Rupee has put RBI between a rock and a hard place

")

The RBI is facing contradictory expectations, with the government preferring a stronger currency, economists and policymakers arguing for a market-driven value of the rupee, and the impossible trinity limiting the options.

A sharp depreciation of the rupee in recent months may have addressed concerns raised by economists and policymakers who argued for allowing the currency to its own level in the markets. At the same time, a weaker rupee does not sit too well politically as governments often prefer a stronger currency. This puts the Reserve Bank of India (RBI) between a rock and a hard place: whether to defend the currency against the dollar or to let it move freely.

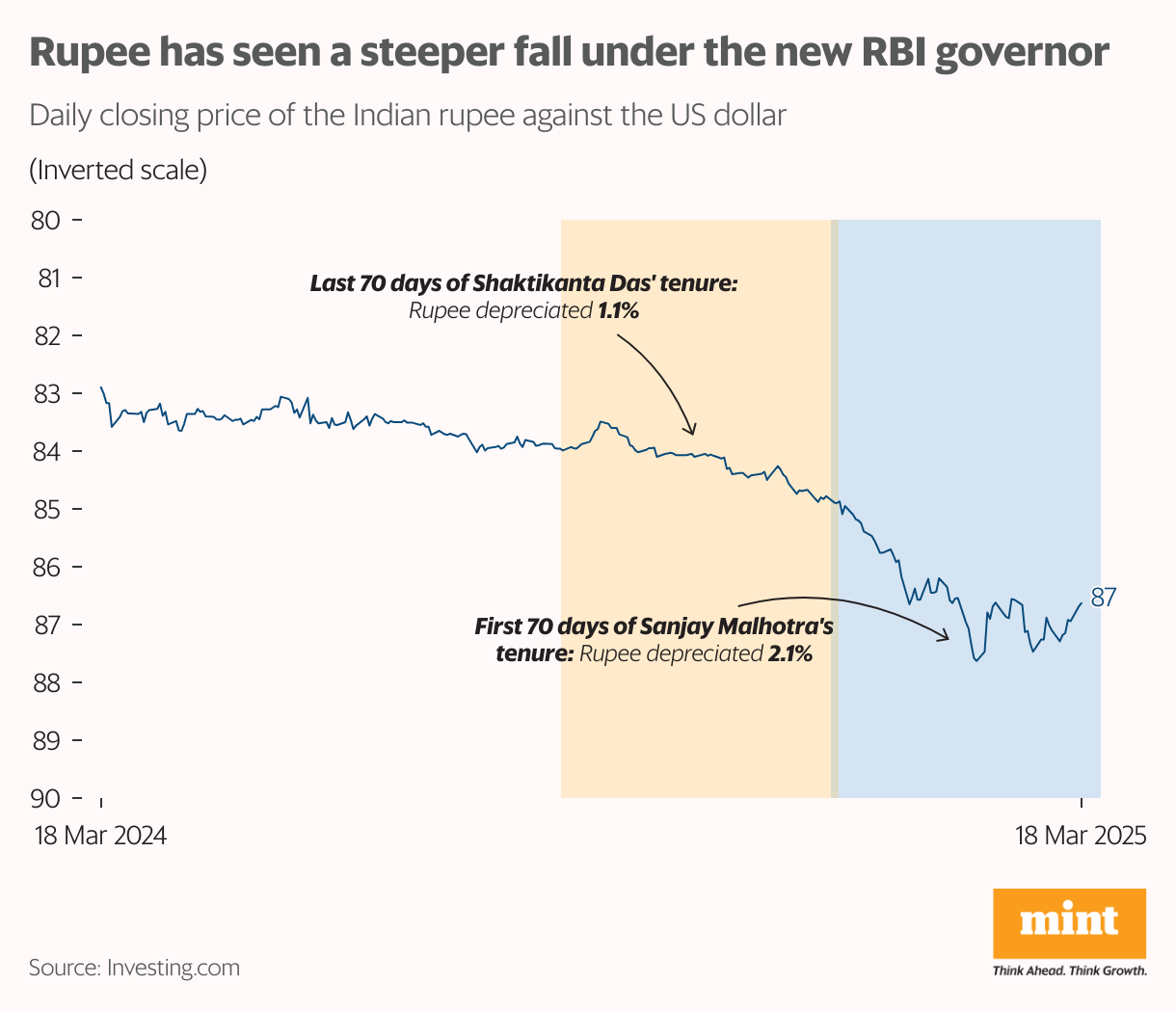

India, under the previous RBI governor Shaktikanta Das, witnessed exchange rate stability, which, market watchers believe, changed after the new governor, Sanjay Malhotra, took charge. A Mint analysis of the rupee’s movement shows that the rupee depreciated 1.1% in the last 70 days of Das’ tenure, while it depreciated nearly double (2.1%) during the first 70 days under Malhotra. However, this trend may change.

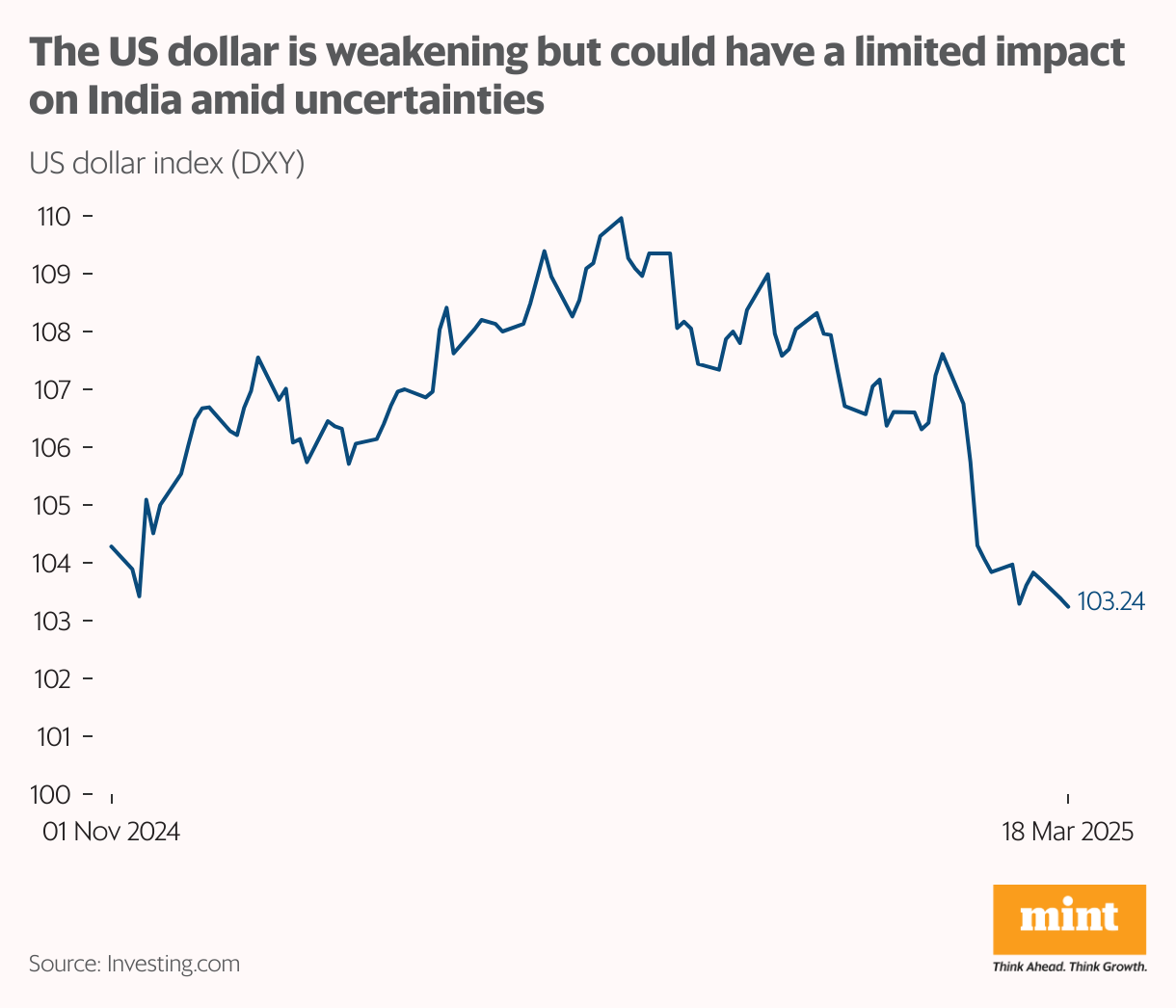

Last week, Mint reported quoting officials that the government does not want the rupee to depreciate too much and the RBI may continue to defend the currency, continuing the trend of curbing volatility. The recent weakening of the dollar amid recession fears in the US may offer a cushion to the rupee, thus reducing the need for market intervention, but the impact could be limited. “The uncertainty about what Donald Trump may do is worse than what he is actually doing. As long as there is uncertainty, we will continue to see volatility," says Madan Sabnavis, chief economist at Bank of Baroda.

The ‘impossible trinity’

On top of the divergent view on the rupee’s movement, the RBI is also facing the “impossible trinity", which means the RBI cannot simultaneously have an independent monetary policy, maintain a stable exchange rate and have free flows of capital at the same time. “When you try to maintain the rupee at a certain level, you will have to sell dollars and buy rupees. This tightens the liquidity," explained Radhika Piplani, chief economist at DAM Capital.

Currently, the RBI is easing the monetary policy against the backdrop of low inflation and injecting liquidity into the system. As such, currency management has to be sacrificed. “Last year, when the RBI controlled the monetary policy to prevent inflation, it ended up with a liquidity squeeze while managing the currency," Piplani added.

While India currently has massive forex reserves of $654 billion, despite sharp depletion from $705 billion since the end of September 2024, the RBI may find it tricky to defend the rupee, given the liquidity requirements against the backdrop of a slowing economy.

“A deficit of around $20-25 billion in India’s balance of payments in FY25 is expected due to a sharp slowdown in capital inflows. This is despite the current account deficit remaining low at 0.8% of GDP. The large negative BOP has increased the reliance of the market on the RBI to supply dollars," said Gaura Sengupta, chief economist at IDFC First Bank.

According to Nomura, since India is largely domestic demand-driven, attracts growth-sensitive foreign capital and has less currency-induced inflation pass-through, allowing the currency to weaken is a prudent move.

Currency conundrum

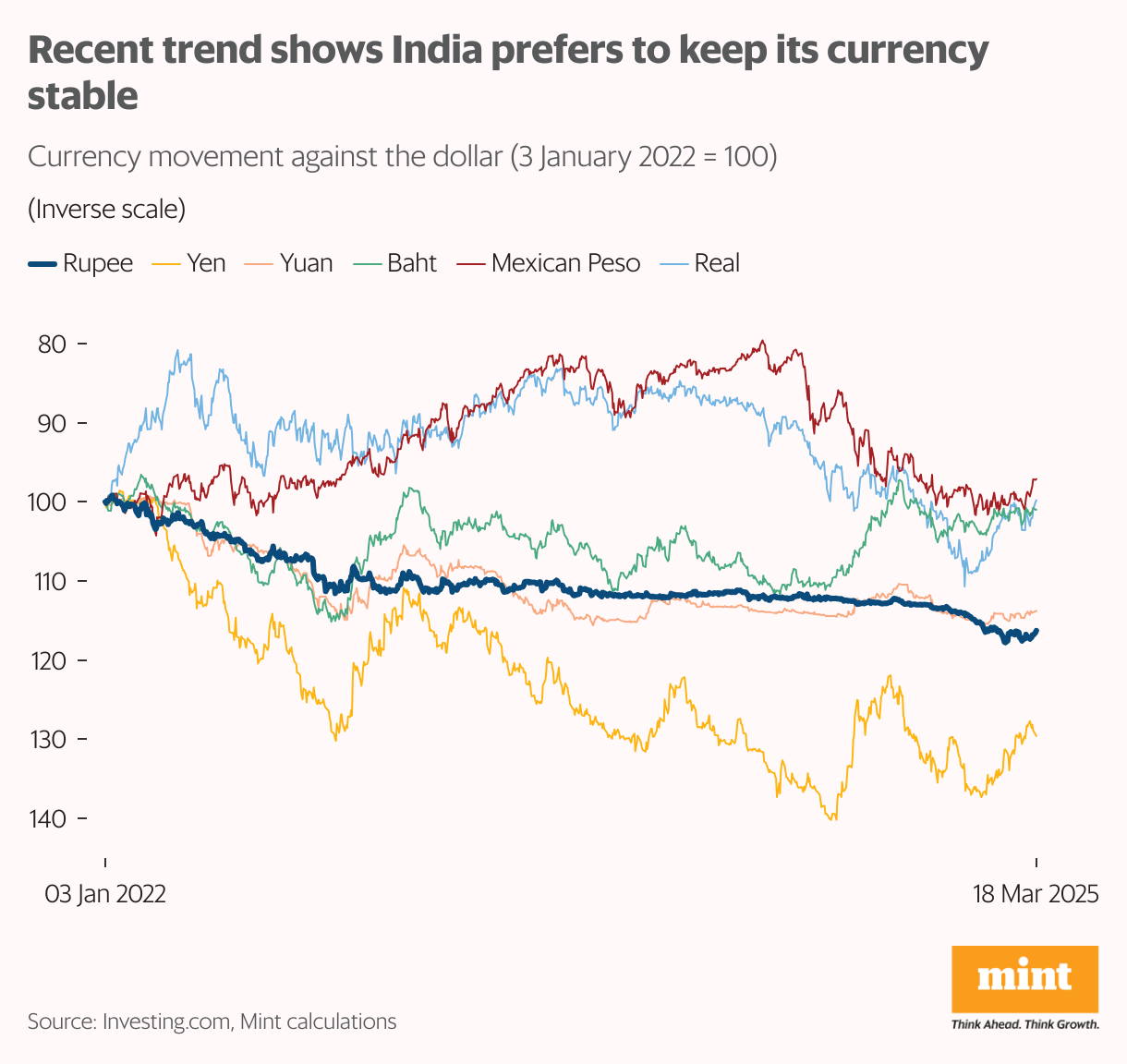

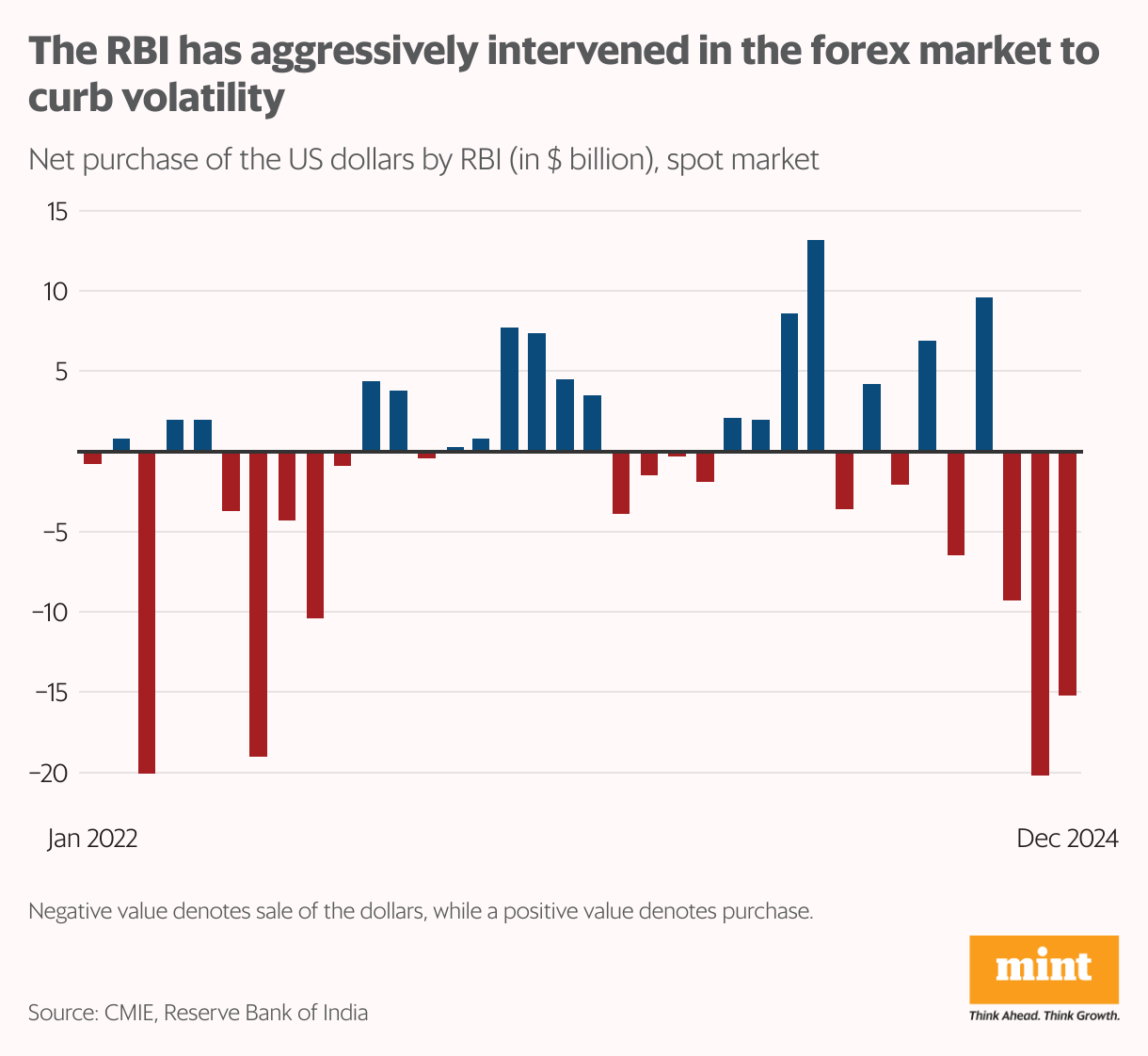

While the ‘impossible trinity’ may be a limiting factor, the recent trends show the RBI’s inclination to keep the rupee stable. A Mint analysis of currency data from select emerging market economies shows that the Indian rupee was quite stable relative to its peers, neither having depreciated much, nor appreciated. While exchange rate stability is desirable, economists argue that it should come due to the outcome of the market forces, which has not been the case in India. The RBI has aggressively intervened in the foreign exchange markets by both selling and purchasing US dollars.

This led to the International Monetary Fund reclassifying India’s exchange rate to ‘stabilised arrangement’ from ‘floating’ in December 2023. The constant intervention had made the rupee overvalued by 8% (this may have come down to about 5% by some estimates due to the sharp depreciation in recent months). However, there is still some room for correction, and aggressive intervention in the markets may lead to problems in the economy.

Also read | Why RBI dialled up dollar sales in the forward market last quarter

In an Ideas for India article, Radhika Pandey (National Institute of Public Finance and Policy), Ila Patnaik (Aditya Birla Group) and Rajeswari Sengupta (Indira Gandhi Institute of Development Research) argue that RBI’s interventions lead to private sector taking on greater dollar exposure and make them unlikely to hedge it. If a large number of companies take such risks without much hedging (due to the high cost), it could pose problems for the economy. According to the Financial Stability Report published by the RBI in December 2024, nearly 35% of the total debt under external commercial borrowings (ECBs) was unhedged.

A similar view was echoed by former RBI governor Duvvuri Subbarao. “If the RBI intervenes to stabilize the exchange rate against the fundamentals, market participants will outsource their risk management to the RBI," Duvvuri Subbarao told Bloomberg in an interview in January.

The RBI will have to walk a tightrope to address the contradictory concerns in the economy, especially given the widespread expectations of volatility due to the trade war.