Mint Primer | What is NPCI’s game plan for the BHIM app?

- Reports suggest that BHIM is looking to foray into e-commerce and integrate with the ONDC. This will enable customers using the BHIM app to access different services provided by ONDC—a government scheme to promote an open e-commerce network.

Last week, the National Payments Council of India (NPCI) announced it was hiving off Bharat Interface for Money (BHIM), a payment app based on UPI, into a separate subsidiary. What is the rationale behind this move? Mint explains:

What was the idea behind BHIM?

BHIM, the payment application developed by NPCI, was among the first wave of apps launched (in December 2016) to facilitate digital payments using the Unified Payments Interface (UPI). BHIM allows users to send or receive money from a UPI payment addressee, or send money to non-UPI based accounts by scanning a QR code. For BHIM, the maximum transaction limit is ₹1 lakh per day for a single bank account linked to the app. Like other UPI apps, one can link BHIM to multiple bank accounts and seamlessly switch between different accounts when making transactions or checking balances.

Read more: Dressing Pine Labs for IPO: What ‘fintech bully’ Amrish Rau can learn from Paytm

How has BHIM fared so far?

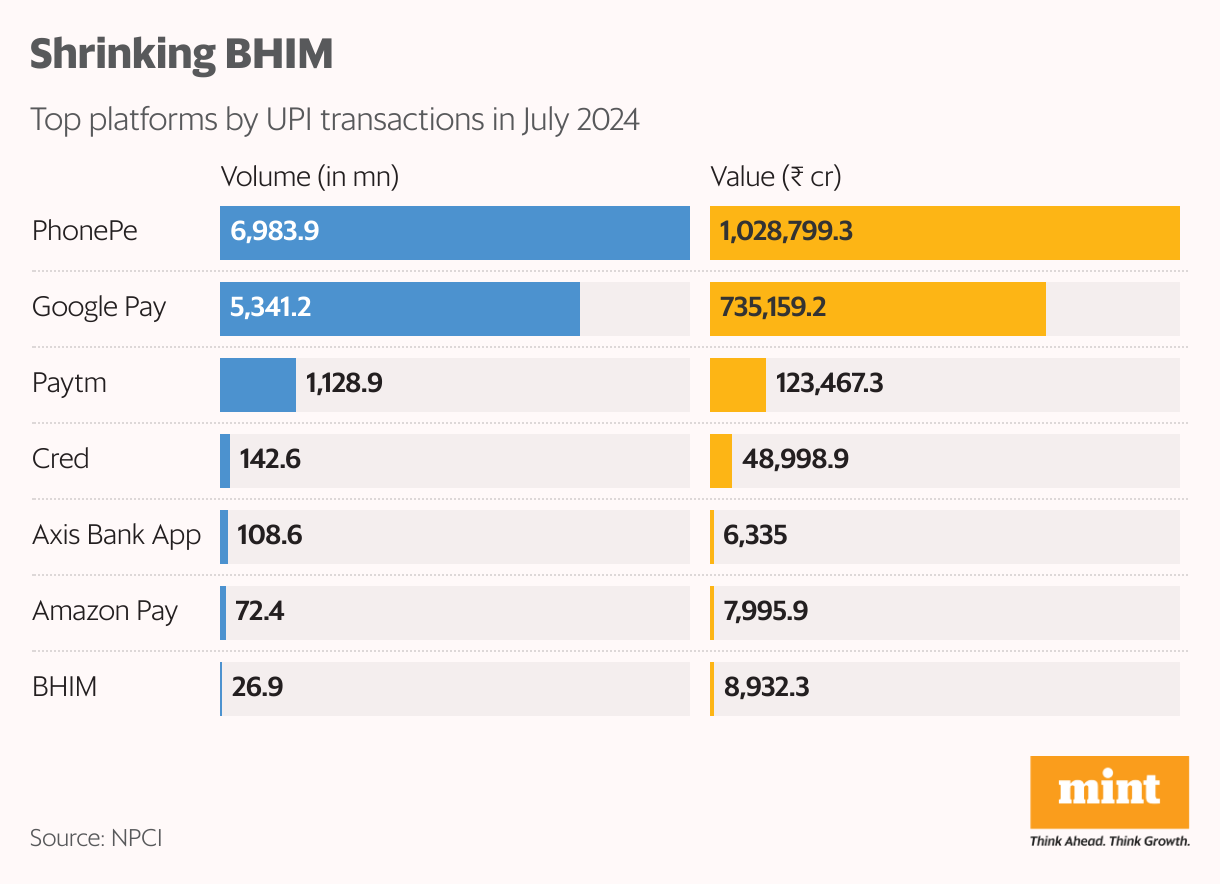

The BHIM app’s market share has dipped in the past few years. In July 2024, BHIM processed 27 million transactions worth ₹8,932 crore while Walmart-owned PhonePe processed as many as 6,983.9 million transactions worth ₹10.28 trillion and Google Pay saw 5,341 million transactions worth ₹7.35 trillion. The reason why third-party UPI apps are popular compared with the BHIM app is not difficult to see: private apps provide promotional offers like rewards and cash backs. On the other hand, there is a limit to what NPCI, which is incorporated as a ‘not for profit’ company, can offer consumers.

Why is NPCI looking to hive off BHIM as a subsidiary?

The move could boost BHIM’s market share vis-à-vis Google Pay and PhonePe, which dominate the payment landscape with a market share of 85%. The BHIM app had limited marketing budgets and lacked in consumer awareness. With the creation of a new subsidiary, BHIM will have a dedicated team to focus on its development.

Read more: RBI’s digital rupee needn’t languish: Here’s how it can succeed

What challenges does BHIM face?

The biggest will be to improve its market share in the retail segment, already dominated by apps like Google Pay and PhonePe. Building a brand image across different strata of society will be among its initial challenges. Separately, BHIM will also have to compete with other bank apps. The subsidiary can potentially fix some of these issues. Lack of customer awareness is a major drawback; limited marketing budgets is another. The new entity will have greater flexibility to invest both in awareness campaigns and tech.

How can BHIM develop its user base?

Reports suggest that BHIM is looking to foray into e-commerce and integrate with the Open Network for Digital Commerce (ONDC). This will enable customers using the BHIM app to access different services provided by ONDC—a government scheme to promote an open e-commerce network. Rahul Handa, former ONDC vice president for strategic initiatives, will be the BHIM subsidiary’s chief business officer. He will drive this initiative that will target tier-II and tier-III markets, which remain untapped by banks.

Read more: Project Nexus: A UPI-like network for international payments

- The BHIM app’s market share has dipped in the past few years. In July 2024, BHIM processed 27 million transactions worth ₹8,932 crore.

- The reason why third-party UPI apps are popular compared with the BHIM app is not difficult to see: private apps provide promotional offers like rewards and cash backs.

- The move could boost BHIM’s market share vis-a-vis Google Pay and PhonePe, which dominate the payment landscape with a market share of 85%.

- With the creation of a new subsidiary, BHIM will have a dedicated team to focus on its development.

- Building a brand image across different strata of society will be among BHIM's initial challenges.