War for deposits: Banks’ biggest headache now coming for investors?

")

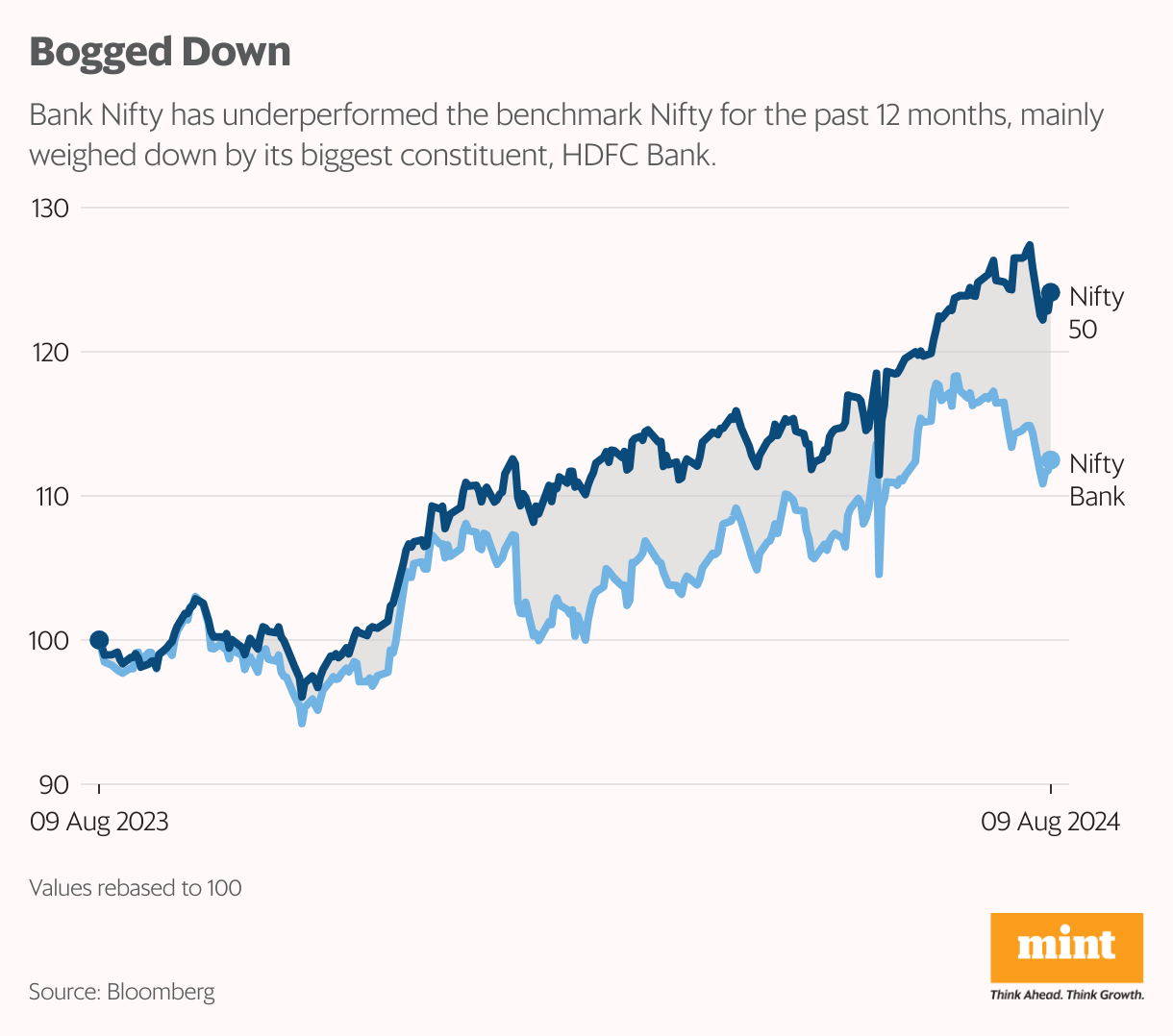

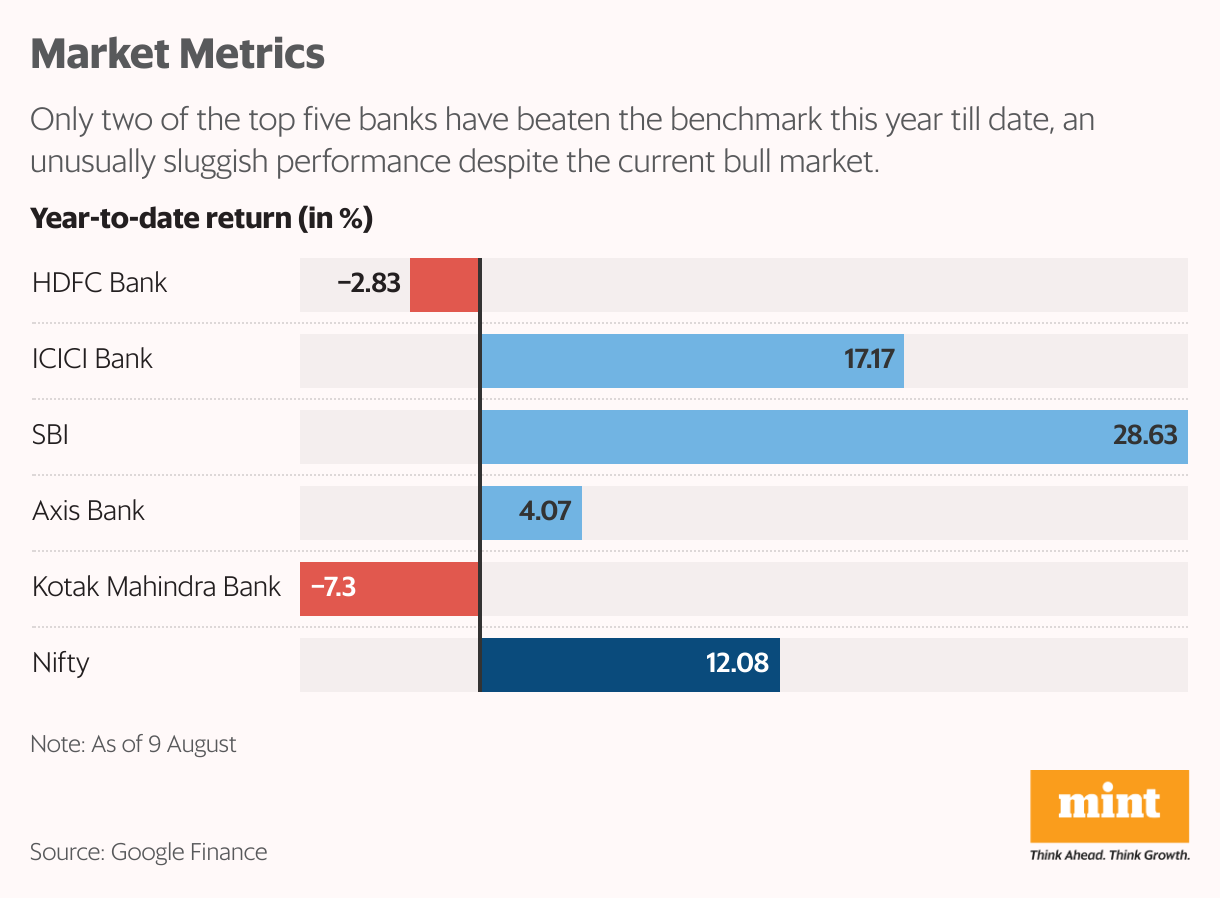

- Bank Nifty has been underperforming the benchmark Nifty by a wide margin—perhaps the clearest indicator of which way the wind is blowing for lenders. They are grappling with systemic challenges, evident in their first quarter results. How should investors approach the sector at this juncture?

New Delhi: For more than a year, one of the most fundamental correlations of the Indian equity market has gone awry—Bank Nifty has been underperforming the benchmark Nifty by a wide margin. For the market to maintain equilibrium, both these important gauges have to move in tandem. Any divergence is indicative of lopsided momentum, which by definition is unsustainable.

Now the biggest culprit behind Bank Nifty’s underperformance has been its largest constituent by weightage—HDFC Bank.

But even beyond this behemoth, Indian banks are currently grappling with some considerable systemic challenges, all of which were evident in their recent results.

Dial D for Deposits

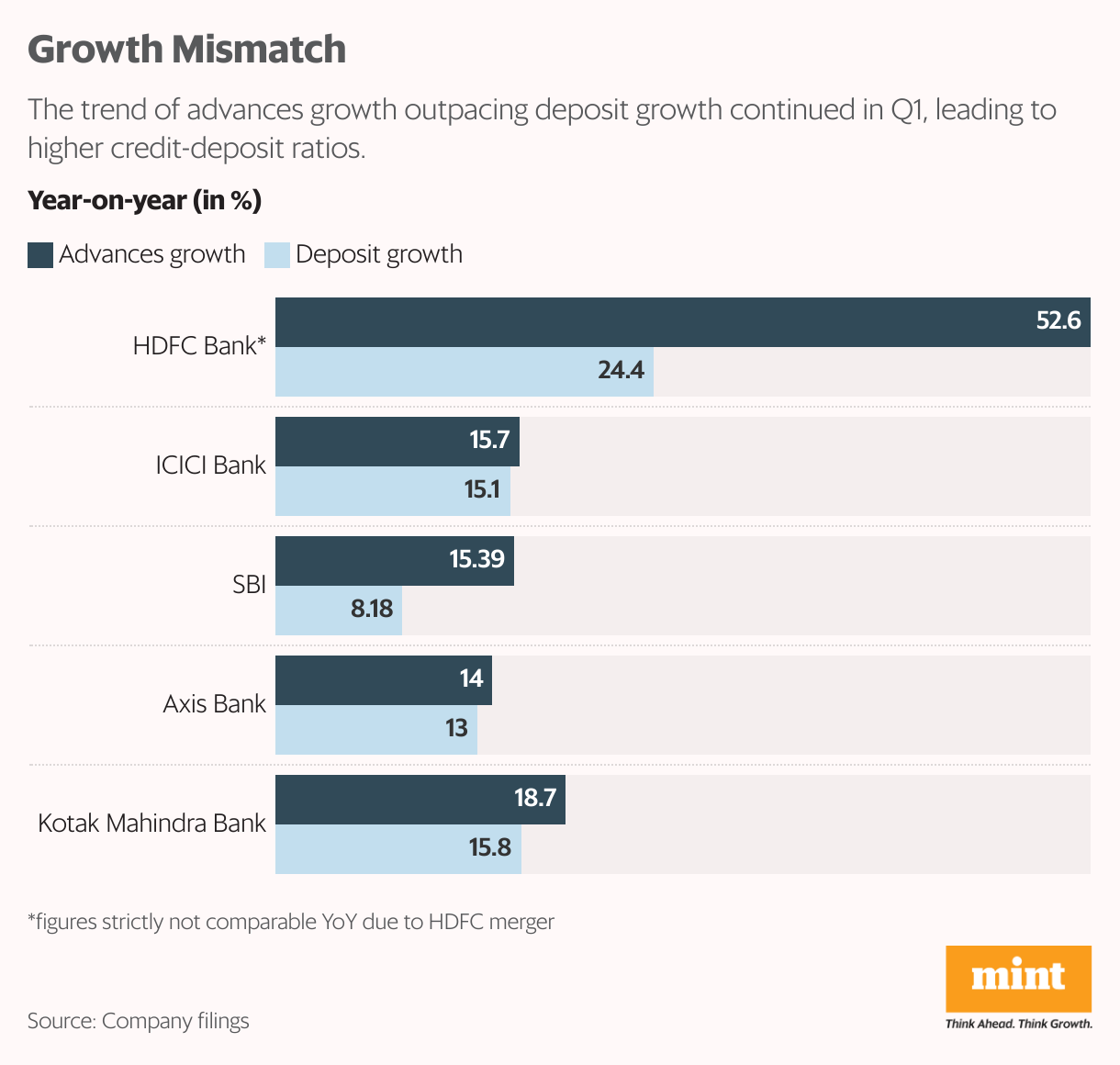

When the country’s largest private sector bank as well as the biggest public sector lender are struggling for deposits, surely some system-wide issues are at play.

HDFC Bank reported zero sequential growth in deposits during the first quarter (Q1) of 2024-25 at ₹23.8 trillion, while that of State Bank of India (SBI) dipped 0.3% to stand at ₹49 trillion.

“Most of the banks witnessed growth moderation along with some uptick in credit cost in Q1," Christy Mathai, fund manager—equity, Quantum AMC (Asset Management Company), told Mint. “Deposit mobilization remains the key focus for the banks and incrementally, the cost of deposits has moved higher than yield increases, impacting the net interest margins (NIMs). Draft LCR norms, if implemented, will impact the liquidity further," he added.

The Reserve Bank of India (RBI), last month, issued draft guidelines for management of liquidity coverage ratio or LCR. It refers to the proportion of high-quality liquid assets (HQLA) like cash and government securities that banks must hold to ensure they can meet their short-term obligations. Under the new draft norms, banks will be required to increase the liquidity cover for ‘stable deposits’—those from which withdrawals are infrequent—from 5% to 10%.

")

For ‘less stable deposits’, for example those held by customers with internet and mobile banking facilities, the required liquidity cover will rise from 10% to 15%.

The draft guidelines, slated to be implemented from 1 April 2025, are anticipated to lower banks’ LCR by around 11-20 percentage points. This, in turn, would necessitate banks shoring up deposits and increasing their HQLA holdings.

However, Indian banks are already facing their worst deposit crunch in two decades, with even the regulator RBI expressing concern.

As on 28 June, bank deposits had grown 11.1% year-on-year, lagging credit growth of 17.4%. This has forced banks to raise deposit rates to lure customers who are preferring other investment avenues like stocks and mutual funds.

The topic of lagging deposit growth loomed large during this earnings season.

“I know that the most important part of our strategy is deposits. And are we happy with the kind of numbers that have come about? Not really. It has fallen short of our expectations," HDFC Bank managing director and chief executive officer (CEO) Sashidhar Jagdishan said at its post-earnings concall.

HDFC Bank saw some significant outflows from current accounts, which contributed to the muted growth. However, the management said it remains committed to pursuing deposit-led credit growth and expects the pace of deposit accretion to pick up in the coming quarters.

Crucially, HDFC Bank is not looking to get into a ‘rate war’ to attract depositors. Instead, it expects to leverage the strength of its wide branch network and enhance customer engagement. Moreover, the bank is looking to convert mortgage customers into primary banking customers and further deepen relationships with existing corporate clients to ensure the building of its deposit franchise.

But will depositors be enticed by ‘enhanced service delivery’ at a time when the stock market is easily delivering far higher returns?

This question is clearly keeping managements awake at night, and not just at HDFC Bank.

“Challenges of low-cost deposit continue with savers turning into investors, deploying money in high yielding capital market products...," Kotak Mahindra Bank’s group chief financial officer Devang Gheewalla pointed out at the Q1 conference call.

The lender’s total deposits stood at ₹4.47 trillion as of 30 June, down 0.3% compared to the preceding quarter.

Second-Order Effects

Adventure is the life of commerce, but caution…is the life of banking," RBI governor Shaktikanta Das said at a conclave in Mumbai last month, quoting English essayist Walter Bagehot.

")

If any member of the audience was perplexed about the governor’s literary turn of phrase, Das soon put his remarks in context.

“Deposit mobilization has been lagging credit growth for some time now. This may potentially expose the system to structural liquidity issues," Das said.“Households and consumers who traditionally leaned on banks for parking or investing their savings are increasingly turning to capital markets and other financial intermediaries. While bank deposits continue to remain dominant as a percentage of financial assets owned by households, their share has been declining with households increasingly allocating their savings to mutual funds, insurance funds and pension funds," he added.

Showing just how seriously the regulator is taking this issue, the governor reiterated the message at the RBI’s monetary policy meeting on 8 August.

“It is observed that alternative investment avenues are becoming more attractive to retail customers and banks are facing challenges on the funding front with bank deposits trailing loan growth. As a result, banks are taking greater recourse to short-term non-retail deposits and other instruments of liability to meet the incremental credit demand. This, as I emphasised elsewhere, may potentially expose the banking system to structural liquidity issues," Das said.

In other words, what is good for the stock market may not be favourable for the banking system.

The current exuberance in the capital market is diverting an important channel of funds away from lenders. This has ratcheted up banks’ credit-to-deposit (CD) ratios—a measure of how much money they are lending compared to what they have as deposits. A high CD ratio, therefore, would raise liquidity and credit risks for lenders.

While there is no specific regulatory threshold for the CD ratio, it is understood that the RBI is comfortable with a range of 70-80%. Which is why the first quarter numbers are a cause of concern—barring SBI, none of the top five Indian banks by market capitalization have a CD ratio below 80.

HDFC Bank, which is still reeling from the impact of the mega merger with parent HDFC last year, reported a CD ratio of 103.5. The management has reiterated its intention to bring down the number to pre-merger levels (84-87%) in a phased manner.

Axis Bank’s CD ratio came in at 92.2, followed by Kotak Mahindra Bank (87.2), ICICI Bank (85.8) and SBI (76.5).

Worryingly, all the lenders posted a quarter-on-quarter uptick in this key ratio, indicating that the sector’s credit-deposit mismatch woes are far from over.

Experts are fretting over banks having to sacrifice some credit growth in order to bring their CD ratios under control. “While Q1FY25 disappointed on the growth front, the (HDFC Bank) management remains confident of growth picking up in the coming quarters. The bank’s focus on deposit-led credit growth would imply a slowdown in credit growth momentum," analysts at Axis Securities said in a note.

Consistent deposit growth and NIM improvement remain key re-rating levers for the bank, they added.

That, of course, would be easier said than done.

Margin Pains

Deposits failing to keep pace with credit growth has another serious implication for banks—the hit on margins.

The ‘war for deposits’ is forcing lenders to hike their deposit rates to attract savers, which is putting pressure on their net interest margins (NIMs), which measures the amount of money that a bank is earning in interest on loans compared to the amount it is paying in interest on deposits.

This was amply borne out in the first quarter numbers.

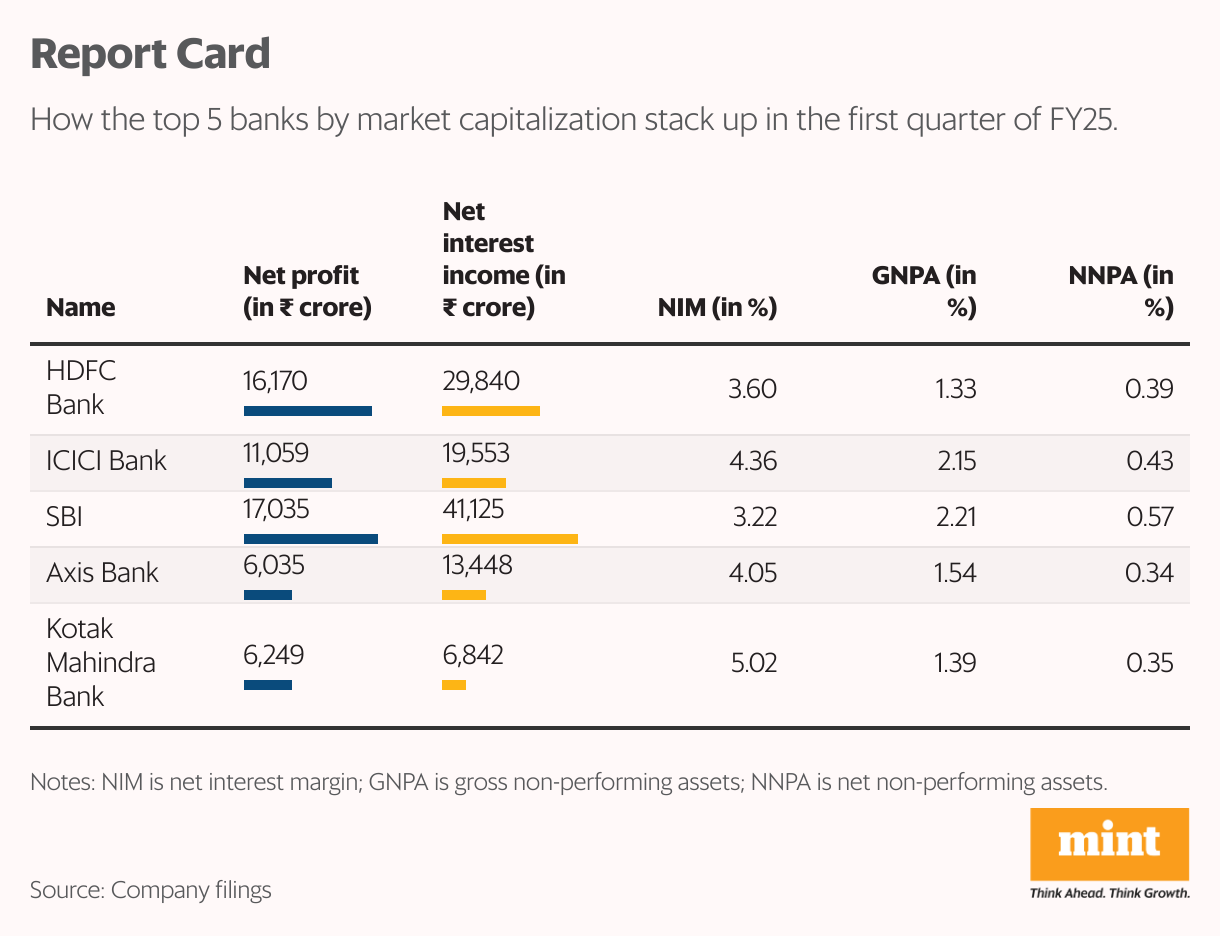

ICICI Bank saw a 4 basis points (bps) decline in NIM quarter-on-quarter to 4.36%, while that of SBI slipped 6 bps to 3.22%. Kotak Mahindra Bank’s margins declined by 26 bps sequentially.

Axis Bank reported sequential flat margins as it witnessed interest on income-tax reversals during the quarter, which when clubbed with healthy investment income, propped up the NIMs.

For HDFC Bank, analysts say NIMs are likely to face some pressure in the near term owing to the increase in the cost of funds, reflecting the rate hike in retail deposits and some possible pressure due to the draft guidelines on LCR.

However, this remains a sector-wide issue, at least in the near term.

“Given the rising competitive intensity for low-cost and granular deposits facing the banking system, loan-deposit ratios at historical highs, and expected rate cuts towards the back-end of FY25, we believe banks are faced with the challenge of quality deposit mobilization, elevated funding costs (lagged deposit repricing) and softer incremental spreads," HDFC Securities said in a report last month.

As banks and NBFCs navigate the growth-margin trade-off, HDFC Securities believes the combination of lower growth and lower spreads is likely to keep valuations under check, especially of mid-sized, high-growth franchises.

“Given the historically high loan-to-deposit ratio (across the banking system) and the RBI’s frequent flagging of growth in unsecured consumer credit, we envisage deceleration in system-wide loan growth trends from current levels," it said, adding that NIMs are likely to drift incrementally lower during FY25.

Asset Quality

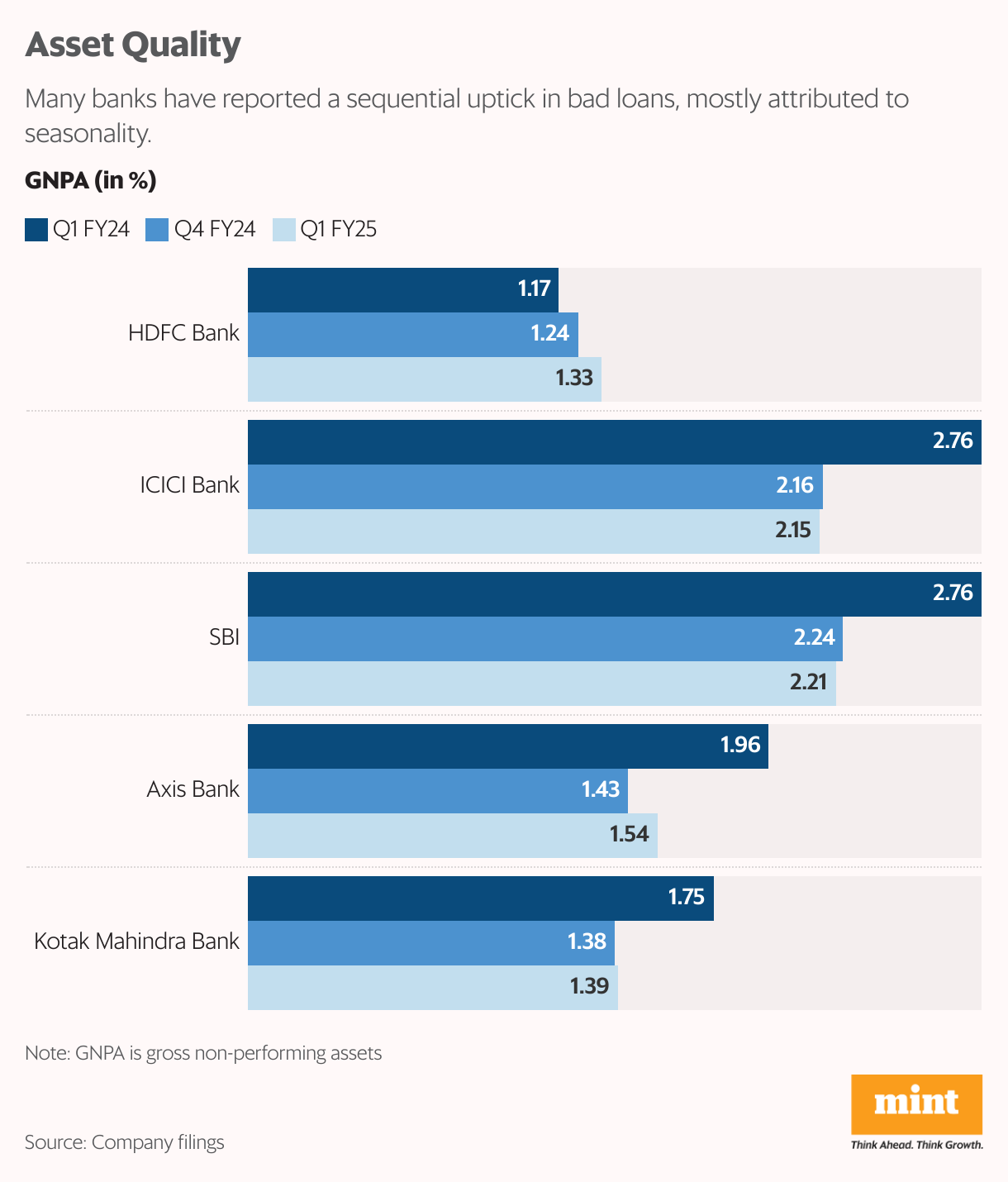

The reduction in the banking sector’s mountain pile of bad loans has been among the top success stories of the Indian economy in the last decade.

As per the RBI’s latest Financial Stability Report, the gross non-performing assets (GNPA) ratio of banks fell to a 12-year low of 2.8% at the end-March 2024. Their net NPA ratio too fell to a record low of 0.6%.

Do the Q1 results maintain this improving trend?

HDFC Bank saw a sequential rise of 9 bps in its gross NPA ratio, while that of SBI remained flat. ICICI Bank too reported flat NPAs, though there were lower recoveries from corporate and SME book and higher gross slippages from the retail book amid an uptick in credit costs.

Axis Bank, which had posted a sequential decline in absolute GNPAs for the past 11 quarters, reported a 7.2% sequential rise whereas net NPAs rose by 10.3%. The management attributed this to collection delay, which is normalizing in Q2.

Most analysts maintain that the uptick in banking sector’s NPA levels in Q1 was seasonal in nature (the heatwave-triggered agri slippages) as well as due to the impact of general elections.

However, with many lenders reporting some incipient stress in their retail and agri loan books, investors would do well to keep track on this crucial metric in the subsequent quarters.

Crucially, RBI governor Das too sounded a note of caution during the policy meet on 8 August.

“Excess leverage through retail loans, mostly for consumption purposes, needs careful monitoring from a macro-prudential point of view. It calls for careful assessment and calibration of underwriting standards, as may be required, as well as post-sanction monitoring of such loans," he said.

Price is Right?

How should investors approach this sector at this juncture? The biggest positive is that banks have been reporting robust credit offtake for the past few quarters, which is a sign of healthy macros as well as revival in private capex. However, the lagging deposit growth risks curtailing this momentum going forward.

Banks’ reliance on other sources like short-term borrowings, certificates of deposit etc to fill the funding gap also exposes them to interest rate volatility, further weighing on their risk profile. Even for the top performers, the Street is hunting for fresh triggers.

“With the cost-to-income ratio at ~39%, we believe ... (ICICI Bank) is nearly fully optimized, which could be difficult to sustain. While ICICI Bank has emerged as a sector leader in recent quarters, we believe that the barriers to outperformance are getting steeper," HDFC Securities noted.

From investors’ perspective, the prolonged underperformance of Bank Nifty is perhaps the clearest indicator of which way the wind is blowing for the sector. However, some experts feel this itself presents an opportunity.

“Clearly, there is underperformance by the banking sector in general owing to some of the near-term issues such as NIMs pressure, elevated CD ratio, higher slippages in select pockets and increased regulatory scrutiny. In our view, even after baking in some of these negatives with normalized credit cost/growth, valuation for the banking sector is looking attractive. This is especially true in private sector banks," Quantum’s Mathai added.