Data explainer: Decoding the dissent of RBI’s doves, in 5 charts

")

Summary

Jayanth R. Varma’s and Ashima Goyal’s tenures as members of the monetary policy committee are set to end after the August meeting. But they have sparked a debate with their dissenting votes in favour of a rate cut.

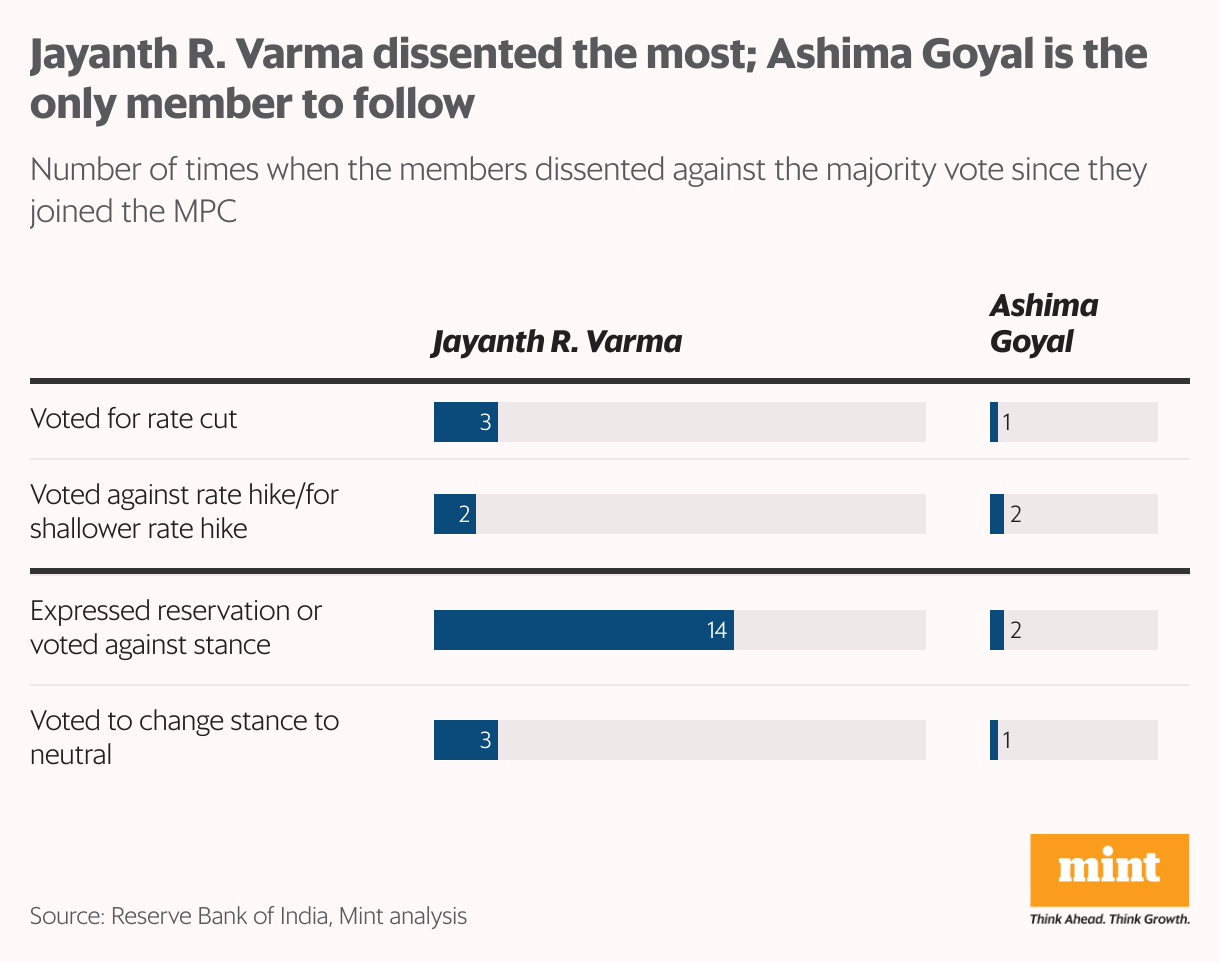

NEW DELHI : Jayanth R. Varma joined the Reserve Bank of India’s (RBI's) monetary policy committee (MPC) in October 2020, and in his very first meeting, he dissented. Ashima Goyal, who was appointed at the same time, has since emerged as the only other dissenting voice, albeit not as often as Varma, who was a hawk initially, but turned dovish in the middle of 2022. Goyal has always had a dovish tilt.

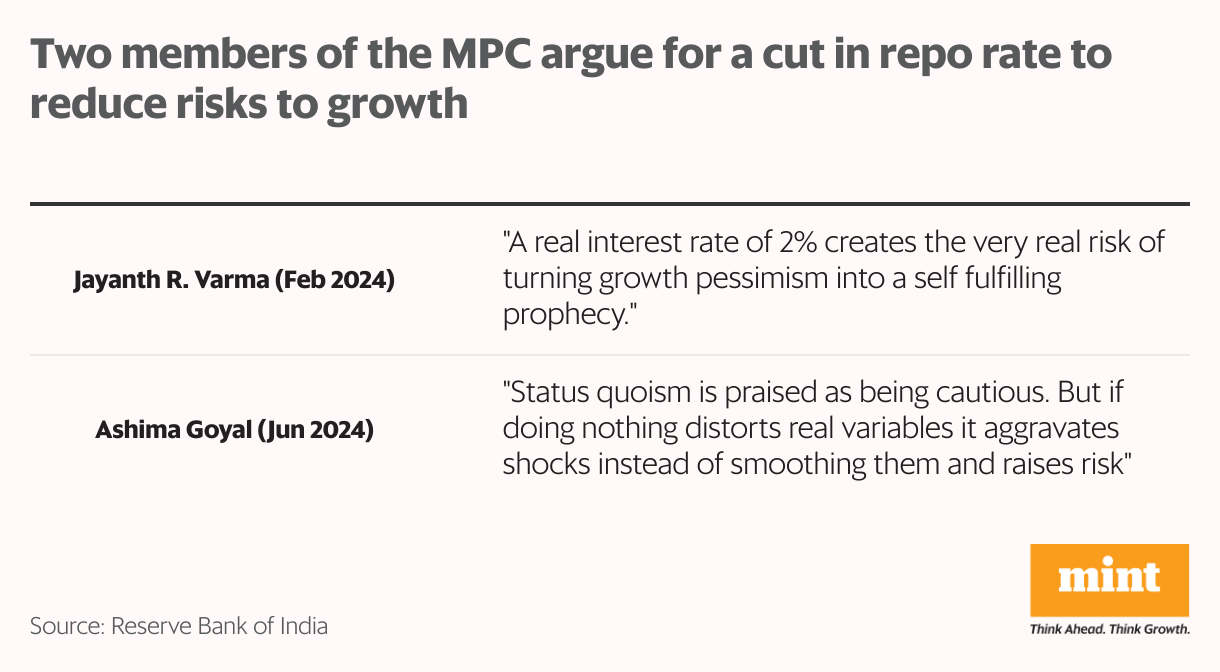

Both these members, whose tenure on the panel will end after the August meeting, have sparked a debate about whether staying with a tighter monetary policy will end up hurting growth, especially since inflation has now largely eased. Varma had been voting for a reduction in the benchmark repo rate since February, but with Goyal also joining in earlier this month, his case has grown stronger. Both invoked high real interest rates to argue their point, as per the minutes of the latest meeting, while the other four members voted to keep the repo rate unchanged at 6.5%.

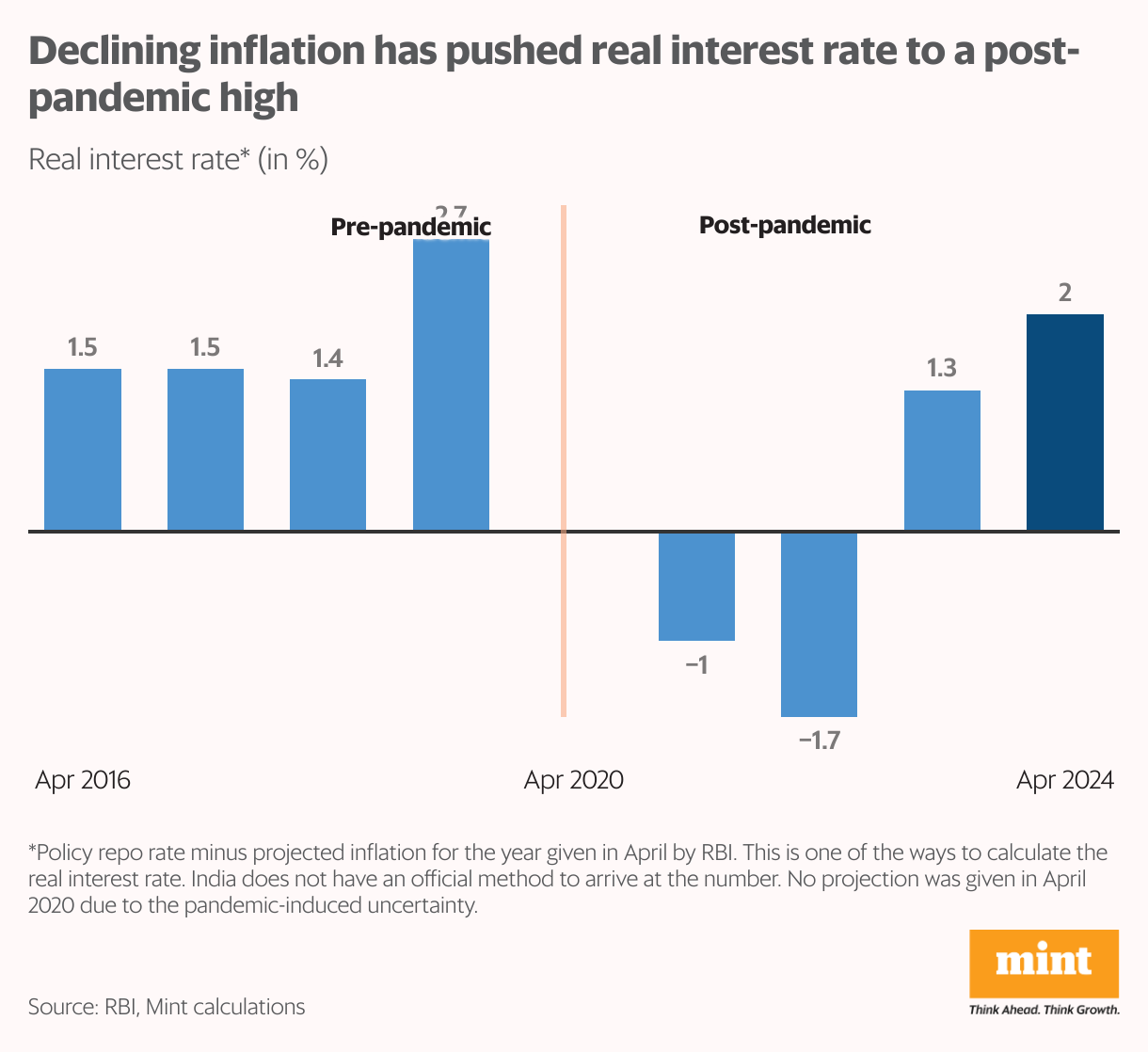

Real interest rate refers to the inflation-adjusted cost of borrowing or return on investments. There is no official definition, or an ideal level. The common definition (i.e. the gap between the policy repo rate and the expected inflation), would indeed put it quite high at 2%, the highest in the post-pandemic era and the second-highest since 2016. Goyal feels a real interest rate above 1% will hurt growth; Varma says 1–1.5% would be sufficient to glide inflation to the target of 4%.

Also Read: Shining GDP overshadows slower GVA: Decoding growth numbers in 7 charts

Growth gambit?

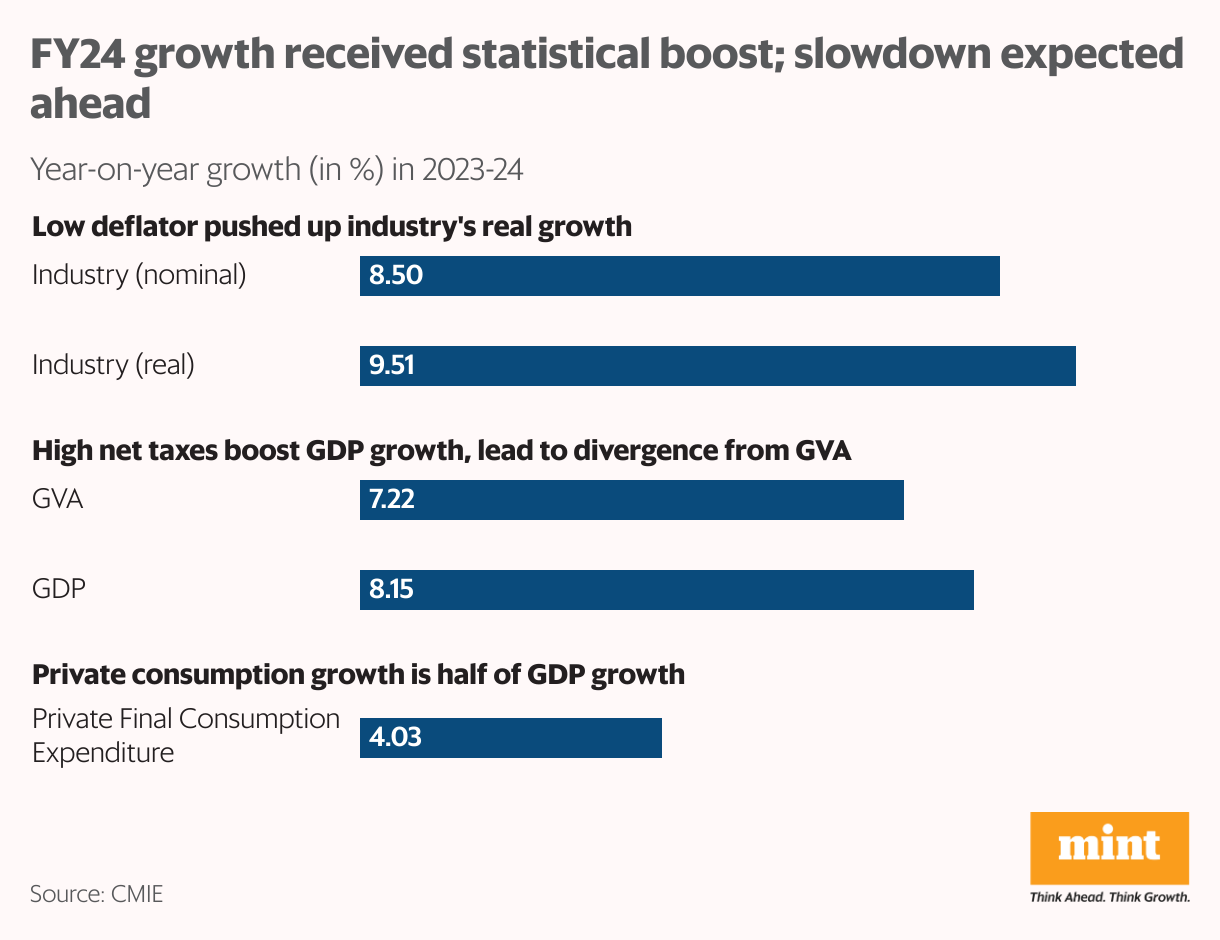

India’s gross domestic product (GDP) growth is expected to slow down to 7.2% this year from 8.2% in 2023-24. But the better-than-expected growth in 2023-24, too, came on the back of a statistical boost from high net taxes and a low deflator. On top of it, private consumption remains weak.

Doves—those favouring an interest rate cut—believe that the slower growth would mean that India’s growth could miss its potential in 2024-25 and 2025-26 if monetary policy is not fine-tuned. Status quoists on the MPC still believe India’s growth prospects are promising.

The argument that the RBI may be risking growth by keeping the status quo came as early as February 2023, when Varma wrote that the majority MPC view was becoming complacent about growth, after being complacent about inflation a year prior. While the growth in 2023-24 did not turn out to be “unacceptably low" as Varma had warned, it was certainly not as impressive as the headline numbers suggested.

Once bitten, twice shy

There are several factors—and recent experience—that could be keeping the other members of the MPC cautious about inflation. When the panel had to loosen the monetary policy during the pandemic, it looked over the rising price pressures, which eventually resulted in inflation shooting past the upper tolerance limit of 6% in 2022-23. The RBI was not alone in perceiving inflation as “transitory"; central banks around the world did so. But the failure to contain inflation within the range for three consecutive quarters did result in the RBI having to explain to the government the reasons for its failure and its proposed corrective steps.

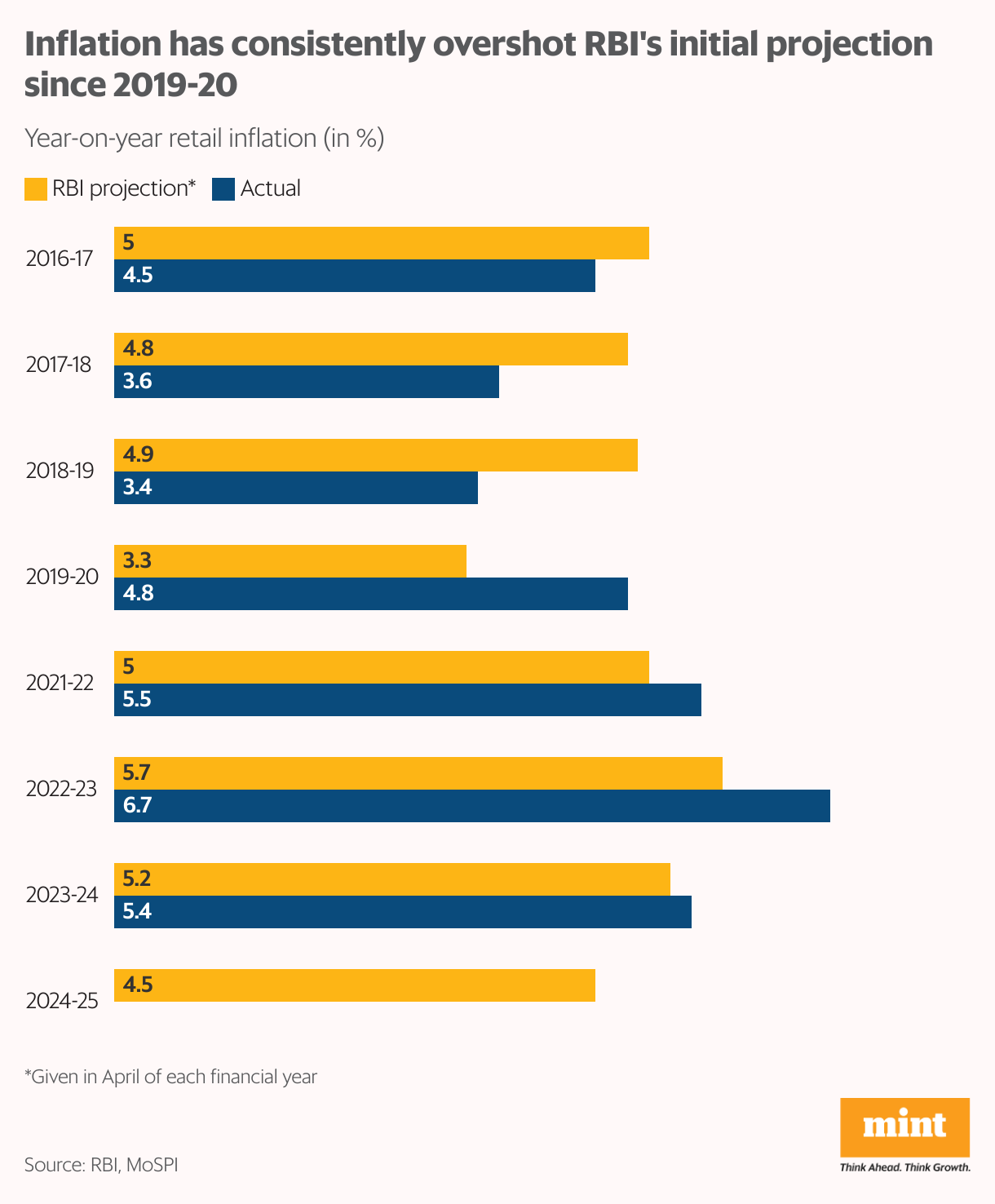

Varma and Goyal are arguing on the basis of the RBI’s expected 4.5% inflation in 2024-25, but for the past few years, actual inflation has overshot the RBI’s early projections, a Mint analysis shows. Moreover, the climate crisis has also made the trajectory of food inflation particularly difficult to track, adding to uncertainty, and driving caution.

Also Read: The spoilers that lie ahead: What ails India’s rosy growth story

Pivot incoming?

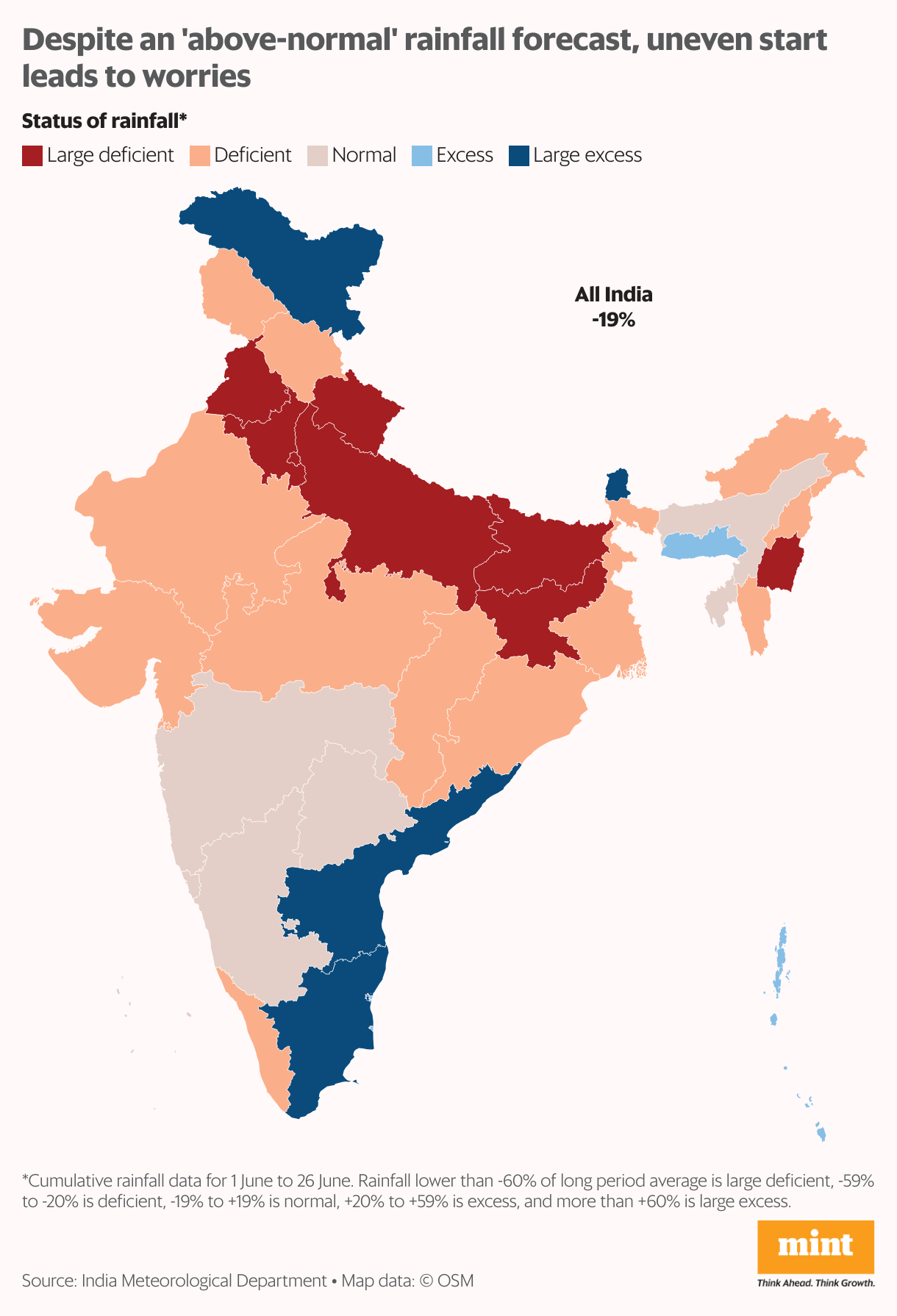

Despite cooling inflation, those who voted for a status quo, including RBI governor Shaktikanta Das, see elevated food inflation risks and a possible spillover onto core inflation and household inflation expectations. Food inflation will depend on the monsoon, which is expected to be “above normal". But the rainfall so far has been uneven—and likely below normal in June. This could delay sowing and potentially push prices up.

Yet, the doves believe that even with slight easing, the real interest rate would still be high enough to contain inflationary risks, and the status quo could end up doing more harm than good. In a note last week, economists at Nomura explained this view by saying that headline GDP growth was “exaggerated" in 2023-24, and while risks on food inflation are always hard to predict, “they have indeed not had any adverse spillovers". A rate cut is expected only from October as the internal MPC members may hold until slower growth forces their hand, Nomura said.