Two years since Adani bought Ambuja and ACC, is a merger on cards?

- The merger may create a Rs2 trillion cement behemoth and smoothen Adani Group's processes to help it grow faster to compete against Aditya Birla Group's UltraTech Cement Ltd. as the group aspires to achieve the top spot in the cement industry

The Adani group is weighing a plan to merge Ambuja Cements Ltd and ACC Ltd that it acquired two years ago into a single entity, two people aware of the plan said, creating a cement behemoth worth over ₹2 trillion.

The group has appointed Jefferies and Axis Capital to advise on the planned merger which would be the biggest in India's cement industry, the people cited above said on the condition of anonymity. The group began integrating the operations of the two companies just a few weeks ago, they added.

The merger likely to be executed through a share swap, and the combined entity under Adani Cement Ltd will sell cement and construction materials businesses products under existing brands, the people said. Adani group is aiming to be India's top cement maker by 2028, surpassing Aditya Birla Group's Ultratech Cement Ltd.

"Many brands, but one corporate or one operation," one of the two people said.

Spokespersons of the Adani group and Jefferies declined to comment, while an email sent to Axis Bank remained unanswered.

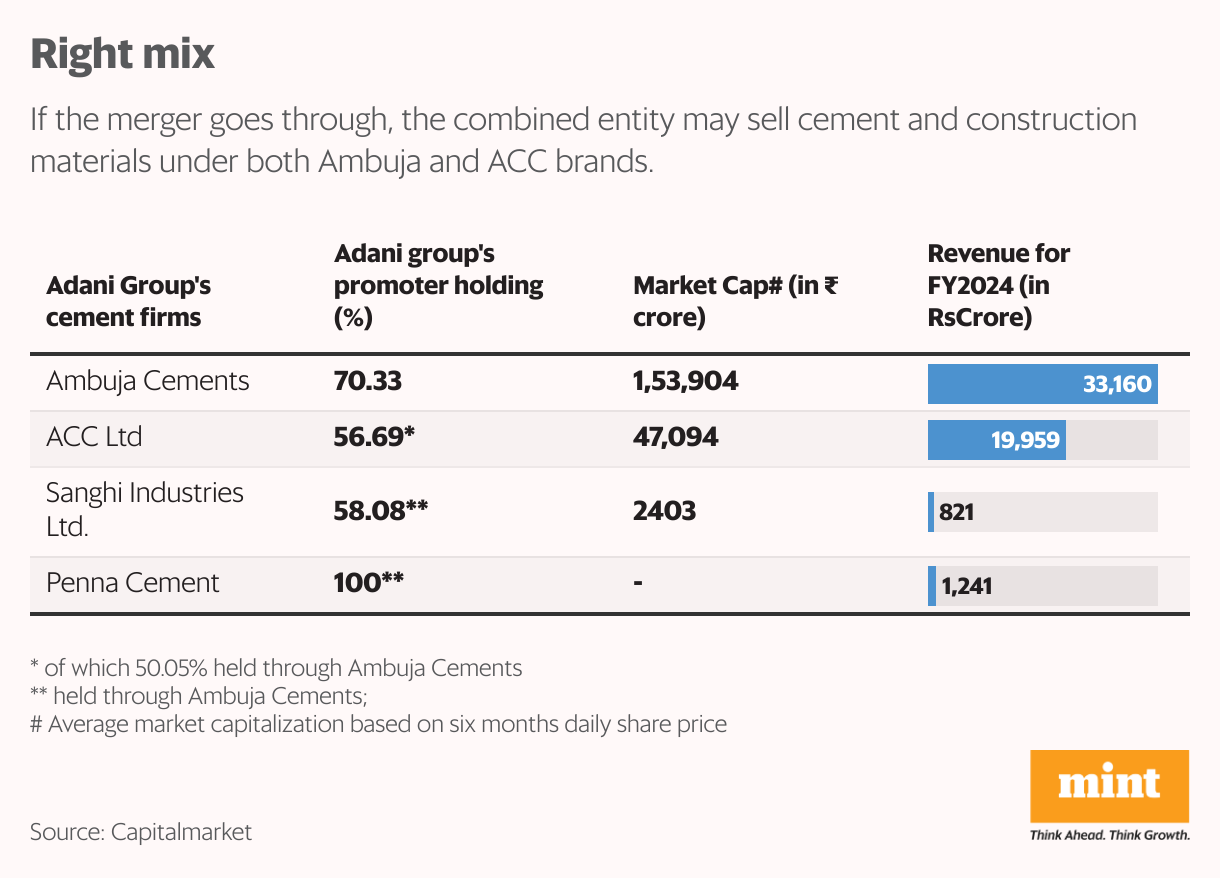

Adani group holds 70.33% in Ambuja Cements, which in turn holds 50.05% in ACC. The promoter group holds a total of 56.7% in ACC. After acquiring these two companies for $10.5 billion in 2022, Adani further acquired Sanghi Industries Ltd and Penna Cement Ltd.

Also read | Gautam Adani’s Ambuja Cements draws up $9-billion war plan for Ultratech battle

Since Ambuja Cements hold 58.08% in Sanghi, which too is listed, the merger plan may also include Sanghi Industries to ensure all listed cement-making firms come under one single entity, the person cited above said. That would make it a two-step process, in which Sanghi first merges with Ambuja Cements, and then ACC and Ambuja Cements combine to create one listed entity, said one of the persons.

"A concrete structure on share swap is yet to be in place. The plan is in an early stage. But the integration should be completed by June 2025," the second person added, adding the merger process will start closer to the completion of the integration or just after that. "The merger may take longer as it requires board's shareholders and regulators' approval," the person added.

Sumangal Nevatia, associate director, Kotak Securities Ltd, said the merger offers several operational synergies.

"It helps the group in terms of costs, management control, scale, supply chain and operational requirements. Rather than having four different boards, management, processes, and listing requirements for the same business, it makes more sense to consolidate and bring the entire business under one management. This may enhance efficiency. But, for such a merger, there may additional stamp duty costs with regards to mining rights. One has to work out the costs and see how it compares with the benefits of the merger," said Nevatia.

The merger, however, may face procedural challenges due to certain regulatory constraints on the transfer of rights or leases in mining assets. The cement industry's raw materials such as limestone, silica, aluminates and ferric minerals are all obtained from mines. In 2018, the curbs on transferring mining rights had stalled a similar merger between ACC and Ambuja Cements under its former owner LafargeHolcim.

Also read | Adani’s resurgence: A $5-7 bn war chest for cement, ports, defence acquisitions

A cement industry analyst at a top Indian brokerage firm said the merger makes sense, even though the transfer of mining and leasing rights may involve cost and time.

“The brands ACC and Ambuja Cements should remain even if the companies merge to become one listed entity. Merger will help in terms of listing requirements and operational expenses," the analyst said on the condition of anonymity.

The Adani group enjoys certain advantages in the cement business, given its large infrastructure operations spanning ports, real estate, road construction and power generation, offering a readymade customer base. Its power plants throw up fly ash which is used in cement making, and having it in-house will help save costs and pricing power.

Similarly, Adani has coal import arrangements with Australia and other countries for power businesses, which can be leveraged in production of cement that requires intense energy. The group has its own energy generation firms as well. For supplying and transporting raw materials or the finished cement product, Adani can use its own ports and logistics network to save significantly on costs.

Also read | Mint Primer | Mining minerals: Could cement & steel get dearer?

Within real estate, the group has cement requirements from major projects including the Navi Mumbai Airport, Ganga Expressway and the planned redevelopment of Asia's largest slum Dharavi in Mumbai.

In a May 2024 presentation to investors and creditors, the group spoke about these synergies, stating that at least 65% of the total cost of cement has synergies with the group itself.

At present, Ambuja Cements and ACC's market capitalization are at ₹1.5 trillion and ₹46,000 crore respectively. Sanghi has a market cap of ₹2100 crore, while Penna Cement is unlisted. The share swap will partly depend on the market cap of the two firms, among other parameters.

In FY24, Ambuja Cements earned a revenue of ₹33,160 crore, with net profit of ₹4,738 crore, while ACC's total income was ₹29,443.7 crore, with net profit at ₹2124.24 crore.

The Adani group wants to enhance its market share to over 20% by FY28 from around 14% now.

After acquiring Penna Cement for ₹10,422 crore in June, Adani's operational capacity rose to 89 mtpa. From this acquisition, another 4 mtpa capacity is under construction and will be operational in 12 months, which will be over and above ongoing expansions.

Also read | In the grinding battle for cement, UltraTech makes a big move in the south

In a June presentation, Adani said cement demand will increase further not only because of the $3 trillion infrastructure push for the next decade, but also due to the country's growing working age population, redevelopment across several cities (housing sale grew 63% in Q4 FY24 YoY (area volume growth), new economic corridors, rural homes, growth in commercial space (net leasing of office space expected to grow by 10-15%) and so on.

Adani currently owns 22 integrated cement production units, 11 captive ships, 86 ready-mix concrete plants, 10 bulk cement terminals, 21 grinding units and around 8000 million metric tonnes of limestone reserve (cumulative).

However, the group is struggling to capture market share in the South and Central India, a July presentation indicates.