Why small finance banks want to glide faster into universal banking

")

- Small finance banks face challenges in raising low-cost deposits and diversifying their loan portfolio.

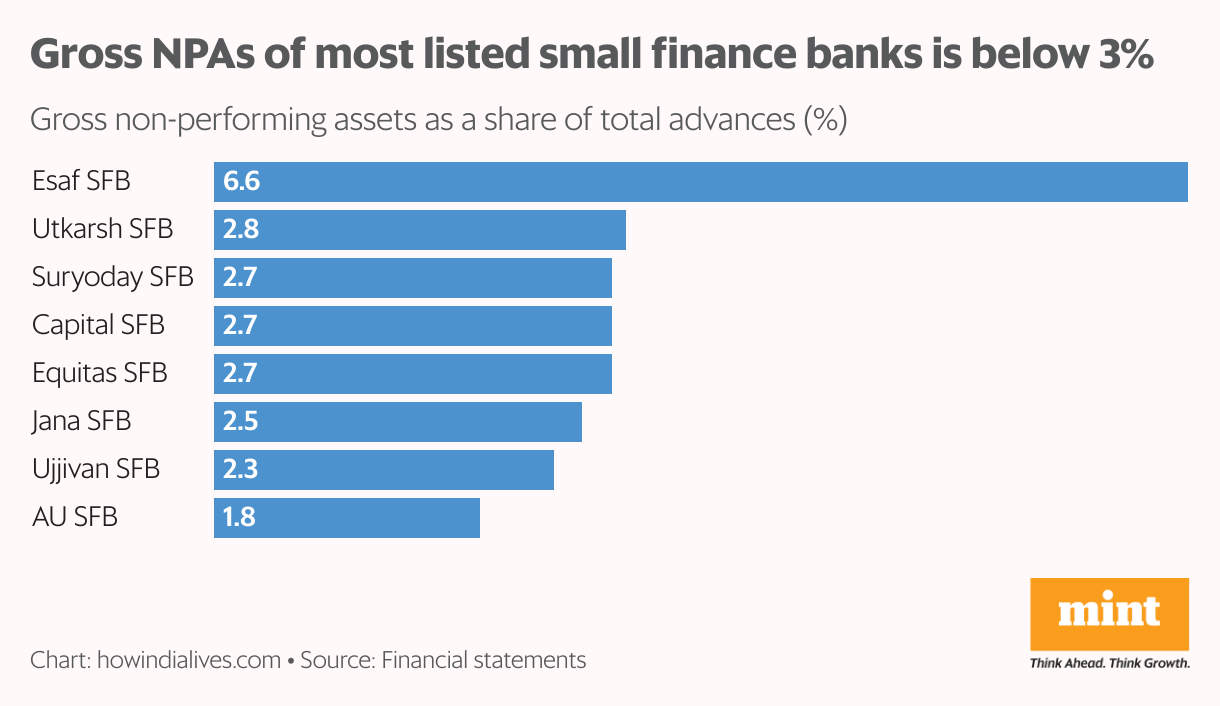

Earlier this month, AU Small Finance Bank, the country's largest small finance bank (SFB) by market capitalization and advances, said it had applied for a universal banking licence. If it gets one, AU would become the first SFB to transition into a full-fledged bank. Its smaller rival, Capital SFB, is also eyeing this shift within 12-18 months. The Reserve Bank of India's updated criteria, released in April, require a net worth of ₹1,000 crore, gross non-performing assets (NPAs) below 3%, net NPAs under 1% for two consecutive years, and a public listing, among other conditions. As of March 2024, AU was the only SFB meeting all these benchmarks.

However, many of them hope to turn into a full-fledged bank.

“Universal banks have relatively lower capitalization and priority sector lending requirements, along with higher borrower and group exposure limits," credit rating agency Icra Ltd pointed out in an April 2024 report, adding that it could also "lower risk perception and thereby facilitate the improvement and diversification of their deposit franchise."

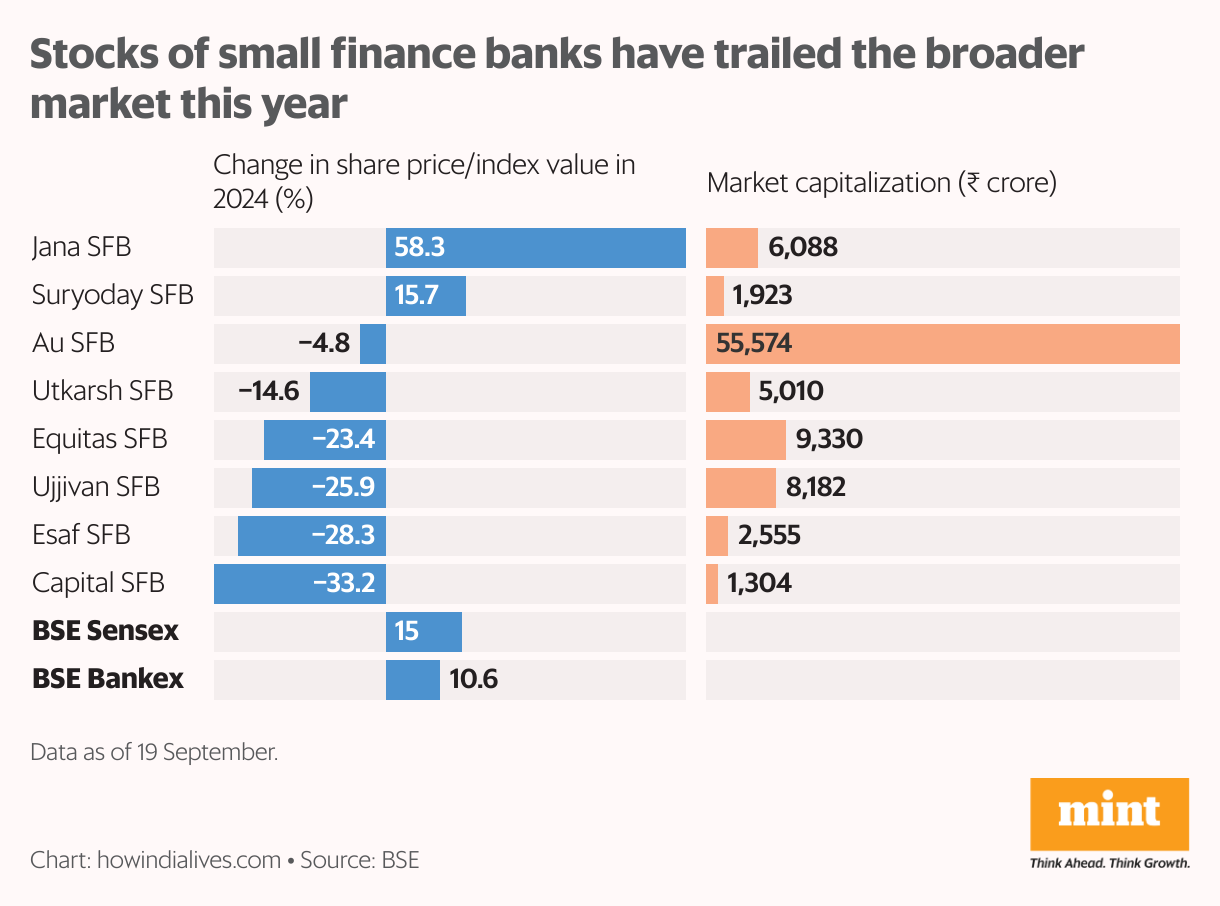

SFBs, as a group, have not impressed stock markets this year. Of the 11 SFBs, eight are listed, and six have underperformed the broader BSE Sensex and the BSE Bankex, which tracks the banking sector.

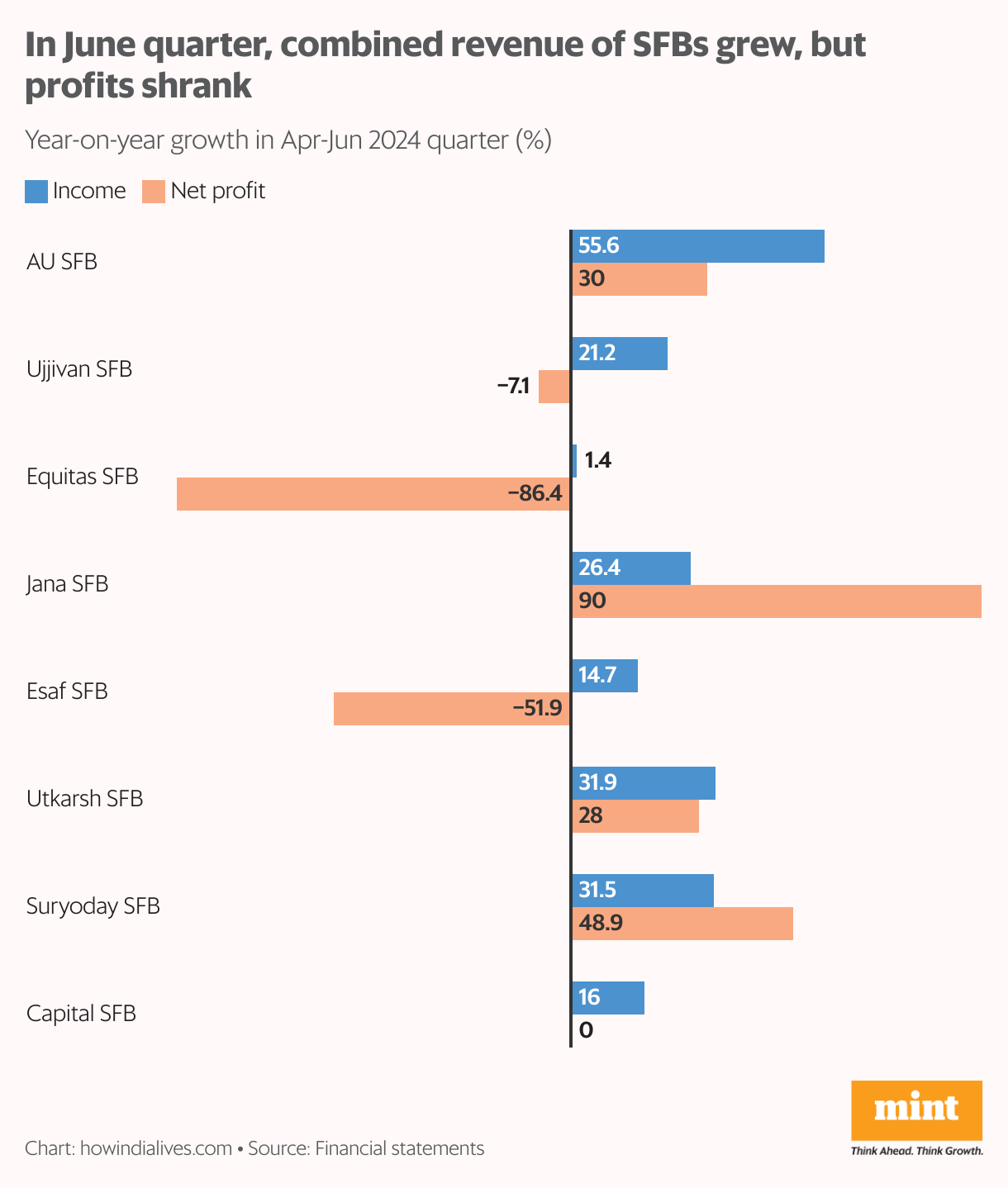

One reason for this underperformance is pressure on profits. In the June-ended quarter, while the total income of these eight SFBs increased 29%, their profits dropped. This was led by Equitas SFB, which set aside ₹180 crore to strengthen its provisioning coverage ratio, done typically as a buffer against bad loans.

CASA chase

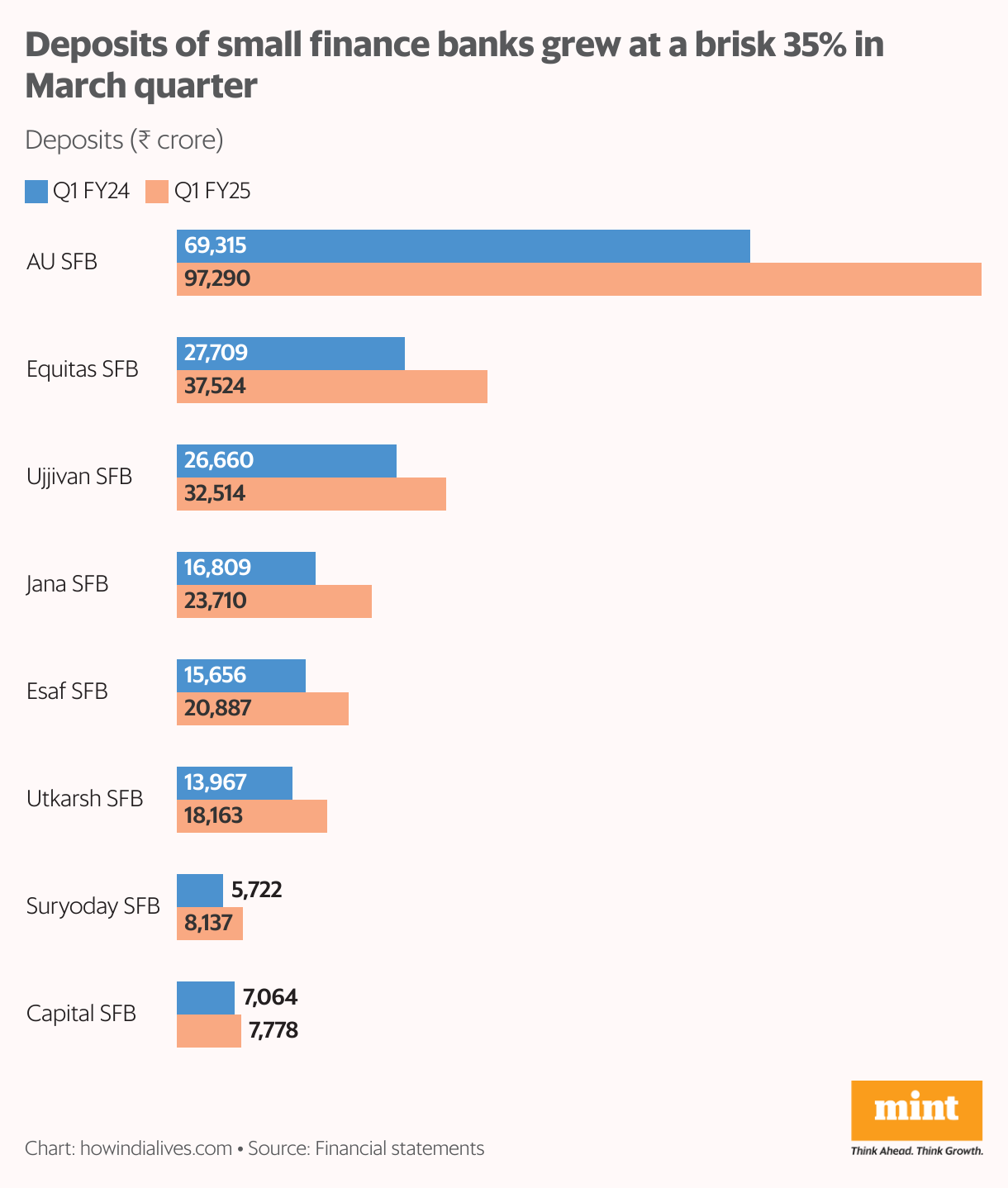

Despite concerns the ‘small finance’ tag might increase risk perception among depositors, SFBs have consistently grown their deposit base. In the June quarter, total deposits of the eight listed SFBs grew 35% year-on-year. A January 2024 report by CareEdge highlighted that while the credit-deposit ratio of SFBs remains higher than that of the broader banking sector—indicating more loans relative to deposits—this ratio has consistently declined in recent years, even as deposits continued to grow.

However, the report also raised concerns about SFBs' ability to attract low-cost deposits, particularly current account and savings account (CASA) deposits. In recent months, all banks have faced challenges on the deposit front and have been urged by both the government and the RBI to mobilize more deposits. In response, SFBs have raised deposit rates this month, which could pressure margins if lending rates don't increase proportionally.

Beyond microfinance

Gross NPAs of SFBs rose to 5.34% in 2021 and 7.32% in 2022, during the pandemic. This has improved since. Seven of the eight listed SFBs had gross NPAs of below 3%, as of June 2024. However, SFBs face limitations in lending, both internally and through regulations. A majority of SFBs were earlier microfinance institutions, a sector where they remain strong operationally.

However, the diversification challenge remains. Since SFBs were formed primarily to improve financial inclusion, they face higher priority sector lending (PSL) requirements and restrictions on loan ticket size.

“Removing the 50% exposure requirement up to ₹25 lakh ticket size and lowering the PSL requirement will facilitate product diversification," Icra said. The share of microfinance for SFBs has dropped from 40% of advances in 2019-20 to 32% in 2022-23. The share of secured loans such as home loans has increased. Universal banking licenses will help them diversify more.

Cost factor

SFBs face unique cost challenges, largely due to their microfinance origins. Many started with a large employee base but lack the infrastructure that traditional banks have built over time. For instance, as of July 2024, all SFBs collectively operated about 3,200 ATMs, a small fraction compared to the 216,000 ATMs across India. While SFBs have issued 34 million debit cards that can be used at any ATM, owning ATMs contributes to brand visibility, which is crucial for attracting CASA deposits.

Also read | Growth in bank deposits has been slow because RBI wants it to be slow

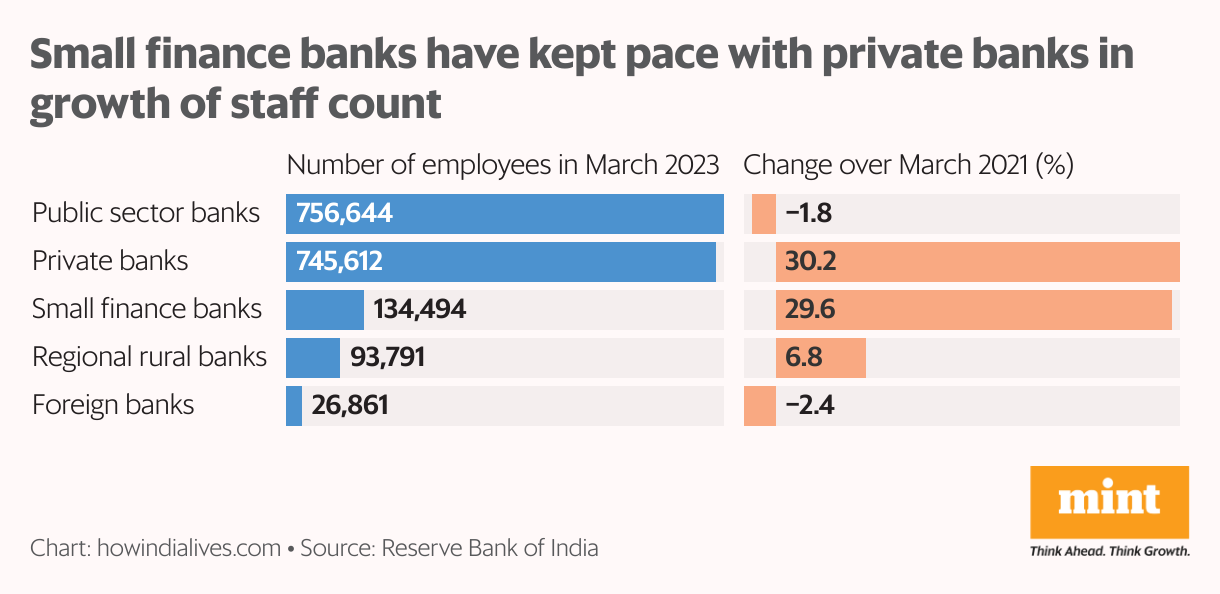

Diversifying their loan portfolio and scaling it up while keeping NPAs low require investments in both technology and people. As of March 2023, SFBs had a staff strength of 135,000. Its 30% increase in staff strength in two years matched private sector banks, underscoring the challenge in acquiring talent. Full-fledged banks have greater strategic freedom in playing this game. That's a reason why some SFBs want to glide faster into universal banking.

www.howindialives.com is a database and search engine for public data