Markets

Markets

Affluent India is fuelling the equities surge. But that story has gaps

")

Summary

- Every bull market needs a story. One of the main stories currently being sold is the premiumization of the Indian economy or that consumers are buying more expensive products than in the past. Is that the case?

Mumbai: It’s winter in Mumbai. And it’s that time of the year when stock brokerages, investment banks and other financial firms organize their India conferences. Presentations are made to talk up Indian stocks. And between presentations, people attending like to stand around having their cups of coffee, and ask each other that favourite question—KLH—or kya lagta hai (what do you think?).

Every bull market needs a story. One of the main stories currently being sold is the premiumization of the Indian economy or that Indian consumers are buying more expensive products than in the past and how that will continue to benefit listed companies. Also, the number of such consumers is expected to go up. Let’s look at a few such data points.

Affluence rising

Domestic passenger vehicle sales (or simply put cars) from April 2023 to January 2024 stood at 3.42 million. If they continue selling at the same pace, firms will end up selling more than 4.1 million passenger vehicles by the end of this financial year, the highest ever. A January 2024 news report in the Business Standard points out that the average selling price of a passenger vehicle in India has gone up over 50%, from ₹7.65 lakh in 2018-19 to ₹11.5 lakh in 2023-24. Premiumization, with more customers buying sports utility vehicles (SUVs), is one reason for the same.

Second, from April to November 2023, the total number of passengers taking domestic flights stood at 101 million. If things continue at this pace, the number of domestic passengers in 2023-24 should cross 150 million, higher than the 2019-20 peak of 141.6 million.

A third data point is the number of demat accounts—they have jumped from 39.4 million in December 2019 to 143.9 million in January. Further, the investments in mutual funds through the systematic investment plan (SIP) route in January stood at ₹18,838 crore, crossing ₹18,000 crore for the first time.

Fourth, the number of Unified Payments Interface (UPI) transactions stood at 12.2 billion in January 2024. Fifth, in December 2023, the number of credit cards stood at 97.9 million.

Yet another data point to buttress the premiumization story comes from the Goldman Sachs report titled ‘The rise of Affluent India’. Published in January, it pointed out that the number of postpaid mobile phone connections as of March 2023 stood at 92 million, up from 79 million in March 2022.

Then, a recent report in the Business Standard pointed out that the sale of luxury homes with prices ₹4 crore or above, jumped by 75% in 2023 to 12,953 homes.

Stock prices, meanwhile, have been rising at a very rapid pace, in particular prices of public sector companies, on account of the improvement in the return on equity delivered by these companies.

A report dated 31 January 2024 in Mint points out that in 2023, Apple’s India revenue only “from iPhones fell just short of the $10 billion mark," with the company shipping more than 10 million iPhones for the first time.

In addition, as the Goldman Sachs report points out: “Only ~4% of India’s working age population has a per capita income of over US $10,000, projecting to ~60mn consumers…If the current trajectory continues, we expect ‘Affluent India’ will grow to ~100mn consumers by 2027."

These and more reasons are offered to make a case for the increasing premiumization of the Indian economy and how that will continue to benefit the stock market. But is that the case? Or is it just a small part of the economy that is getting premiumized? The British economist Joan Robinson once said: “Whatever you can rightly say about India, the opposite is also true." So, it is important to look at the other side as well.

The opposite

Private consumption expenditure, which over the years has formed around 56-58% of the Indian economy, is expected to grow 4.4% in 2023-24, the slowest since 2002-03 when it had grown 2.9%, except for the pandemic year of 2020-21 when it had contracted 5.2%. Clearly, a significantly large section of the population is struggling. Or as Hindustan Unilever, one of the largest fast moving consumer goods companies, recently stated: “Rural consumer sentiment remains subdued." Or as a news report in Mint stated, quoting Krishnarao Buddha of Parle Products: “Both rural and urban markets have slowed down." Sustained high food inflation is one big reason for this.

Further, from April 2023 to January 2024, firms sold 14.97 million two-wheelers in the domestic market. If this pace continues they will end up selling close to 18 million units in 2023-24, significantly better than the 15.86 million units sold in 2022-23, but still well short of 21.18 million units sold in 2018-19. Also, entry level two-wheelers, like entry-level cars, aren’t selling well.

Further, as per the Road Transport Yearbook 2019-20, cars, jeeps and taxis formed 13.8% of vehicle population in 1991. In 2020, they formed 13.4% of the vehicle population. During the same period, the proportion of two-wheelers increased from 66.4% to 74.7%. So, three out of four vehicles are two-wheelers. This may have marginally changed in the last few years as two-wheeler sales have slowed down and cars may now form more than 15% of India’s vehicle population, but trying to pass this off as premiumization of the entire Indian economy is a little too much. Of course, vehicle numbers in absolute numbers would have gone up.

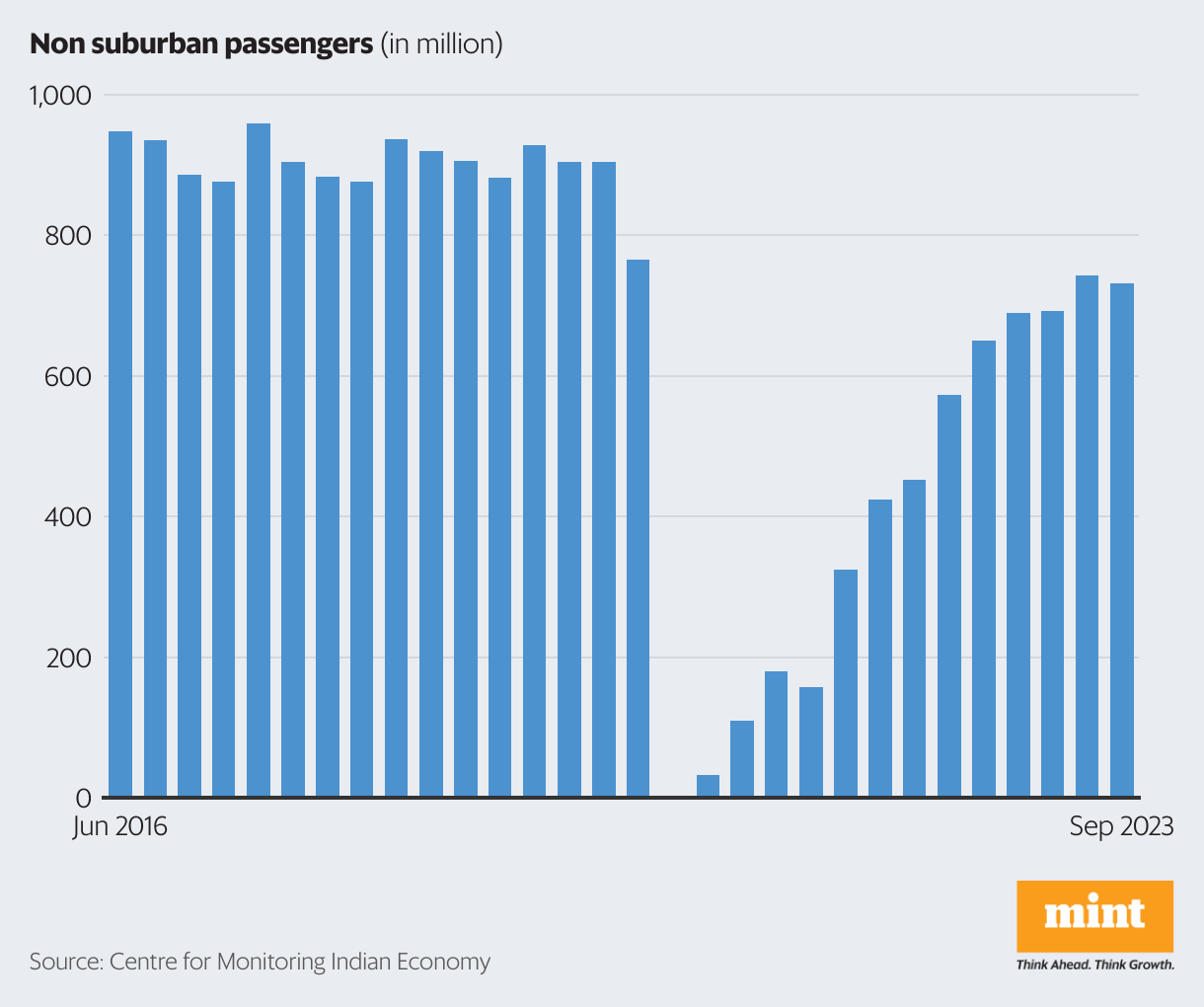

Now, let’s take a look at chart 1, which plots the number of passengers using the Indian Railways (non-suburban), every three months. While the number of passengers has improved post the pandemic, it still isn’t anywhere near where it was before the pandemic.

From April to September 2023, the latest data available, around 1.47 billion individuals travelled the Indian Railways. At this pace 2.94 billion passengers will travel the Railways by the end of the current financial year. Now, compare this to the more than 150 million passengers expected to travel by air. That is around 5% of non-suburban railway travel. How can any premiumization story not take the 95% into account?

Also, 2.94 billion people will be lower than the 3.65 billion people who travelled in 2018-19 and 3.94 billion in 2012-13, but higher than 2.6 billion in 2022-23. In addition, as the Indus Valley Report of 2023 pointed out, 1% of Indians account for 45% of flights. Moving on to, the rise in demat accounts, which is a welcome development, but as has been often pointed out, a bulk of the demat accounts have very small amounts invested in stocks. At the same time, more Indians are punting in derivatives than ever before. As a recent Bloomberg news report pointed out: “In 2023, Indian investors traded more [options contracts] than anywhere else in the world." Retail investors make up for 35% of these trades. As the news report further pointed out: “The average time an Indian trader holds an option is less than 30 minutes."

So, why are so many individuals busy speculating, and losing money in the process, instead of doing proper jobs? Data from Securities and Exchange Board of India shows that 90% of investors lose money while trading options and other derivatives. This, of course, needs deeper research, but trying to pass this off as premiumization is clearly suspect.

As far as the growing popularity of the Apple iPhone is concerned, data from Counterpoint, a market research firm, tells us that shipments of smartphones in India remained flat through 2023 at 152 million units. Also, rural tele-density has remained flat for many years and urban tele-density has been falling.

It need not be said that an increase in UPI transactions makes things easier for those selling and buying, but what does it mean beyond that? Earlier these transactions were largely happening in cash. But how does this signify that more economic transactions are happening, given that we have no idea of how many such transactions were happening in cash earlier.

Also, the number of credit cards going up needs to be looked at in the larger scheme of things. First, as a proportion of total number of cards (credit and debit cards), credit cards stood at around 8% in December 2022. In December 2023, they stood at 9.2%. A definite improvement. Nonetheless, with the rise of UPI payments, the need for owning a debit card has gone down.

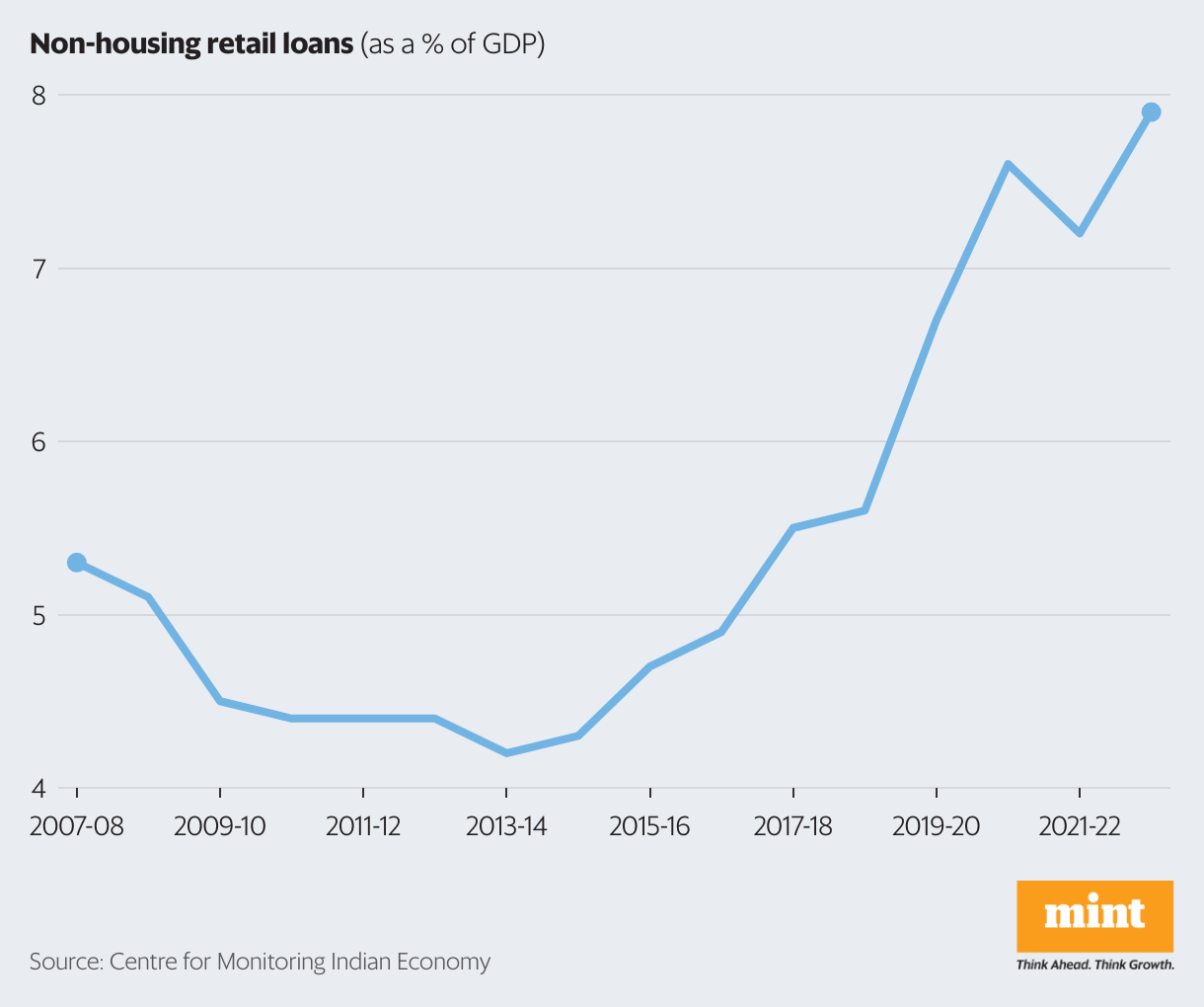

Second, look at chart 2, which plots non-housing retail loans given by banks as a percentage of the gross domestic product (GDP). These loans have gone up from 5.62% of the GDP in 2018-19 to 7.89% in 2022-23. This is primarily on account of an increase in credit card outstandings and personal loans. At one level, this might show the confidence people have in their future and the ability to repay their loans. At another level, it can also show that people have had to borrow to finance their consumption. This is reflected in the fact that the household financial savings have fallen from 7.9% of the GDP in 2018-19 to 5.05% in 2022-23. So, a part of the premiumization that is happening, like youngsters buying iPhones—a depreciating asset—is through individuals taking on higher loans. Of course, this anomaly is probably being set right in 2023-24, with people spending less and saving more. Also, the falling household financial savings figure includes the rising investment in stocks and equity mutual funds.

As far as the sale of 12,953 luxury homes is concerned, in a country of 280 million households, it doesn’t tell us much. Also, banks are now giving out more non-priority sector home loans (in absolute terms) to finance costlier homes, than priority home loans to finance affordable ones.

Let’s look at a few more data points. Work demanded under the work guarantee scheme, the Mahatma Gandhi National Rural Employment Guarantee Scheme, from April 2023 to January 2024, has been the highest in any year except the pandemic periods of April 2020 to January 2021 and April 2021 to January 2022. The scheme is self-selecting, i.e., only those who want to do manual unskilled work can volunteer for it. The high demand for such work indicates that there is some trouble on the jobs front.

Further, as per the government’s Periodic Labour Survey for 2022-23 (from July 2022 to June 2023), 45.8% of the labour force works in agriculture, a jump from 42.5% in 2018-19, though there has been a fall from 46.5% in 2020-21. As a country moves from being a developing country to becoming a developed one, the proportion of people working in agriculture comes down. In India’s case, this proportion has gone up in the aftermath of covid. Now, agriculture has huge disguised unemployment, meaning that there are way too many people trying to make a living out of it. Nevertheless, their employment is not wholly productive and the production won’t suffer even if some of these people stopped working.

Given these reasons, it’s hardly surprising that in late November, the central government extended the scheme providing free food grains to over 813 million beneficiaries under the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY) for a period of five years with effect from 1 January 2024. What this clearly tells us is that a large number of individuals still haven’t recovered from the economic aftershock of the pandemic.

Small part of the whole

To conclude, while the premiumization story might be a good one to sell for the stock market wallahs, it’s just a very small part of the whole story.

As the American writer F. Scott Fitzgerald once wrote: “The test of a first-rate intelligence is the ability to hold two opposing ideas in the mind at the same time, and still retain the ability to function." But that’s very difficult to do.

The small premiumization that is happening might end up creating opportunities in the stock market. Nonetheless, selling an investment thesis to the world at large on the basis of just that—when the broader consumption story of the Indian economy is not a very good one—is difficult. Hence, the premiumization story has been sold as it has been sold. And an answer to a simple KLH question cannot encapsulate all the nuance or the fact that the prospects of the broader economy can be different from the prospects of the stock market.

Vivek Kaul is the author of Bad Money.