this is necessary for the long-term viability of the system, as zero charges prevent payments firms, banks and fintech companies from investing in critical areas such as cybersecurity, innovation and infrastructure upgrades.