Chairing Tata: How RNT set the leadership benchmark for his successors

- In the last 33 years, the Tata group has had three chairmen—Ratan Tata, Cyrus Mistry and N. Chandrasekaran. Of the three, Ratan Tata inherited the most challenging legacy. What do we learn from his leadership playbook?

New Delhi: For over a century, the Tata group has been a cornerstone of Indian industry, spanning sectors from steel to software. At the helm of this corporate giant have been three key leaders: J.R.D. Tata, Ratan Tata, and N. Chandrasekaran. Each has left an indelible mark, shaping the group’s trajectory in the face of an ever-evolving global business landscape.

However, a stark contrast underscores J.R.D. Tata’s towering influence. He served as chairman for 53 years, a tenure that profoundly shaped the group’s foundation and culture. In the 33 years since, the group has seen three chairmen, each adapting to the challenges of their time. Even Cyrus Mistry, despite his brief tenure, made significant directional changes after succeeding Ratan Tata in 2012.

The heavy lifting, however, was done by Ratan Tata during his 21 years at the helm from 1991 to 2012, and since 2016, by N. Chandrasekaran, a group lifer and the first professional to lead the Tata group.

Their leadership provides a lens through which we can assess the progress of the $165 billion steel-to-software conglomerate. Founded 156 years ago by Jamshedji Nusserwanji Tata, with a vision to establish an iron and steel company, a luxury hotel, a world-class educational institution, and a hydroelectric plant, the Tatas have remained faithful to this mission.

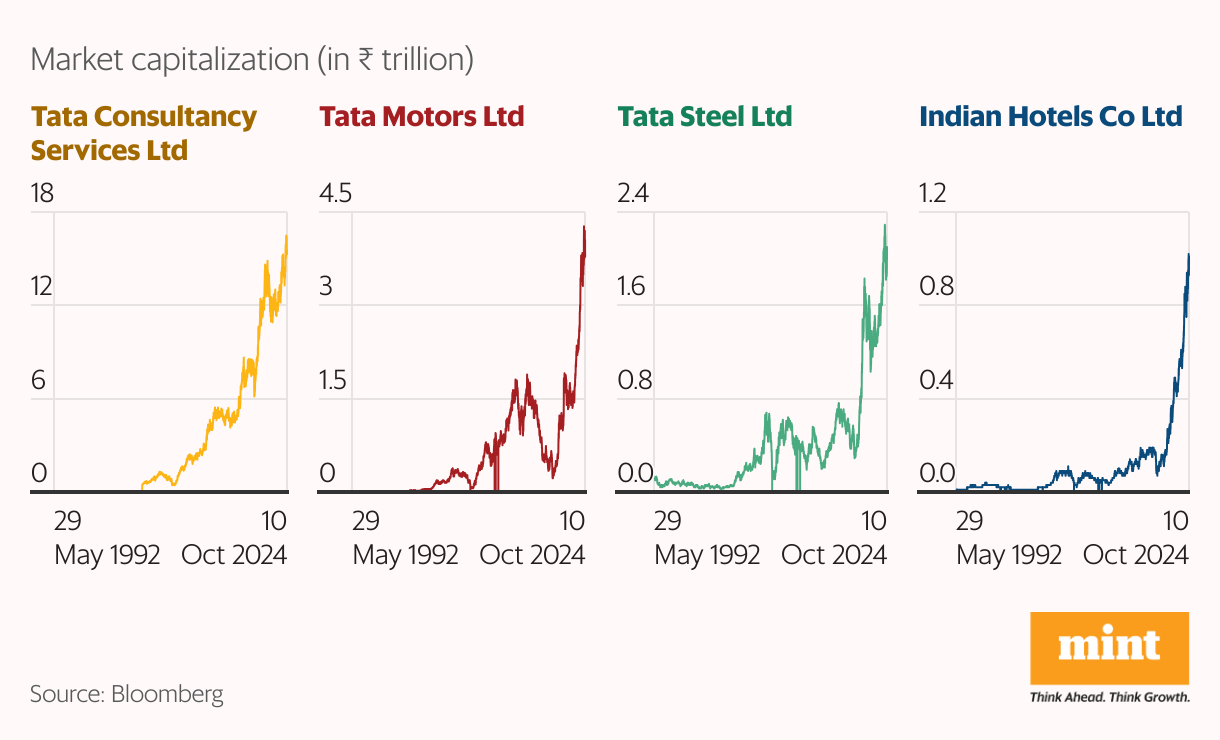

Tata Steel, Indian Hotels, and Tata Power stand as leaders in their sectors, while institutions like the Tata Institute of Fundamental Research, the Indian Institute of Science, and the Tata Institute of Social Sciences underscore the group’s contributions beyond business.

The three chairmen represent varying degrees of family attachment and influence.

Ratan Tata, a true heir to the Tata legacy, was followed by Cyrus Mistry, an insider due to his family’s 18.4% stake in the group. N. Chandrasekaran, however, was the rank outsider—neither a Tata nor a Parsi, and not a shareholder—rising from within the organization. His leadership is a testament to the group’s meritocratic culture and its rejection of tribalism.

Whim & fancy

Of the three, Ratan Tata inherited the most challenging legacy: a collection of loosely connected businesses spread across multiple entities, with varying degrees of control by the holding company. While nominally part of the Tata group, there was little cohesion among them, making it difficult to consider Tata a true conglomerate in the vein of GE. Regulation, chance, and circumstance had all played a role in shaping this mix of interests.

For instance, J.R.D. Tata launched Tata Airlines on a whim in 1932, when he flew the first single-engine de Havilland Puss Moth in India. Twenty-one years later, the government nationalized it, extinguishing the group’s airline ambitions for nearly six decades. Similarly, in 1968, J.R.D. placed a young technocrat, F.C. Kohli, in charge of a nascent Tata Consultancy Services (TCS), a management and technology consultancy that eventually became the group’s cash cow. When Ratan Tata assumed leadership in 1991, however, TCS had more promise than performance. It would take the software export boom from India and some initial indifference from Tata, who had bigger issues to tackle, to allow the fledgling company to grow independently.

Velvet glove, iron fist

J .R.D. Tata was a great leader who believed in empowering others, which fostered a culture where figures like Russi Mody, Darbari Seth, and Ajit Kelkar ran their businesses as if they were their own. The problem, however, was that such independence, once granted, became difficult to rein in. Over time, all three leaders came to view the companies they headed as personal fiefdoms, presenting a unique challenge for Ratan Tata as he sought to consolidate control.

For Ratan Tata, the immediate challenge was to assert his authority over a sprawling and fragmented business empire. He understood that this required direct confrontation, and while his approach was often measured, it became clear that his velvet glove concealed an iron fist.

It took nearly six years to quell the simmering unrest among the powerful satraps, with one case—Russi Mody at Tata Steel—almost escalating into open rebellion. Mody eventually retired in 1993, followed by Darbari Seth at Tata Chemicals, though Seth negotiated the appointment of his son, Manu Seth, as managing director as part of his exit.

The most resistant of them, Kelkar, was finally ousted during a board meeting in September 1997, when Ratan Tata assumed the role of chairman and managing director of Indian Hotels Co. Ltd (IHCL).

From India to the world

During this period, Ratan Tata also focused on strengthening Tata Sons’ stake in key group companies, some of which had dangerously low holdings, leaving them vulnerable to hostile takeovers, as seen with Tata Steel in the mid-1990s. In a more controversial move in 1996, he introduced the Tata Brand Equity and Business Promotion (TBEBP) scheme, requiring companies to pay a royalty to Tata Sons for the use of the Tata name.

While it wasn’t a major cash generator, the decision faced resistance, and eventually, to address investor concerns, the royalty was capped at a modest ₹75 crore.

However, this was merely the beginning. Tata’s true ambition was to expand the group’s market reach from India to the world. This global push began with the £270 million acquisition of British firm Tetley in 2000, and over the next nine years, the group acquired 36 companies, including Corus in 2007 and Jaguar Land Rover (JLR) in 2008. These two deals alone amounted to an eye-popping $15 billion.

Despite the enormous investments, Tata worked diligently to improve the group’s capital efficiency and balance sheet, not only through financial assets but also by enhancing its intangible assets. As a result, raising funds for these ambitious acquisitions proved relatively easy, with banks eager to lend support.

In hindsight, some acquisitions, notably Corus and JLR, were overpriced and did not yield the expected financial returns. While it’s unfair to fault Tata for China’s aggressive dominance in the global steel market, which made Corus unviable, these acquisitions saddled the group with significant debt—at a time when the world was grappling with the financial crisis. This period marked one of the most controversial chapters in the group’s storied history.

The Mistry chapter

In December 2012, Ratan Tata turned 75 and, in line with the policy he had helped establish, retired as chairman. In his wisdom he selected, as his successor, Cyrus Mistry, whose family had held an 18.4% stake in Tata Sons for over 35 years. After a brief honeymoon period, it became evident that Mistry intended to chart his own course. Rather than preserving the legacy he inherited, he set out to fix what he perceived as flaws, with his primary focus on addressing what he referred to as “a set of ill-conceived global acquisitions," a point of contention that would later fuel a bitter court battle following his ouster four years later.

Mistry’s claim that these acquisitions led to “the largest value destruction in Indian corporate history" was undoubtedly an exaggeration, but there was merit in re-evaluating the group’s unchecked growth, particularly some of the acquisitions and other initiatives undertaken during Tata’s tenure.

Two businesses, in particular—passenger cars and airlines—were bleeding the group, while another, telecom services, was stagnating. These ventures highlighted another issue: over-centralization, with decision-making ultimately resting with one person. Mistry’s response to this was the creation of the group executive council (GEC), a brain trust designed to decentralize power. However, this move upset many within Tata Sons, who saw it as a rival power centre.

Despite the internal friction, Mistry took significant steps into businesses that would shape the group’s future. Early in his tenure, he facilitated Tata Power’s $1.4 billion acquisition of Welspun’s solar farms, marking a strategic entry into the green energy sector. Digital initiatives also started gaining prominence within the group’s agenda. However, before he could fully implement his vision, his tenure was abruptly cut short.

Mistry’s conflict with Tata, culminating in his removal and the subsequent legal battle, was as much about differing leadership styles as it was about the group’s direction.

Ratan Tata had always been a big-picture leader, focused on long-term growth. Mistry, on the other hand, saw the need to address internal issues before expanding outward. However, Tata had a unique ability to rally people behind his vision, even when it defied conventional business wisdom. The Nano project, for instance, demonstrated a misreading of the Indian market, while the two airline ventures were classic examples of one hand not knowing what the other was doing.

Super salesman

Enter N. Chandrasekaran, a man lauded even by his competitors as a “super salesman" for his role in the extraordinary success of Tata Consultancy Services (TCS), the crown jewel of the Tata group. The task before him was daunting—continuing the good work initiated by Cyrus Mistry while aligning with the ethos of his former boss, Ratan Tata.

Chandrasekaran, meticulous and methodical, took on this challenge with precision. One of his first major accomplishments was resolving the long-standing dispute with Japanese telecom company NTT Docomo, which had been a source of friction under Mistry and had caused significant heartburn for the group.

Next came a critical pivot at Tata Motors, whose domestic business was struggling. Chandrasekaran’s focus on electric vehicles (EVs) gave the company a clear direction. This strategic shift culminated in a major deal in October 2021, with private equity firm TPG and ADQ of Abu Dhabi investing ₹7,500 crore ($1 billion) in Tata Motors’ EV division, valuing the business at $9 billion. Following this success, Chandrasekaran announced mega investments in semiconductors, 5G technology, and digital ventures.

As the most tech-savvy Tata chairman, Chandrasekaran understood that the future of the group’s diverse businesses—from consumer products to energy and engineering—would be driven by technology. Leveraging the group’s intrinsic strengths in this area, he positioned Tata to capitalize on technological advancements. Under his leadership, the Tata group has grown in both market share and value in its key businesses.

Chandrasekaran’s test

Yet, Chandrasekaran’s real challenge is just beginning. Much like Ratan Tata, who spent his first few years resolving legacy issues, Chandrasekaran’s initial years were focused on addressing lingering concerns. But the true measure of a leader of a conglomerate lies not in dousing small fires but in creating a vision for the future. Ratan Tata transformed the group by instilling a global mindset, raising the share of revenues from outside India from less than 10% to 60% during his tenure. While some of his bold bets may not have panned out, they do little to diminish the significance of his accomplishments and the transformative impact he had on the group.

Chandrasekaran’s test will be to maintain that momentum. As a seasoned marathon runner, the 61-year-old knows the importance of pacing for the long haul. “We are trying to get the group prepared for the future," he told the Financial Times in an interview.

But defining the nature of that growth won’t be easy. With the conglomerate model facing scrutiny globally, Tata’s broad-based approach—offering “all things to all people"—is inherently risky.

The airline business, with its disparate challenges across different companies, and the digital venture, where Tata Neu has had a rocky start, will both demand significant resources and attention beyond what one leader can provide. Identifying new leaders who can take ownership of these businesses will be crucial.

Complicating matters further is the impending selection of a new chairman for the Tata Trusts, which holds a 66% stake in Tata Sons, the holding company that controls the group’s various businesses.

Chandrasekaran’s relationship with the new Trusts chairman—effectively the representative of the owners—will be closely monitored. A harmonious working dynamic, similar to the one he had with Ratan Tata, would ensure a balance of family support and professional leadership, fostering the group’s sustained growth. However, any discord could cast a shadow over the group’s smooth functioning.

Although the passing of an era may not seem like the ideal time to confront these looming challenges, N. Chandrasekaran doesn’t have the luxury of time.