Quick commerce is on steroids. So, why is Dalal Street not cheering Zomato, Swiggy?

- Quick commerce is on steroids. The two listed companies, Zomato and Swiggy, have doubled their revenue from this segment in the last one year. And yet, Dalal Street isn’t that enthused—the firms are laggards when compared to the benchmark Nifty 50. What gives?

New Delhi: Summer of 1997.

The dotcom boom was in full swing on Wall Street. Venture capital firms, investment banks and retail investors were in a mad scramble to get their hands on anything with a ‘.com’ attached to its name. Every company seemed to be a trailblazing hero which was about to dislodge the outdated, crusty incumbents and rewrite history. Every founder was a Napoleon, Guevara and Rockefeller rolled into one.

On 15 May that year, a small, Seattle-based startup made its market debut. Founded by a nerdy Wall Street executive with a disarmingly hearty laughter, the three-year-old company had never made a dollar in profit. Its topline growth was impressive, but equally impressive was its growing list of competitors, including giants of corporate America which were mounting a fervent challenge to protect their kingdom. Whatever might be the startup’s financial and operational predicament, its vision was audaciously ambitious—to become the “Earth’s Biggest Bookstore".

The online bookseller was named Amazon.com. The founder was a gentleman called Jeffrey Preston Bezos.

Amazon.com had a stellar start to its market innings, soaring 30% over its IPO price on the very first day, followed by a continuous uptrend in tandem with the broader market. But it soon ran into the corporate equivalent of a Category 5 hurricane.

The dotcom mania imploded in spectacular fashion in 2000, striking the fear of God into both Wall Street and Main Street. The Nasdaq index plunged about 80% during the bubble burst period. Many hyped internet sensations vanished in a puff of smoke, including Amazon-backed Pets.com, which shut shop barely nine months after completing its IPO. Amazon’s stock itself shed a spine-chilling 90% of its value, between 2000 and the end of 2001.

Analysts began raising doubts over Amazon’s ability to survive. Its lack of profitability was like a huge bull’s eye painted on the back of the company. Bezos, however, remained undeterred. Over the next few years, Amazon got into almost every e-commerce category, from music, video games and electronics to toys, home decor and even enterprise software services. The e-tailer grew its revenue handsomely, but thanks to its cash-guzzling expansion, profits remained minuscule. It never paid dividends to shareholders. And what was the impact on the stock? Amazon’s shares, which hit a high in December 1999, took almost a decade to reclaim that level.

A fast-growing company. In a fast-growing sector. Led by a charismatic founder-leader. Staffed by the best minds in the business. And yet, the path for shareholders was anything but smooth.

Amazon, of course, later turned out to be among the defining success stories of the stock market, but it is so easy to forget what that road looked like and how long the journey took.

It is said the markets are always in giving mode—either in the form of returns or lessons. For millions of investors in India’s fast-scaling quick commerce sector, has the lesson-learning phase suddenly gotten underway?

Bigger, higher, quicker

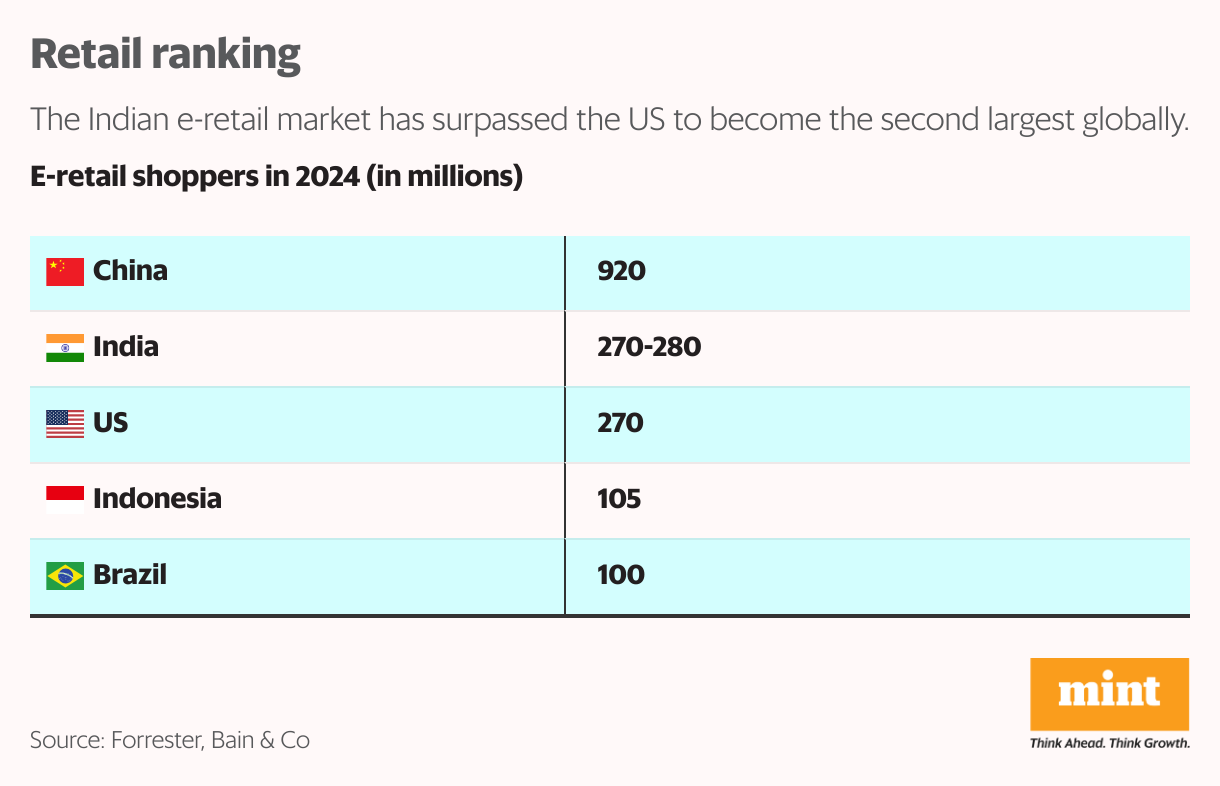

Perhaps the most lasting impact of the covid-19 pandemic was the rapid digitization of India, especially with respect to consumer behaviour. With over 270 million online shoppers, the Indian e-retail market has now surpassed the US to become the second largest globally, according to a recent report by management consultancy Bain & Co.

The domestic e-retail market has reached a size of approximately $60 billion in gross merchandise value (GMV). A key metric in e-commerce, GMV tracks the total value of all the goods sold on a platform, not including discounts and other expenses.

One of the primary drivers of the e-retail sector is quick commerce, where orders are delivered in less than 30 minutes.

“The dramatic rise of quick commerce has been one of the most defining hallmarks of India’s e-retail market over the last two years. In 2024, more than two-thirds of all e-grocery orders and one-tenth of e-retail spend happened on q-commerce platforms," the report stated.

Bain expects the quick commerce market to grow by over 40% annually until 2030, fuelled by expansion across categories, geographies, and customer segments.

All good news, right? But why is the cheer not spreading to Dalal Street?

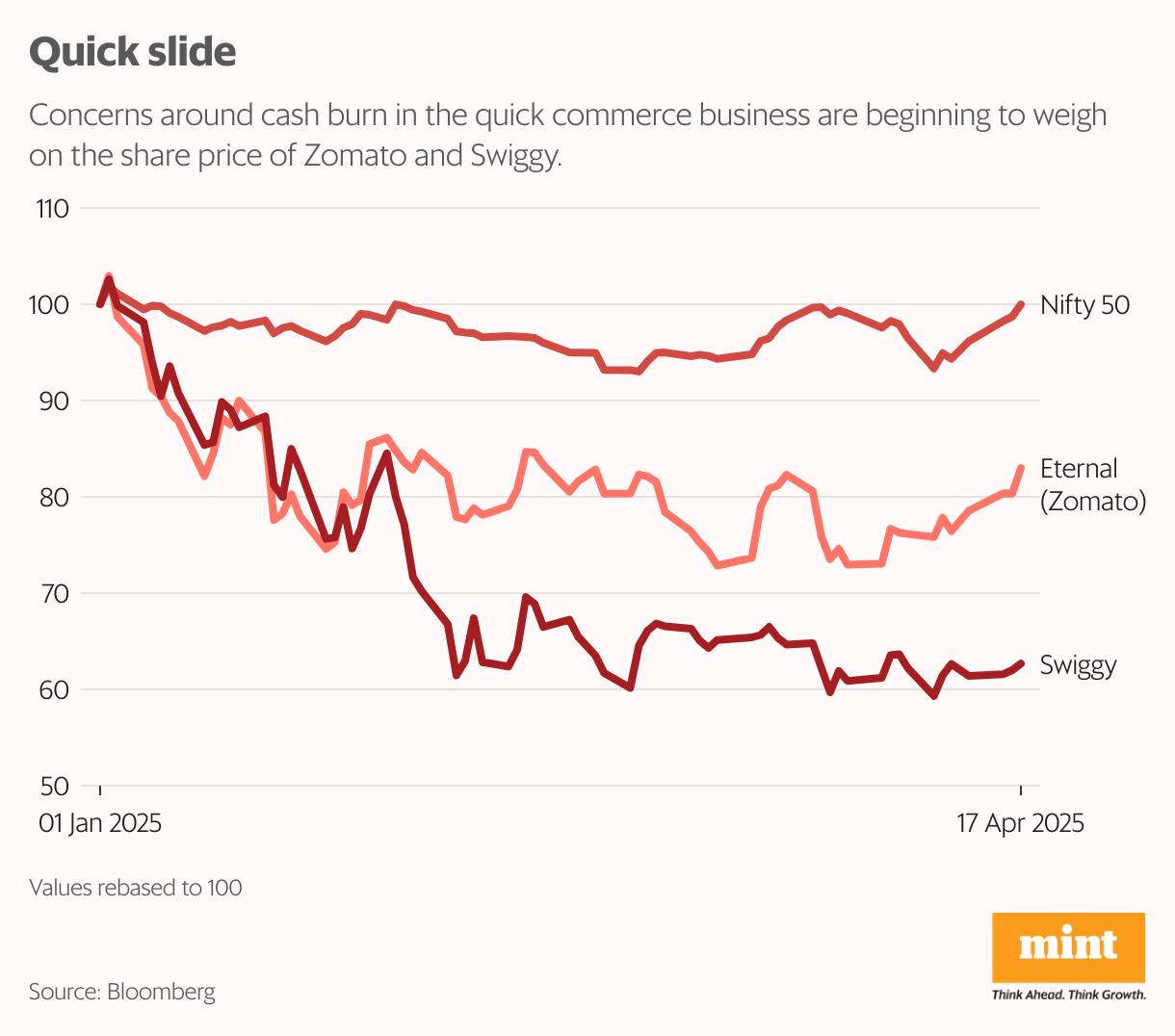

With an over 20% fall this year so far, Zomato (now rebranded as Eternal) is among the top laggards of the benchmark Nifty 50. Its peer, Swiggy, which listed in November last year, has fared even worse, shedding almost 40% this year to date, and down 15% from its IPO price.

The furious pace of expansion in the quick commerce space, as well as the rapid inroads being made by some deep-pocketed newcomers, is starting to make analysts nervous about the capital-intensive nature of this competition. And the time it will take before we can crown ‘the last men standing’ in the sector.

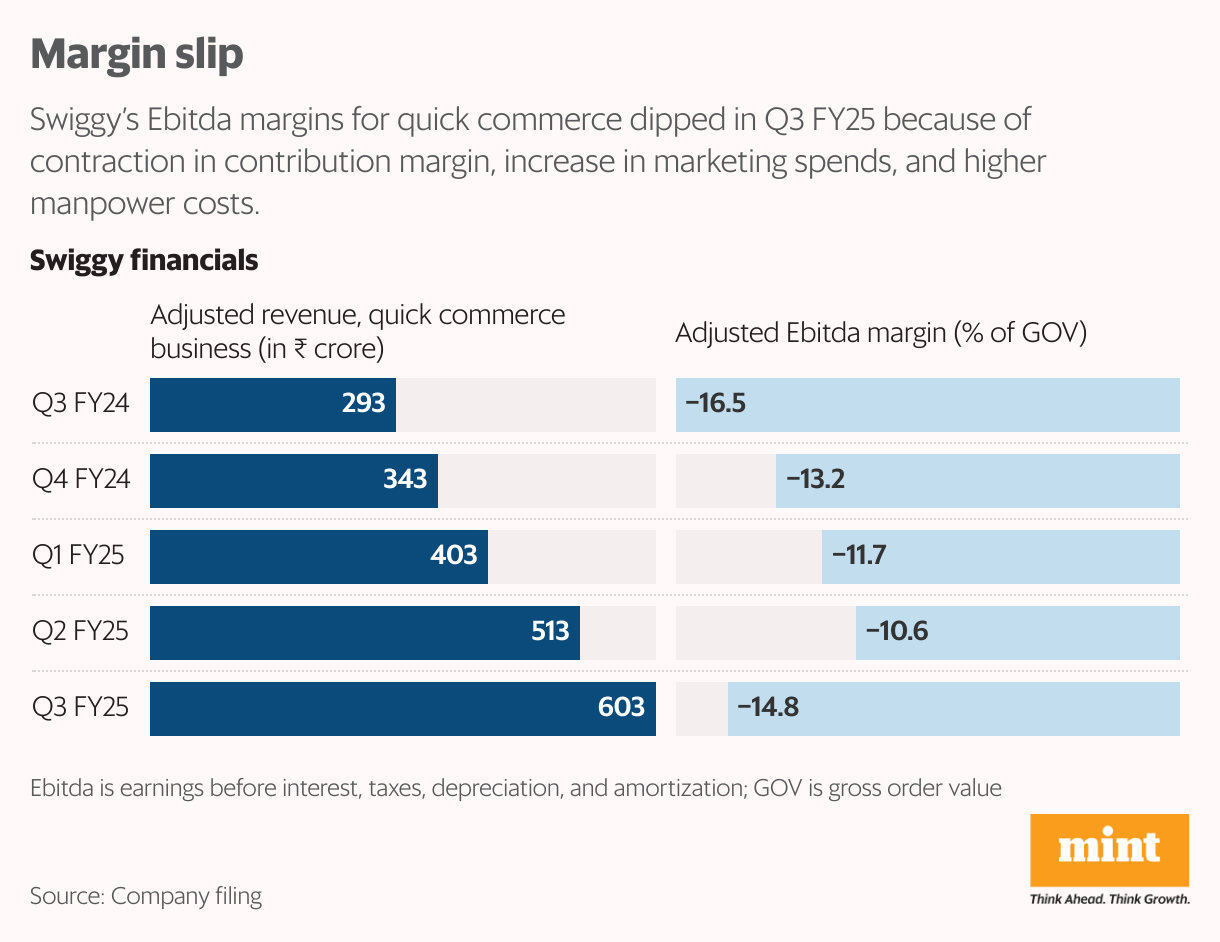

Zomato operates in the quick commerce segment through Blinkit, which it acquired in 2022, while Swiggy runs Instamart. Swiggy is the third-largest player in the quick commerce market with Blinkit and Zepto occupying the top-two positions, Jefferies stated in a note dated 11 March.

“Quick commerce has been the talk of the town for the last few years. This sector has gone from being a fan favourite to scrutiny by veteran investors on the back of rising competitive intensity, high burn rates, never-ending funding rounds, elusive profitability and thin margins. And all of these factors are now putting pressure on valuations," Pranay Aggarwal, director and CEO of Stoxkart, an online investment platform, told Mint.

Interestingly, quick commerce was supposed to be the ‘alpha’ for Zomato and Swiggy, with brokerages assigning higher multiples for this vertical compared to their traditional business of food deliveries.

“The quick-commerce story narrative has quickly moved from “higher growth, improving unit economics" to “rising losses, high competition market". This is at a time when the risk appetite is reducing and global internet multiples have de-rated," analysts at global brokerage BofA Securities said in a note.

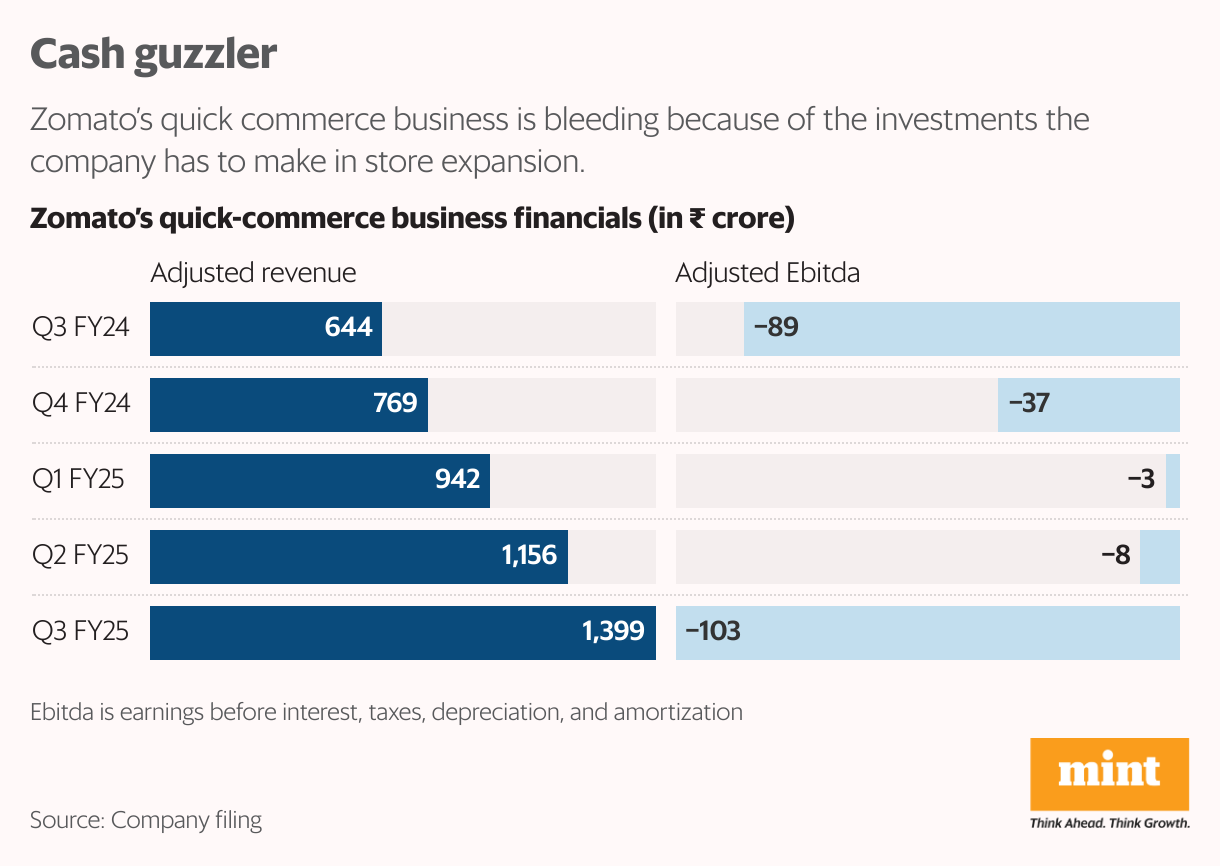

While the market opportunity in the quick commerce segment is certainly formidable, expansion is a massively cash-guzzling exercise, requiring heavy investments in dark stores (retail facilities used to fulfill online orders), IT infrastructure and operational expenses like worker salaries.

Zomato, which has over 1,000 dark stores, plans to double the number by December 2025. Swiggy Instamart had earlier said it will increase its dark store count from 600 to 1,046 by March 2025. Zepto too is targeting the 1,000-mark, from around 800 currently.

The rising competitive intensity is compounding the problem for the listed incumbents, with players like Flipkart, Myntra, BigBasket, Amazon, and of course Zepto snapping at their heels.

All these players are backed by strong balance sheets—in case the competition descends into an all-out price war, as many analysts fear, the damage for both the winners and losers will be substantial.

“As new platforms launch their services and as incumbent platforms enter in each other’s turf, they are likely to offer higher discounts initially. Incumbents are unlikely to let go of their high-end users and are likely to respond," BofA Securities noted.

High competition is likely to lead to higher marketing spending, an increase in platform-led discounts, consumer delivery charges going down, higher rental expenses for dark stores and higher wages, it added.

It is also not as if expansion is a sure-shot gamble. Many new-age companies have already burnt their fingers with forays into tier-II and III towns. In fact, early in 2023, Zomato said it had ceased food deliveries in 225 smaller cities as the performance of these markets was “not very encouraging".

Quick commerce players are now expecting the next wave of growth from tier-II and III towns, but price sensitivity and consumer behaviour in these markets can be markedly different from that in metros. Traditional kirana shops are more cohesively woven into the social fabric of smaller towns and villages. These family-run outlets often know their customers on a first-name basis, offer free home deliveries and even extend credit to their clientele.

Can an app compete with this level of hyper-personalized service?

That apart, fewer working professionals per household compared to metros and high demand for sachet products (which is detrimental to quick commerce firms’ margins and average order values) will make these markets an extremely tricky pitch for companies.

Food for thought

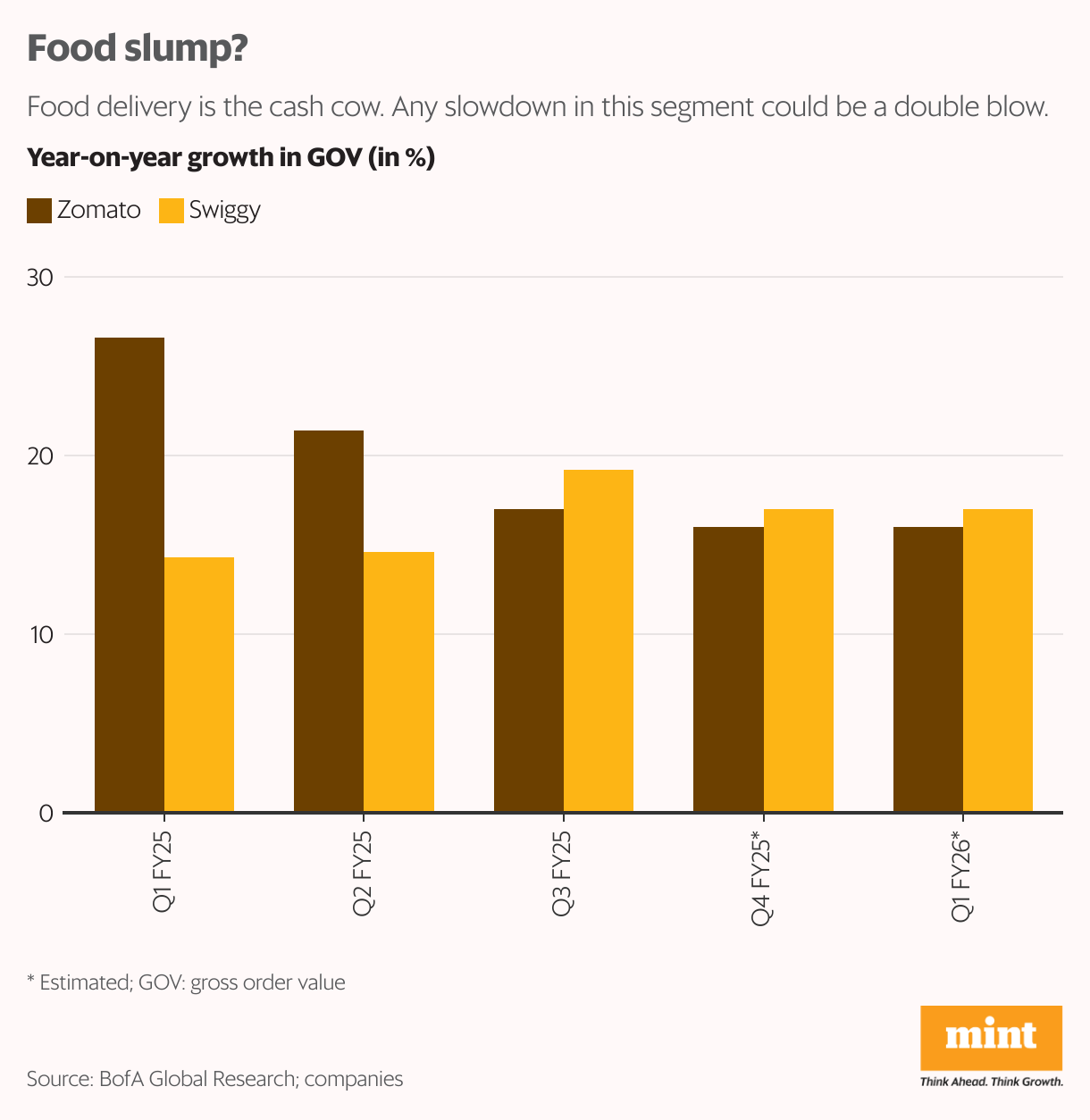

Troubles have a peculiar mathematical propensity of arriving in a bunch. As if the wall of worries around quick commerce was not enough, Zomato and Swiggy are also witnessing lacklustre growth in their food delivery business.

For Q3FY25, Swiggy saw 19% year-on-year (y-o-y) growth in the gross order value (GOV) of food delivery, while that of Zomato slumped to 17% compared to 26% in Q1. In its post-earnings statement, Zomato said its 20%+ y-o-y GOV growth guidance for the food delivery business is more long-term. “There will be periods of higher and lower growth along the way. Currently, we are going through a broad-based slowdown in demand which started during the second half of November," it said.

The company, however, exuded confidence about a recovery soon, saying it remains confident of the long-term outlook of more than 20% yearly GOV growth in the business given the strong fundamentals.

Others are not so sure about the segment as a whole.

“We expect the food delivery GOV growth in the next few quarters to slow to 16-18% y-o-y vs. market expectations of around 20% growth. While this is not a material slowdown, we note that slower-than-expected growth would lead to consensus downgrades for both Zomato and Swiggy," BofA Securities said.

The urban consumption slowdown is visible across the entire e-commerce sector. As per Bain estimates, e-retail growth has slowed to 10-12% in 2024, compared to the historical trend of 20%, weighed by the twin effects of inflation and stagnating wage growth. That said, the recent tax cuts delivered by the union budget may come to the rescue of e-commerce firms.

“Our analysis of long-term historical data suggests that there was a noticeable increase in consumption in FY06, FY11, FY13 and FY14—the last four occasions when there were meaningful tax cuts. Therefore, we believe that the income tax cuts announced in the union budget for FY26, are likely to trigger strong consumption growth among middle class consumers, who are a key demographic for the hyperlocal e-commerce players," ICICI Securities stated in a report.

“Given the discretionary and celebratory nature of food delivery, we think the sector could be the key beneficiary as consumers start seeing higher disposable incomes from May 2025," it added.

Zomato and Swiggy declined to comment on this story.

Investor corner

More hyped a sector, the more difficult it is for public investors to make money— that’s a rule of thumb many veteran market experts swear by.

The only way to profit from a hype train is to board it early. The latecomers might find the narrative changing faster than their reflexes.

BofA Securities recently downgraded Zomato to ‘neutral’ and Swiggy to ‘underperform’, led by its expectations of rising losses in the quick commerce business for the next 12-15 months and slowing growth/slower pace of margin improvement in food delivery. While this seems to be the consensus view, there are some dissenting voices as well. For instance, ICICI Securities thinks the markets are overreacting to concerns around quick commerce cash burn as well as arrival of new entrants like Zepto, which was founded in July 2021 and is reportedly eyeing an IPO later this year.

")

“Our on-the-ground checks (across 4 locations in each of the top 8 metros) reveal that while some discounting still persists in the space, item level discounting is past the peak levels seen from Nov’24-Jan’25. At this time, players are more focussed on incentivizing higher order values through some cart level discounts," it said.

Additionally, there has been a noticeable pull back in performance marketing spending from the quick commerce platforms, which should yield some improvement in contribution to Ebitda (earnings before interest, taxes, depreciation, and amortization) conversion. “Therefore, despite lack of visibility on contribution margin improvement in the near term, we think the valuation for quick commerce businesses is compelling for investors with an investment horizon of >1 year," it added.

It is interesting to note that even among the sector’s backers, expectations for quick gains are muted. Analysts say the conversation veering towards fundamentals rather than just ‘vibes’ is a welcome shift.

“The quick commerce sector has reasonable growth tailwinds from potential higher order value and increasing share of internet savvy user base in the medium term. But market share focus of key players could keep the competitive intensity elevated in the near term," George Thomas, fund manager—equity, Quantum AMC, told Mint. “While the sector has a long growth runway and scope for optimizing operating metrics, current valuations are difficult to justify as most of the cash flow generation is back-ended," he added.

Given the nascent stage of the industry, players have scope to improve the operating metrics by rationalizing assortment and optimizing their supply chain.

“Quick commerce is not going away, but the hype cycle is maturing into a grind cycle. For investors, that means shifting from growth-at-all-costs optimism to fundamentals-first discipline. This is a sector where timing your entry and managing expectations will be more important than chasing momentum," Stoxkart’s Aggarwal pointed out. “At the current juncture, investors should avoid FOMO in IPOs," he added.

One would do well to remember that not every startup will turn out to be Amazon. And even if some company manages to replicate Bezos’ astronomical success, it will take more time than what impatient investors assume.