Economy

Economy

Mint Primer | The 3% fiscal deficit target: Is it sacrosanct?

")

Summary

- The government says there is no scientific basis to the 3% target. A slightly higher deficit would actually help the economy grow faster. It will also provide the Centre with enough fire power when a crisis such as the pandemic strikes.

In a bid to provide maximum flexibility to growth, the government has tweaked its approach to fiscal consolidation. It no longer wants to fix a fiscal deficit target. Mint looks at the new approach and the significance of the 3% target set by law.

Why do we need fiscal consolidation?

Governments need to live within their means. But with the ability to print money and borrow at will, they often spend more than what they earn, causing fiscal deficit. So, that’s the difference between revenue and spending (shown as a percentage of gross domestic product). Having a high fiscal deficit is not good economics. It causes inflation to rise and hurts economic growth as it forces interest rates to remain high. Fiscal consolidation is the process of controlling the fiscal deficit by ensuring that expenditure does not significantly exceed revenue. Most governments do this by setting a legally mandated target.

Read more: War for deposits: Banks’ biggest headache now coming for investors?

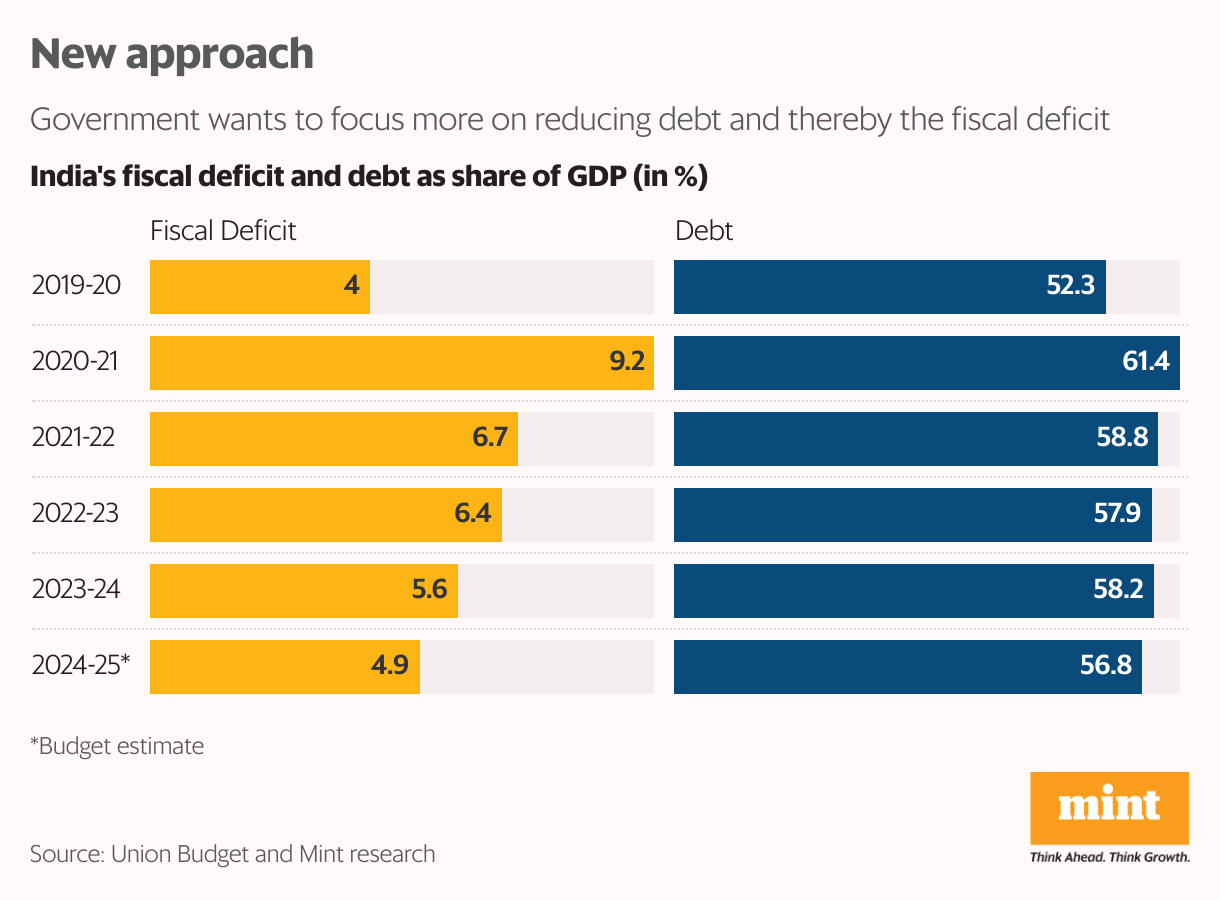

How did we get to the 3% target for India?

The Fiscal Responsibility and Budget Management Act, 2003, mandates the Union government to keep the fiscal deficit below 3% of its gross domestic product. More than two decades after the law came into effect and for reasons both within and beyond its control, the Centre has not been able to meet this target even once. In FY19, the deficit came down to 3.4% but the pandemic that followed pushed it up to 9.2% in FY21. The Modi government has been aggressively reducing it ever since. In FY24 it managed to reduce it to 5.6%. The target for FY25 is set at 4.9% and in FY26 it is expected to be below 4.5%.

Don’t states have to keep the deficit down too?

Indian states too are obligated to keep their fiscal deficit under check, and they have done a much better job of it than the Union government. The aggregate fiscal deficit of the states was well below 3% in four of the last six years. It touched 4% in FY21 post-covid. In FY24, the revised estimates put it at 3.4% and this is expected to decline to 3.1% in FY25.

Read more: We can’t celebrate India’s small current account deficit: Here’s why

Is there a change in approach?

Next cabinet secretary T.V. Somanathan has said the Centre is no longer committed to a 3% fiscal deficit target. He said that after FY26 (by when it would be below 4.5%) the target will be dynamic and set in a manner the government’s debt-to-GDP (an unsustainable 58.2% in FY24) is on a declining trend. This, the Centre feels, will provide more flexibility for growth by making enough resources available. A fast-growing economy like India, he argued, can afford a higher fiscal deficit and still reduce debt.

So is the 3% target sacrosanct?

The government says there is no scientific basis to the 3% target. A slightly higher deficit would actually help the economy grow faster. It will also provide the Centre with enough fire power when a crisis such as the pandemic strikes. Post-covid, it spent heavily on infrastructure to revive growth. But many economists say a deficit that is higher than 3% will increase India’s borrowings at a time when savings are declining. This will push up interest rates, hurt private investment and slow economic growth.

Read more: India steps up push to make rupee a power player, but the road is long