Indian companies' profit puzzle: When global turmoil meets economic theory

")

From promising forecasts to a precarious present,can geopolitical shocks derail India's corporate growth story? An economic thumb rule can give some answers.

Indian companies began 2025 on a great note. Inflation was falling, the economy was growing at 6.5-7%, and the rate-cutting cycle had started. But cut to the April-June quarter, and it is an entirely different story.

Crisis after crisis has erupted, starting with US President Donald Trump’s tariffs in April, followed by tighter US visa and immigration norms, the India-Pakistan conflict in May, and the Israel-Iran face-off in June. The result? Uncertainty that brings with it downside risks to economic growth and, by extension, corporate profitability.

Also Read: Global news wrap: Israel-Iran conflict, US student visas, global growth, rising temperature

So, what’s the link between corporate profits and the economy anyway? Let’s find out what economics says.

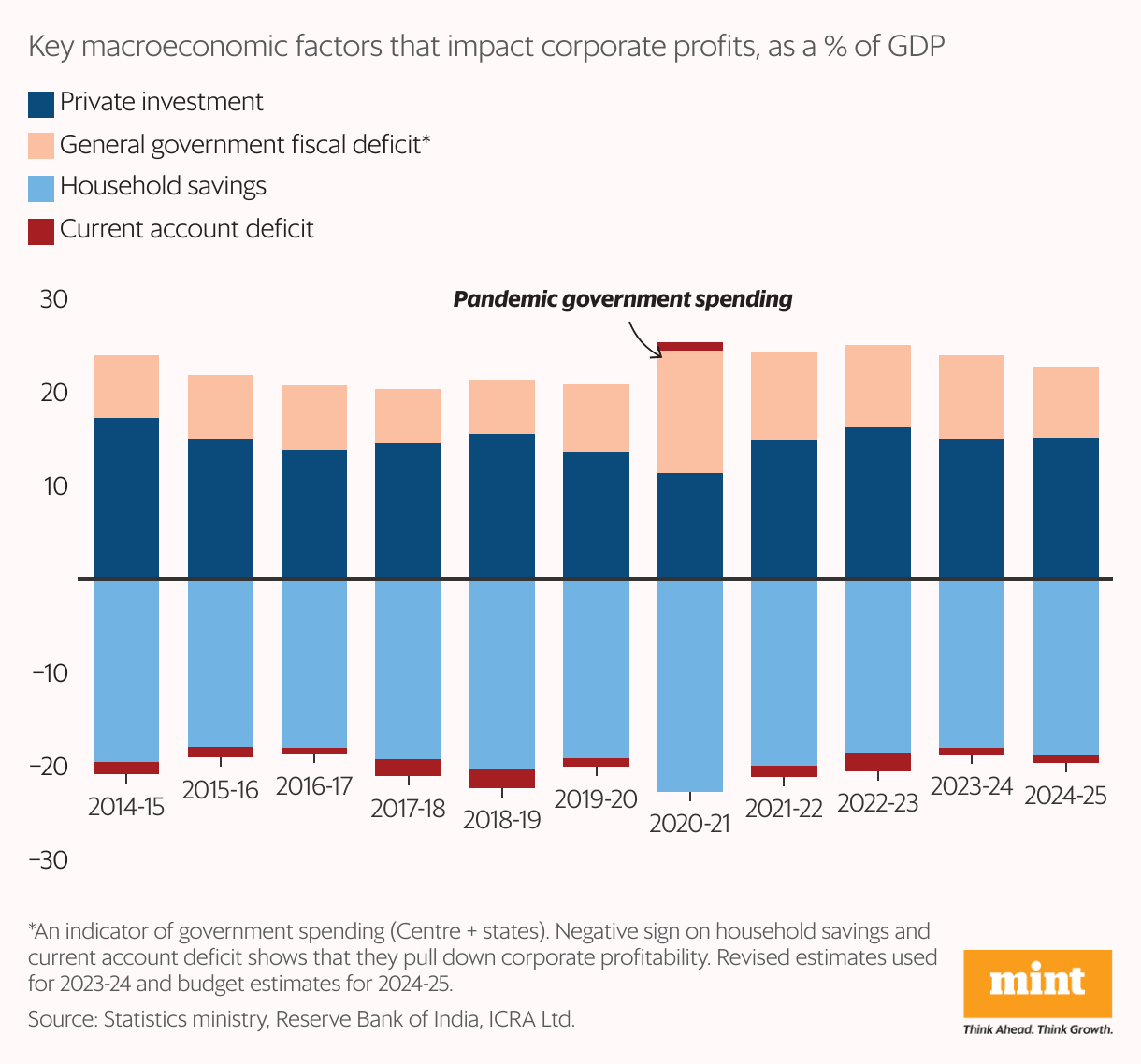

The corporate sector's profits are derived from the interplay of four macroeconomic factors: investment, government spending, household savings, and current account balance. The relationship connecting corporate profit to these macroeconomic variables is known as the Levy-Kalecki identity.

This identity views profitability in the corporate world through a macroeconomic lens, offering a way to understand how corporate profits will move in a time of economic uncertainty.

The underlying rationale is simple:

- Investment: When companies buy fixed assets and inventory, they create new revenue and profit streams. Therefore, higher private corporate investment is associated with higher corporate profitability (India saw this in the 2003-2007 boom).

- Government spending: The government buying goods and services from businesses has a direct positive impact on profits.

- Household savings/spending: When government spending flows to common citizens, some or all of that is also likely to be used to buy goods and services for households, thus again indirectly increasing corporate profits. Household savings, though, have an opposite impact, because savings represent that part of household income that is not spent on buying goods and services.

- Current account balance: When we run a current account deficit, there is a net outflow of funds to the rest of the world, implying that these funds are not available for spending in India. Hence, current account deficits have a negative impact on corporate profits, too.

So this is how macroeconomic factors impact corporate profits in theory. Now let’s see how it’s played out in reality.

Also Read: In charts: Why West Asia is important for India beyond trade

Stacking the Levy-Kalecki macroeconomic variables over 2014 to 2024 shows that private investment has been declining, and the government has done most of the heavy lifting on this front. A case in point is 2020-21: when the pandemic cut private investment and household spending, government spending came to the rescue.

But these dynamics have changed now. New developments threaten corporate profitability on at least three fronts.

- First, the government’s determination to stay on the path of fiscal prudence means that its spending cushion may not be available to the same extent in the coming years. The impact? Theory says corporate profits will suffer.

- Second, household borrowing is already rising. If the prevailing uncertainty leads to job losses, households are likely to cut back on discretionary spending. In other words, the household savings rate could reverse after three years of trending downwards. The impact? Theory again says corporate profits will suffer.

- Third, if the tensions in West Asia push up crude oil prices, the current account deficit could go up (as would inflation, further reducing households’ ability to spend). The impact? Theory says corporate profits will suffer, yet again.

So, in summary, what we see now is a combination of macroeconomic factors that could be detrimental to Indian companies' profits.

Then, where will corporate profits come from? The only option left is to raise private investment—something that has been elusive for years now.

Also Read: Missing from India's population narrative: Unmet family goals, financial barriers, coercion

The Reserve Bank of India (RBI) has done its bit to reduce the cost of capital by cutting the policy rate by 100 basis points this year and pumping abundant liquidity into the market. But investment intentions translate into actual capital spending only when companies are reasonably certain about future demand.

And herein lies the real problem: both domestic and export demand are facing headwinds of uncertainty. Urban consumer confidence is stagnant, and rural confidence shows only a modest rise. The risk of China dumping cheap goods into India is high. Export growth is threatened by rising tariffs and trade protectionism. Under these conditions, it is tough to expect a surge in private investment.

That brings us to a chicken-and-egg situation: private investment follows growth, and this time, growth may need investment to pick up.

At this point, the only thing we know for sure is that corporations will be cautious about investing until the global situation is clearer. Thus, even though our economic fundamentals are better than they have been for a long time, any expectation of a boom in corporate profitability will remain hostage to geopolitical risk.