Why Fed rate cut isn’t the only factor shaping RBI meet

")

- The US Fed’s rate cut has already pushed some emerging market central banks to follow suit. But India’s monetary policy committee, which is meeting this week, has much more on its plate before it can follow that path.

The US Federal Reserve’s 50-basis-point rate cut was a cue to action for central banks around the world. Some emerging markets were quick to follow suit: Indonesia led with a pre-emptive cut, followed by South Africa, Mexico, and China, which rolled out a stimulus package that included key short-term rate cuts.

Read this | RBI may change policy stance, tweak growth forecast: Mint Poll

As the Reserve Bank of India’s (RBI) monetary policy committee convenes this week, it faces a key decision—whether to reduce the repo rate or wait for inflation, particularly food inflation, to stabilize. But there are more factors at play.

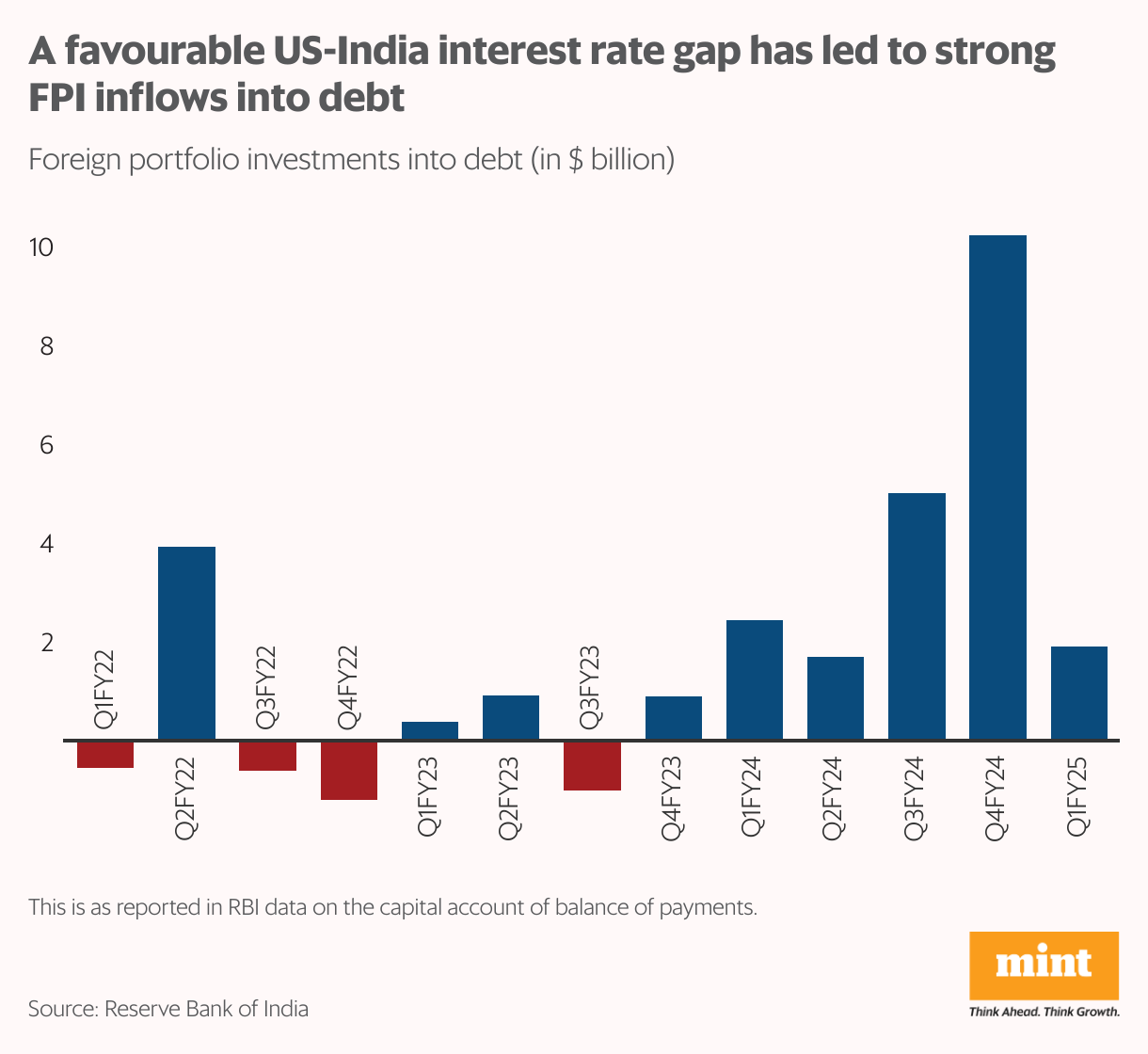

A primary concern is the impact of monetary policy on foreign portfolio flows. Debt inflows have been particularly strong for the last six quarters, driven by a wide interest rate differential between India and the US, as well as the inclusion of Indian bonds in global indices. India isn’t alone in reaping the benefits: in expectation of a US rate cut, global portfolio flows into emerging market debt reached over $58 billion in July and August, dwarfing the $9 billion that went into equities, according to the IIF Capital Flows Tracker.

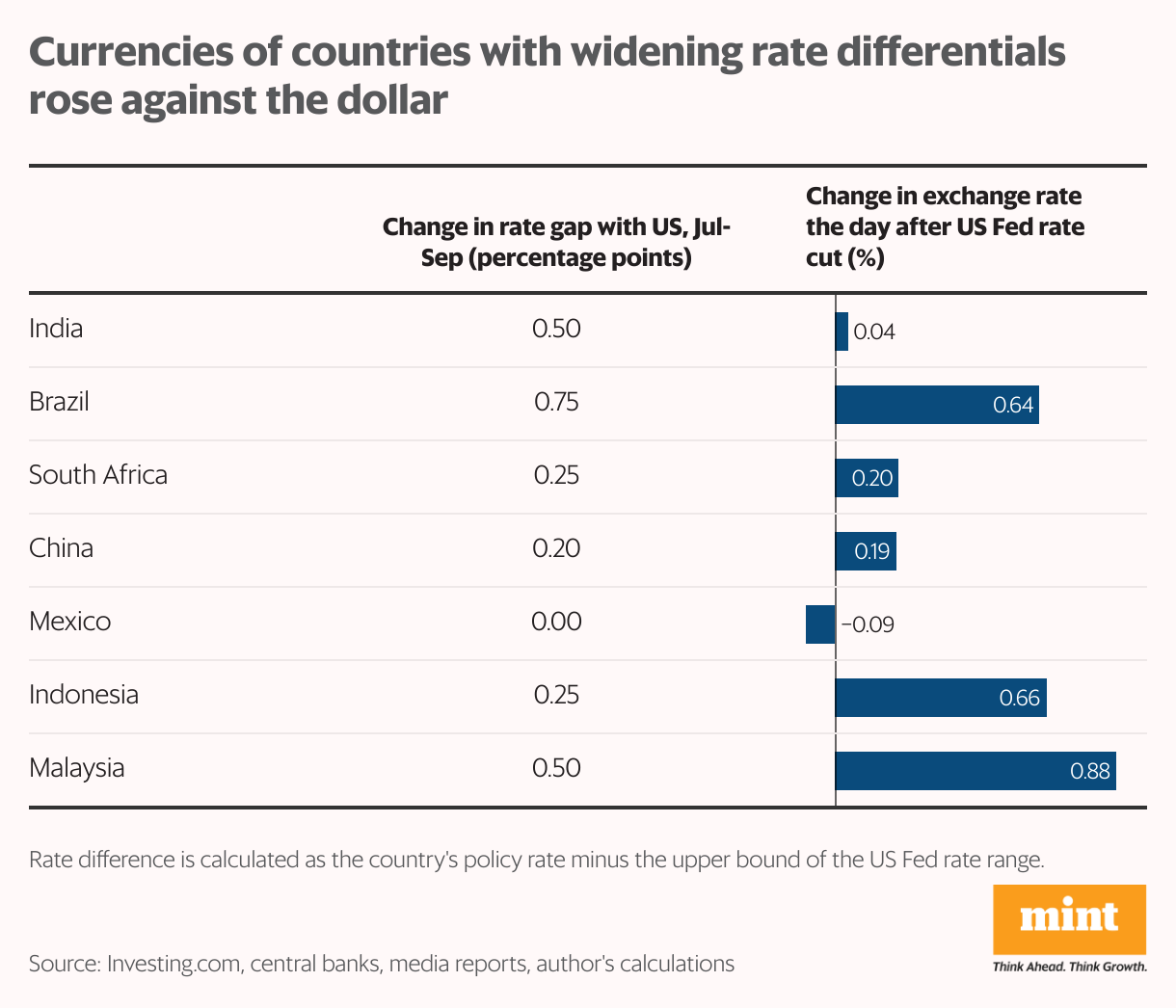

In a world where markets compete for mobile global capital, increasing or at least maintaining the interest rate gap would keep Indian debt attractive. Markets track this rate differential: Currencies of countries with a wide (or widening) rate differential strengthened after the Fed rate cut. The rupee gained 0.04% the next day, and the Brazilian real by 0.6%.

From bull to bubble?

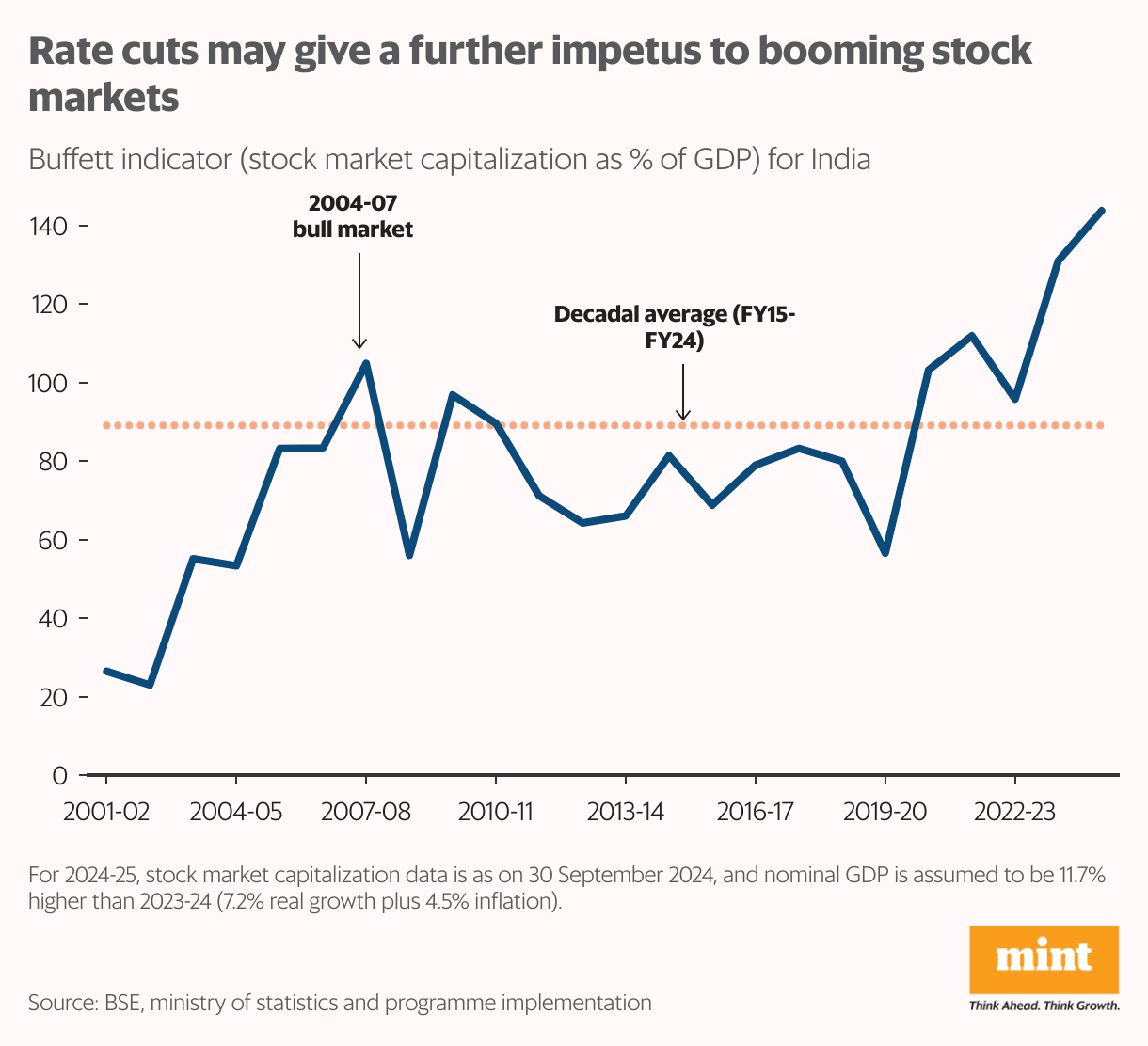

The second factor is that an easing cycle at this point carries the risk of tipping an already frothy stock market into bubble territory.

And this | Will a surprise uptick in August inflation put RBI rate cut timeline in limbo?

Indian equities have remained bullish despite two years of tight monetary policy. The Buffett indicator, which compares market capitalization to GDP, underscores the degree of overvaluation. A ratio of 100-120% is generally seen as fair value, indicating that the total market worth of listed companies aligns with the value of goods and services produced. However, since 2023, this ratio has surged, now well above its long-term trend. Even allowing for the forward-looking nature of markets, the current figure exceeding 140% suggests stock prices may have outpaced economic fundamentals.

If this bubble bursts, the resulting market crash could seriously dent the confidence and savings of millions of retail investors, many of whom have only recently entered the stock market.

Deposit drain

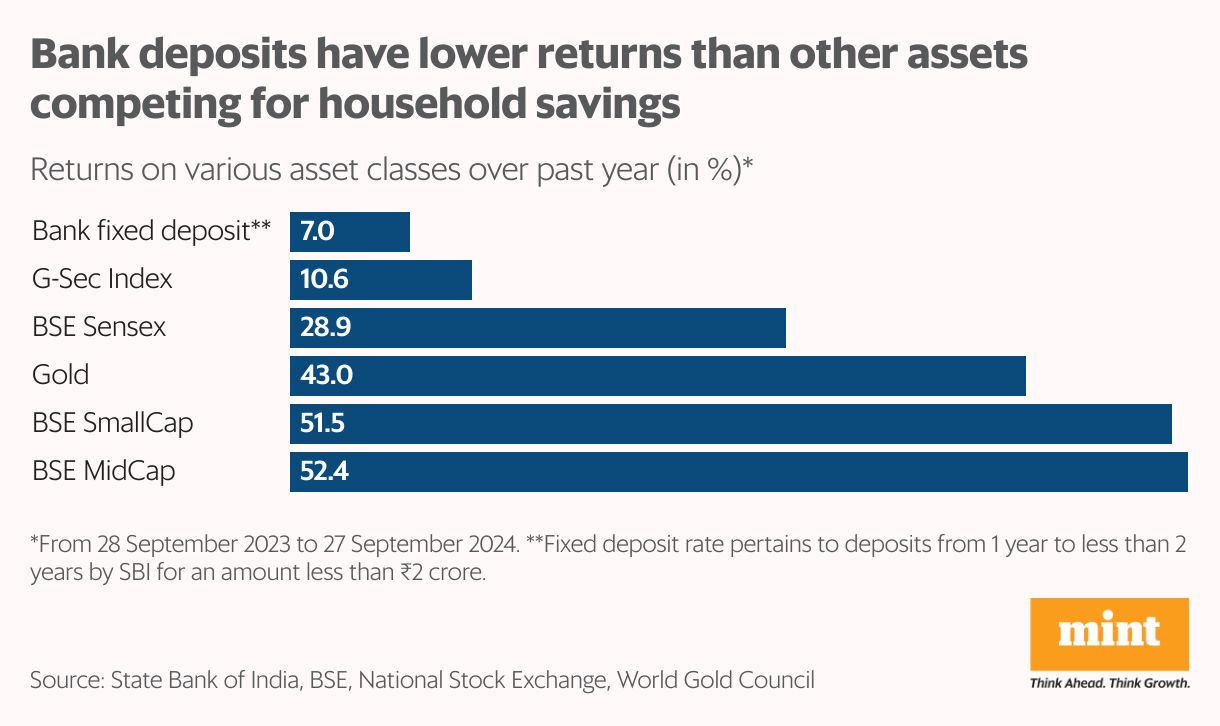

Third, a rate cut could further reduce the attractiveness of bank deposits. Banks are already having to use novel ways to attract deposits: innovative product launches, partnering with aggregators, and targeting new segments like content creators and gig workers. Strategizing to get deposits has become necessary as competing assets are racing ahead. Given robust credit growth, banks will face some tough choices if monetary easing starts.

More here | If deposits are stuttering, how will banks manage the credit boom?

In the event of a rate cut, if banks lower both lending and deposit rates, they risk losing deposits, forcing them to rely on higher-cost borrowings, which would increase their funding costs. Alternatively, if they reduce lending rates but raise deposit rates to retain customers, their net interest margins will shrink. If they choose to keep both lending and deposit rates high to protect margins, monetary policy transmission would be hampered. The RBI is likely to weigh these trade-offs carefully as it formulates its next move.

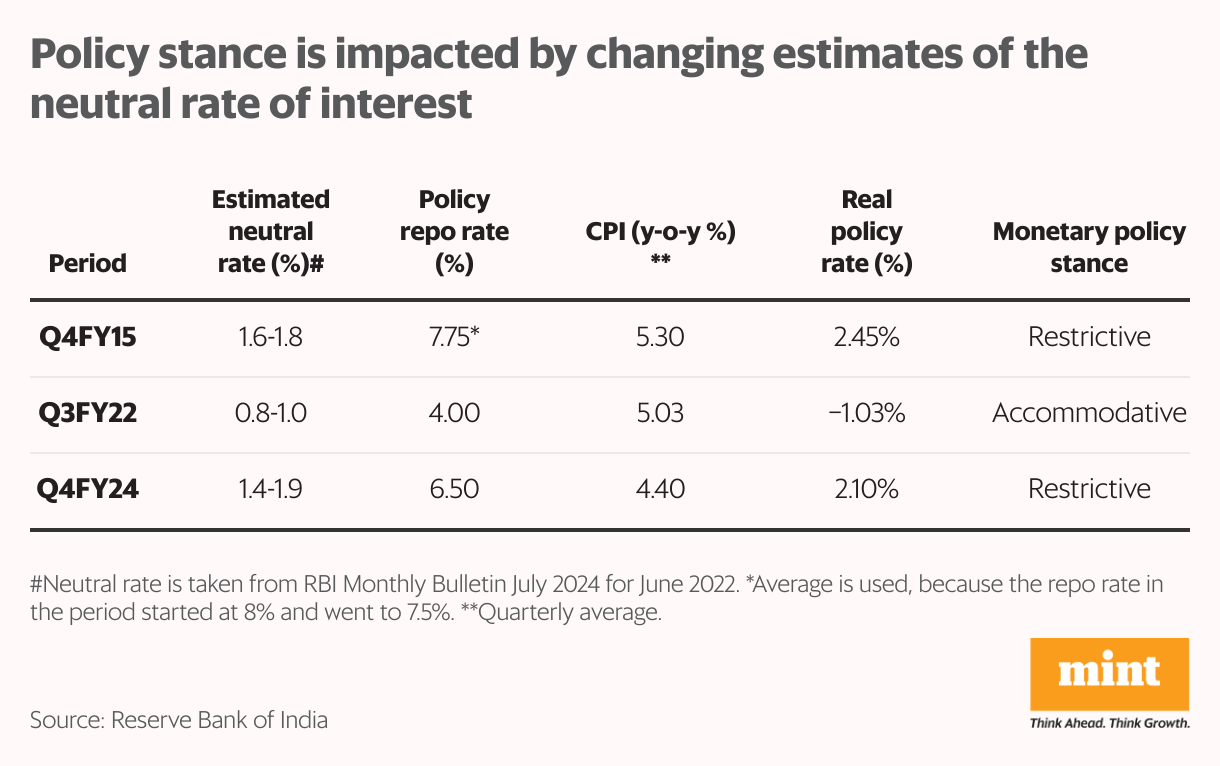

Neutral interest rate

Central banks also keep an eye on the “neutral" interest rate, at which the economy operates at potential output and inflation is stable. A real interest rate (repo rate minus inflation) exceeding the neutral rate (as it does now; see chart) is considered to be restrictive for the economy.

This leaves less space to raise interest rates further, and it would justify holding rates for now. But going forward, structural changes in savings behaviour (such as rising incomes) could lower the neutral rate, while investment optimism could push it up—a balance that makes its impact on the policy decision tough to predict. While the RBI governor describes the neutral rate as a “theoretical construct", the fact that RBI regularly updates it shows it’s important enough to be tracked. What action the RBI takes will depend, to some extent, on how it sees the future path of the neutral rate.

The author is an independent writer in economics and finance.