Economy

Economy

The spoilers that lie ahead: What ails India’s rosy growth story

")

Summary

- The election outcome suggests a disconnect between the optimism about growth data and the ground reality. Here are four factors that the new government would do well to take note of.

The new government starts off on a firm economic footing, thanks to three years of strong growth and a restrained fiscal position. But, as the unexpected election outcome suggests, there seems to be a disconnect between headline growth rates and ground reality—and therein lie the risks.

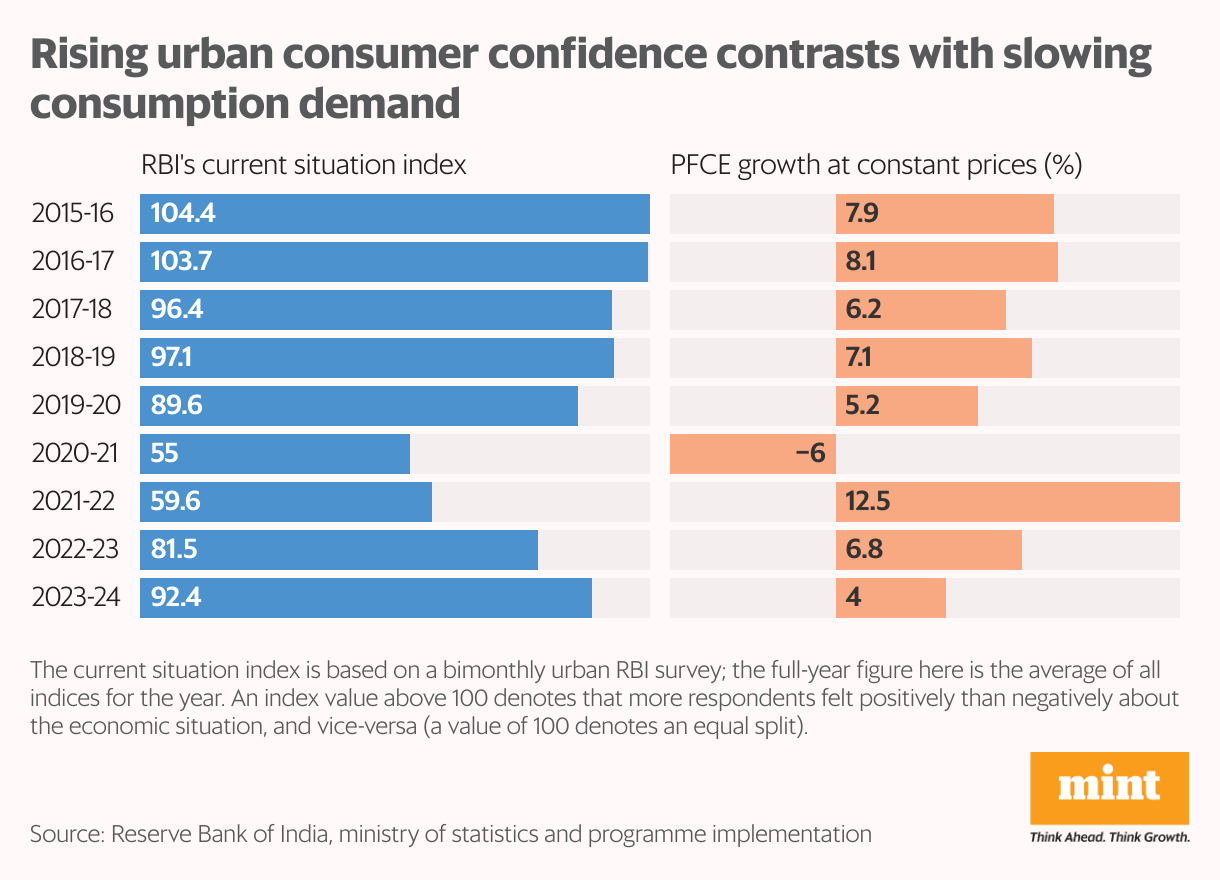

Consumption demand, which accounts for 56% of India’s GDP, is a good starting point. Growth in private final consumption expenditure (PFCE) has slowed in the past two years. Rural consumption was hit by inflation and low wage growth, and it was the urban consumers who kept the spending ship afloat. No wonder, the Reserve Bank of India’s consumer confidence index is back at pre-pandemic levels: it is based on an urban survey.

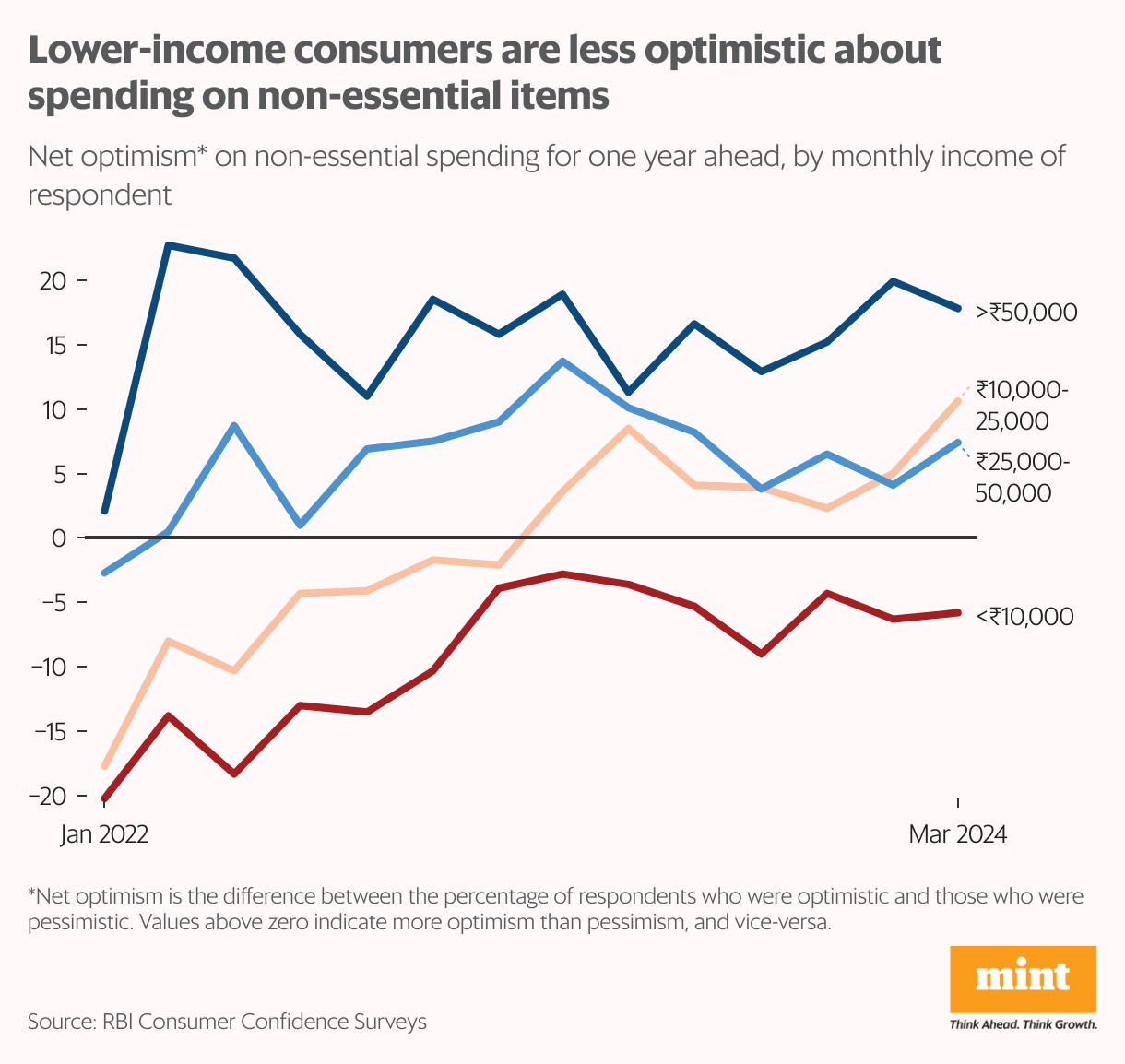

But digging deeper into the data made some fault lines apparent. The survey separates essential and non-essential spending. The trend is directly linked to income: respondents in the lowest income group were pessimistic about future discretionary spending despite the post-pandemic growth revival, even as the highest earners remained buoyantly optimistic. In the middle-income group, optimism took a few months longer to show up than for high-earners.

The pessimism of the poor is more acute in metro cities: last year, an average of 24% of metro city respondents earning less than ₹10,000 a month expected to increase their spending, against 44% of similar non-metro respondents. Intuitively, that makes sense—metro life is more expensive, and offers less family support. The poorest are likely to be in unskilled, informal jobs and, therefore, the most vulnerable to financial shocks.

Miserable metros

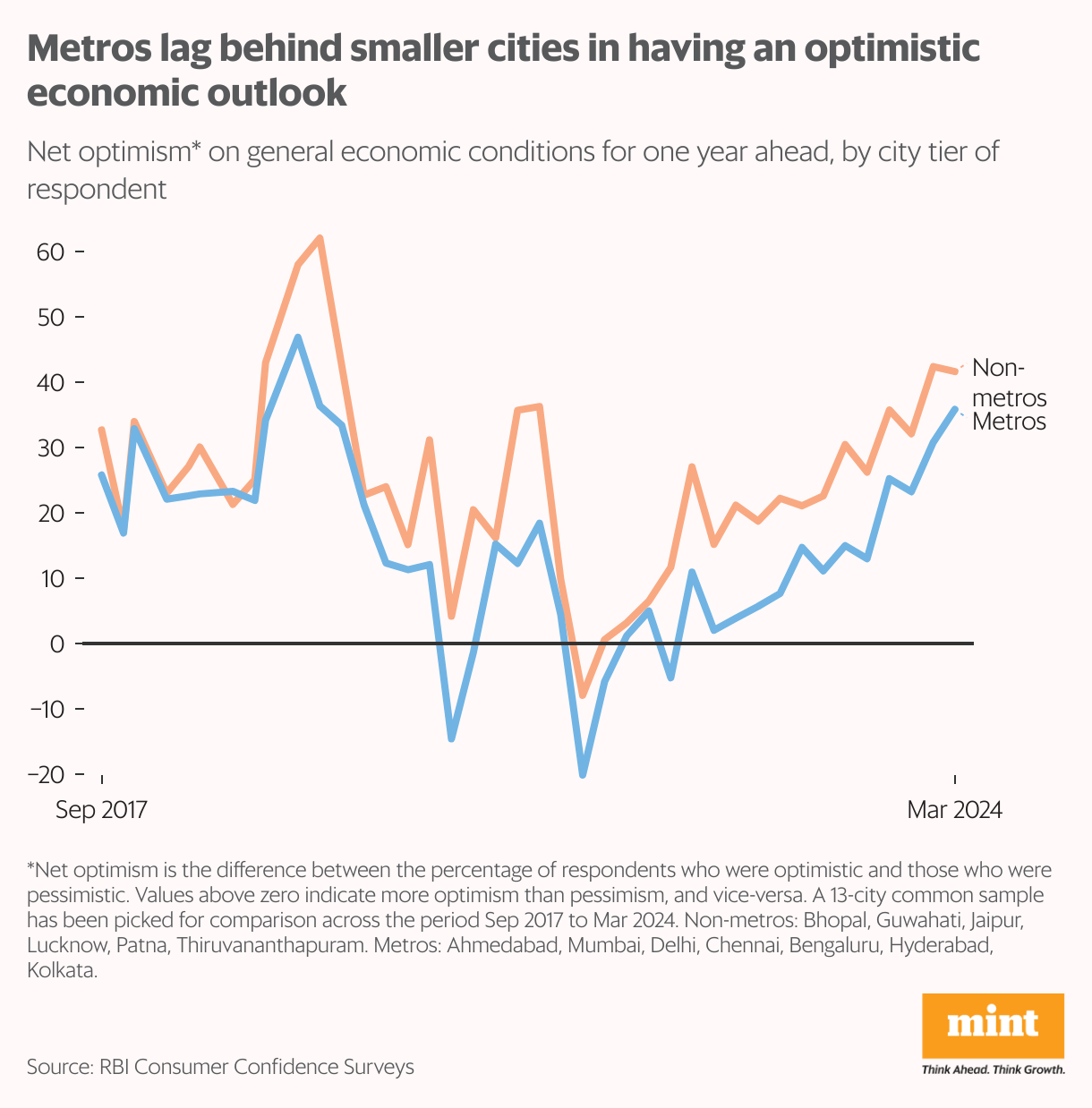

Three Indian metros—Mumbai, Delhi and Bengaluru—are among the world’s top 50 startup ecosystems, while Chennai, Pune and Telangana are emerging stars (Global Startup Ecosystem Report 2023 by research firm Startup Genome). Yet the RBI survey shows that metros are less optimistic than Tier-II cities about their future economic outlook.

One possible reason is the close link between employment prospects and economic optimism. Smaller cities have experienced a boom in jobs and incomes, driven by infrastructure improvement, digitization, e-commerce, and expansion of bank loans and credit/debit cards. Not surprisingly, between March 2022 and March 2024, the share of non-metro respondents with an improved employment outlook rose from 25% to 45%. The corresponding rise for metros was muted.

The solution? A general need is to revitalize metros and transform them into clean, green and safe cities, which attract investment and jobs. City-specific problems (air quality in Delhi, traffic in Bengaluru, overcrowded trains in Mumbai) will also need to be addressed.

Entrepreneur, not by choice

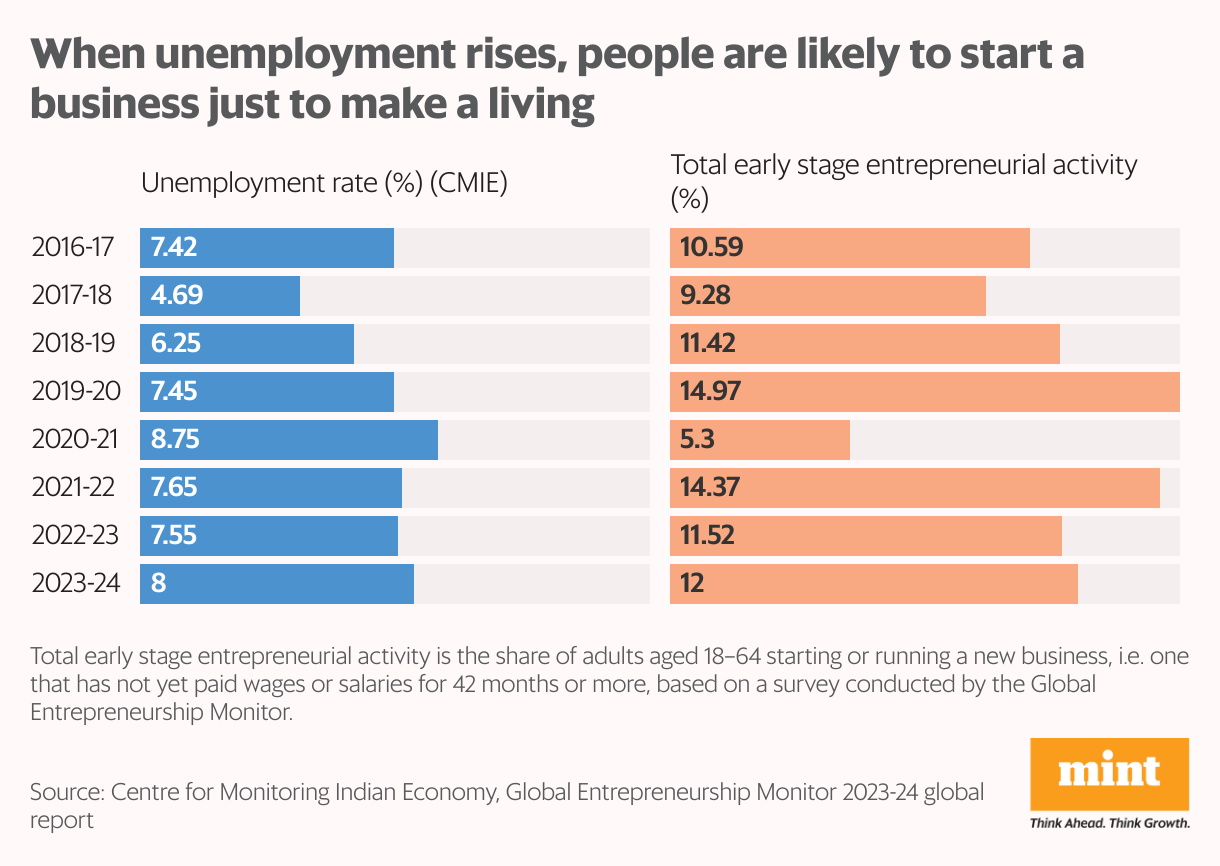

India has a strong entrepreneurial vibe. According to the Global Entrepreneurship Monitor, one in five working age adults intend to start a business in the next three years. These usually fall into the category of medium, small and micro enterprises (MSMEs), which contributed 29% to India’s GDP in 2021-22 and 45% to its total exports in 2022-23. Over 99% of MSMEs were micro enterprises, most of which were proprietary concerns. In other words, the small shops and factories that dot the country fuel economic dynamism. Entrepreneurs create jobs, spur local innovation, and boost production.

The problem is that entrepreneurship in India arises out of necessity rather than opportunity. Nearly 88% of the respondents in the Global Entrepreneurship Survey 2022-23 indicated that the prime motivation for starting a business was the need to earn a living, given a scarcity of jobs. This is quite obvious from recent data: periods of unemployment see a rise in entrepreneurial activity.

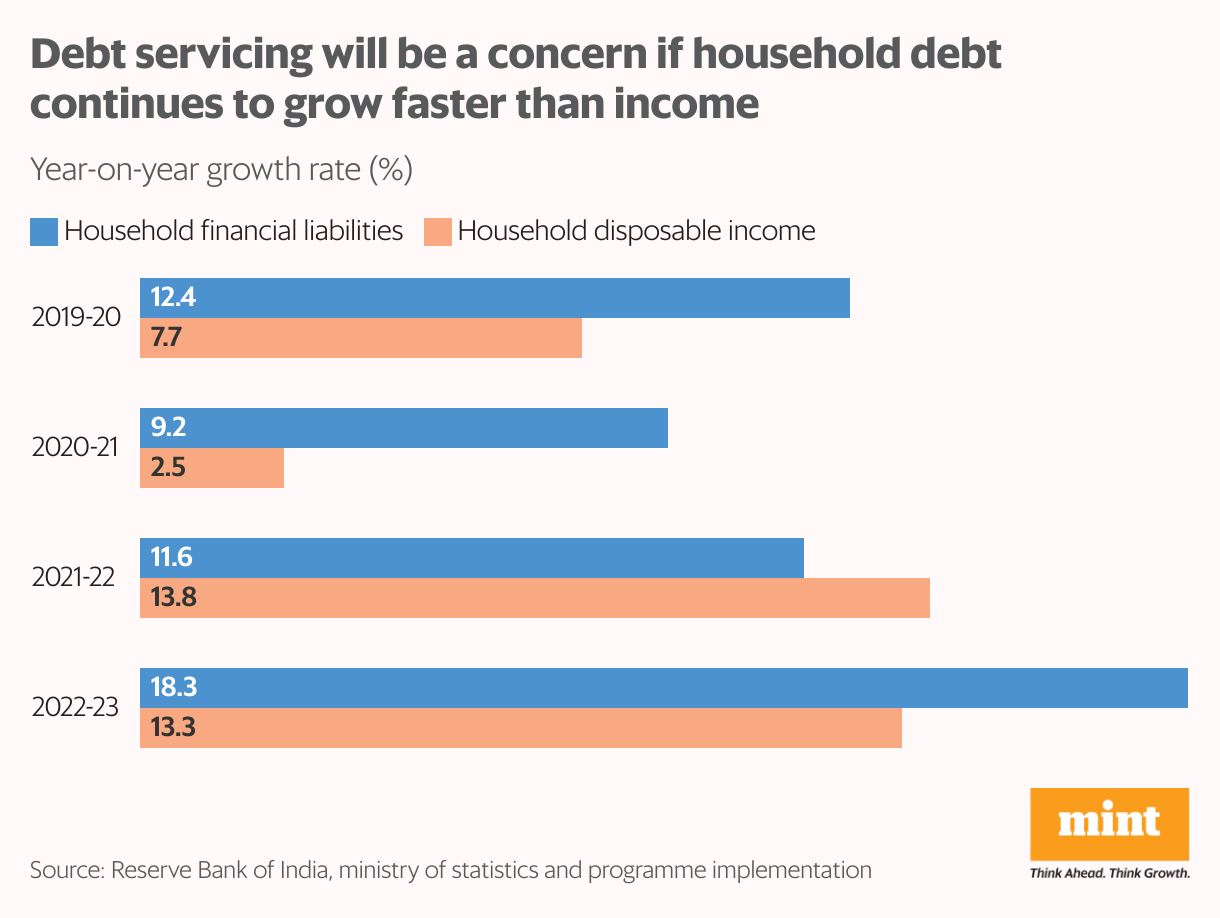

Borrowing boom

Lastly, India is turning into a nation of spenders. The reasons for taking loans is a bigger concern than the amount of debt. A survey by Paisabazaar showed that 21% of personal loans taken on its platform during January-June 2023 were for travel expenses, and 31% for home renovation.

Demography, digitization and development could be driving this trend of increasingly casual borrowing. Millennials and Gen-Zs are quick to borrow to fulfil their aspirations. Over 70% of the borrowing by lower-middle-class individuals in 2023 was by 18- to 39-year-olds (“How India Borrows" report). The growth of digital ecosystems enables easy credit and facilitates app-based loans.

A rise in household debt is natural when the unbanked are brought into formal financial systems. But if liabilities grow faster than incomes, servicing debt becomes an issue, and we run the risk of eroding the confidence of the most important consumer: the Indian household.

The author is an independent writer in economics and finance.