A glimpse into the house that Deepak Parekh built

")

- Before its merger with HDFC Bank Ltd, effective from 1 July, HDFC had 21 subsidiaries or associate companies. All the significant ones are leaders in large, essential, and expanding sectors of financial services

MUMBAI : In 1978, Deepak Parekh joined Housing Development Finance Corp. (HDFC) Ltd, a housing finance company set up by his uncle, and built it out. When India opened financial services in the 1990s, he led the group’s diversification into many sectors. It wasn’t just about registering a presence, it was about making an indelible mark. Before its merger with HDFC Bank Ltd, effective from 1 July, HDFC had 21 subsidiaries or associate companies. All the significant ones are leaders in large, essential, and expanding sectors of financial services.

Besides Parekh, credit should also go to leaders like Aditya Puri, Deepak Satwalekar, Keki Mistry, Renu Sud Karnad, and Milind Barve, who all had long stints at the top. Sashidhar Jagdishan, the managing director and chief executive of HDFC Bank, has been with the bank since 1996. In the bank’s 2021-22 annual report, he outlined reasons for the merger: “…only 2% of our customers source their home loans through us, while 5% do it from other institutions. The latter is equivalent to the size of our retail book. Home loan customers typically keep deposits that are 5 to 7 times that of other retail customers. And about 70% of HDFC’s customers do not bank with us."

In other words, HDFC Bank was not maximizing the housing loan space by itself. And the HDFC group was not maximizing the network possibilities that HDFC customers presented. The regulatory reasons to keep both firms separate were anyway diminishing. It made sense to pass the baton from the ‘parent’ to the ‘child’—both immense performers in their own right.

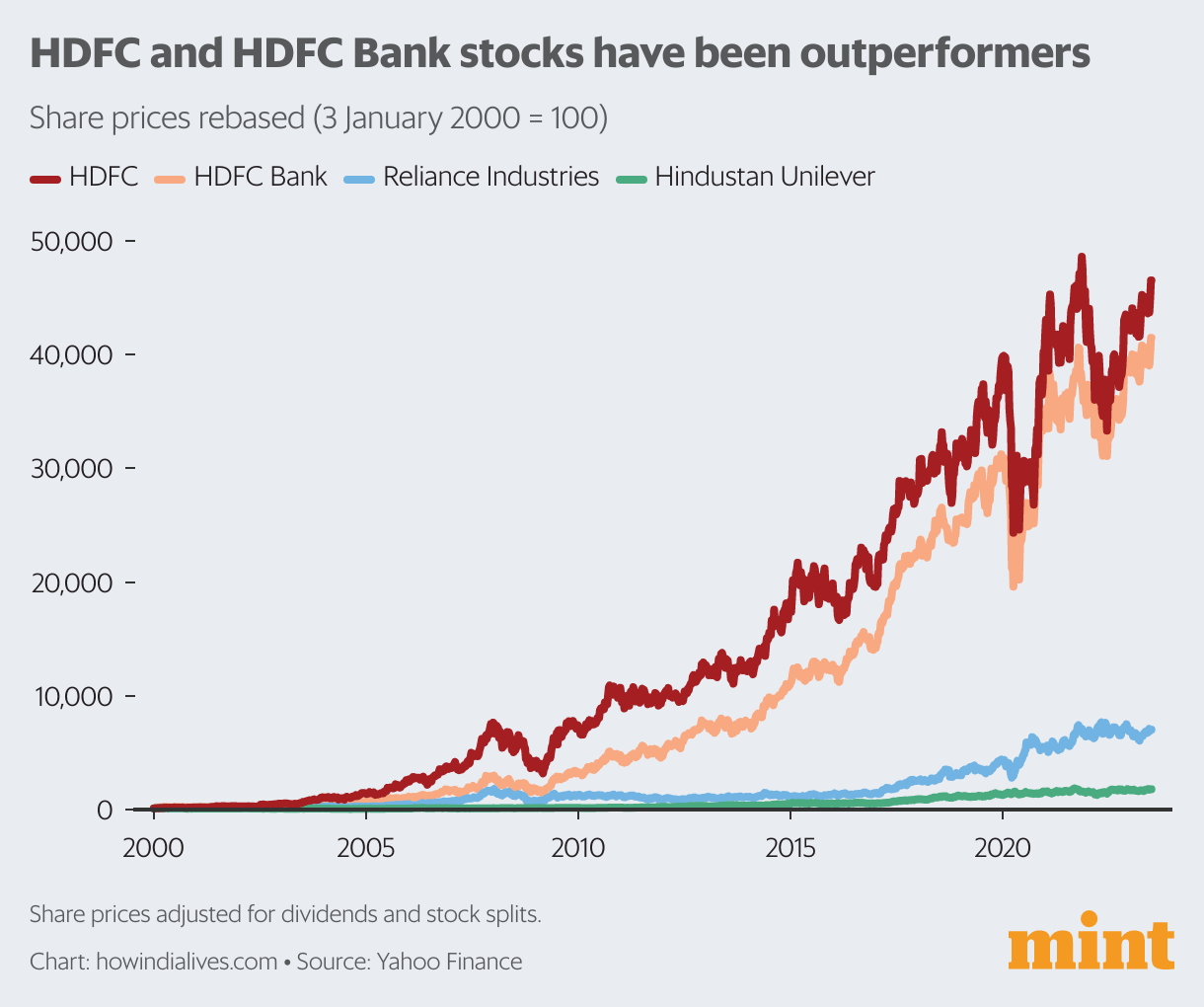

Soaring Stocks

WHAT PAREKH and his team achieved is magnified when seen through the prism of shareholder returns. Both HDFC and HDFC Bank were among the 30 stocks that made up the bellwether index BSE Sensex. In this century, HDFC returned a compounded 30% a year and HDFC Bank 29%. They tower above two other blue-chip, old-economy businesses that were in the Sensex during this period: Reliance Industries Ltd returned 20% and Hindustan Unilever Ltd 13%. The Sensex, in this period, returned 11%.

In the case of HDFC Bank, super-high shareholder returns were the byproduct of a relentless pursuit of consistent—not supernormal—growth under Aditya Puri, who led the bank from 1994 to 2020. It aimed for 20% year-on-year growth and hit it almost every year. Thus, ₹10,000 invested in the HDFC and HDFC Bank stocks on 1 January 2000 is today worth ₹46.5 lakh and ₹41.5 lakh, respectively.

Different Tracks

THE PRISM of shareholder returns also offers a clue to why this merger was more a question of when, and not why. In the past 10 years, the HDFC Bank stock has returned a compounded 19%, while HDFC has returned 14%. Growth at the housing finance major had been slowing. By comparison, HDFC Bank was still hitting its stated 20% growth target with metronomic consistency. Between 2013-14 and 2022-23, HDFC Bank topped HDFC on every growth metric by a handsome margin. On the one hand, HDFC Bank could raise cheap deposits to fund its growth. On the other, it could deploy these deposits and increase its loan book. During this period, retail loans, including housing loans">housing loans, comprised 50-57% of the bank’s loan book.

The relative growth rates of HDFC and HDFC Bank during the past decade underscore the changing nature of financial services and the convergence around the bank.

Generational Shift

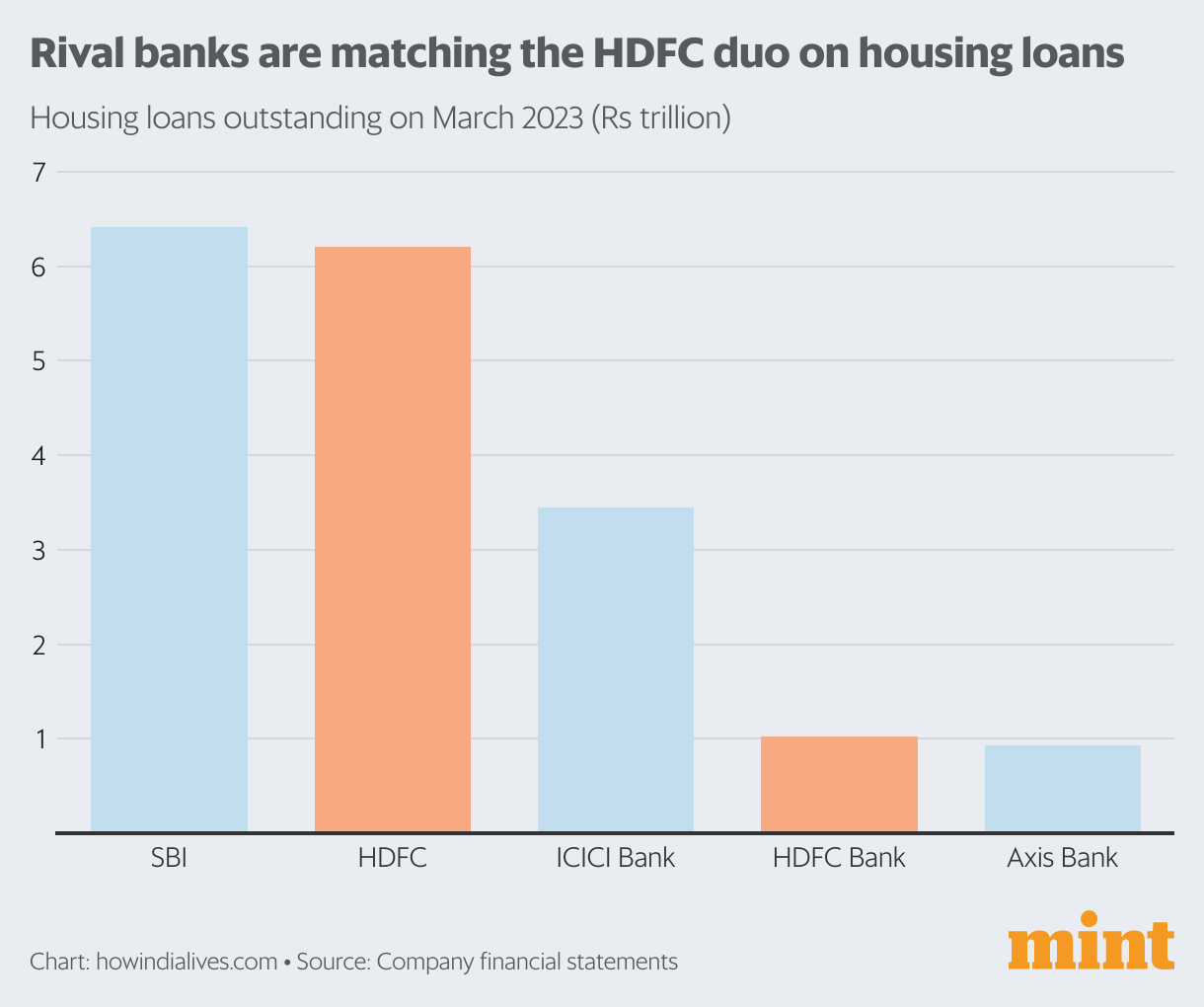

IN 1994, when HDFC Bank was incorporated, a bank had to keep 15% of its deposits with the regulator as the cash reserve ratio (CRR) on which it earned nothing. Another 35% went into government securities towards maintaining the statutory liquidity ratio (SLR). Thus, it could deploy only half of its deposits as loans. Not being a bank, HDFC did not have to maintain such onerous requirements.But HDFC did not enjoy cheap deposits. Its average cost of funds in 2022-23 was 6.7%, against 3.7% for HDFC Bank. Today, CRR and SLR are down to 4.5% and 18%, respectively. Interest rates are lower. There is greater order in real estate. Banking has changed: State Bank of India does more housing loans than HDFC. The housing loan book of ICICI Bank Ltd is 3.4 times that of HDFC Bank. A generation has passed, and the child has truly taken over.

www.howindialives.com is a database and search engine for public data.