Ambuja Cements’ Penna acquisition could take time to bear fruit

")

- Until then, Ambuja's investors need to brace for a drag on profitability because of Penna Cement's weak financial performance

With an eye on the southern markets, Ambuja Cements Ltd last week announced plans to acquire Hyderabad-based Penna Cement Industries Ltd.

Penna has a cement manufacturing capacity of 14 million tonnes per annum, including capacity still under construction, across Andhra Pradesh and Telangana. The acquisition is expected to contribute to Ambuja’s goal of reaching 140 mtpa capacity by 2027-28, from 93 mtpa currently, including the new capacity from the Penna acquisition.

But there are some dull spots that indicate that the Penna acquisition could take time to yield the desired results.

The Ambuja management has guided for more than 15% return on capital employed (RoCE) by the third year of the acquisition. But the internal rate of return (IRR), which is a better gauge for evaluating an acquisition, is unlikely to be enticing enough.

IRR captures the time value of money, unlike RoCE. IRR could be lower than the guided RoCE because improvement in Penna’s operations would be gradual as some capacity is still under construction.

Also, cement is a regional-focused industry. With freight costs accounting for 20% of the total cost on average, the movement of cement from one region to another is restricted.

In terms of regional comparison, India Cements Ltd is Penna's closest comparable listed regional peer, with a total plant capacity of 14.4 mtpa (57% in Andhra Pradesh and 32% in Tamil Nadu).

The enterprise value (EV) of the Penna deal is ₹10,422 crore, which is almost at par with India Cements’ ₹10,500-crore EV. The net debt of Penna is about ₹3,500 crore, according to Ambuja management.

That leaves Penna's equity value or market capitalization at ₹7,000 crore, which nearly matches the market capitalization of India Cements.

A point to ponder is if India Cements is considered expensive. Almost all analysts having a ‘sell’ rating on the stock. So Ambuja's acquisition of Penna is also expensive from the perspective of portfolio investors.

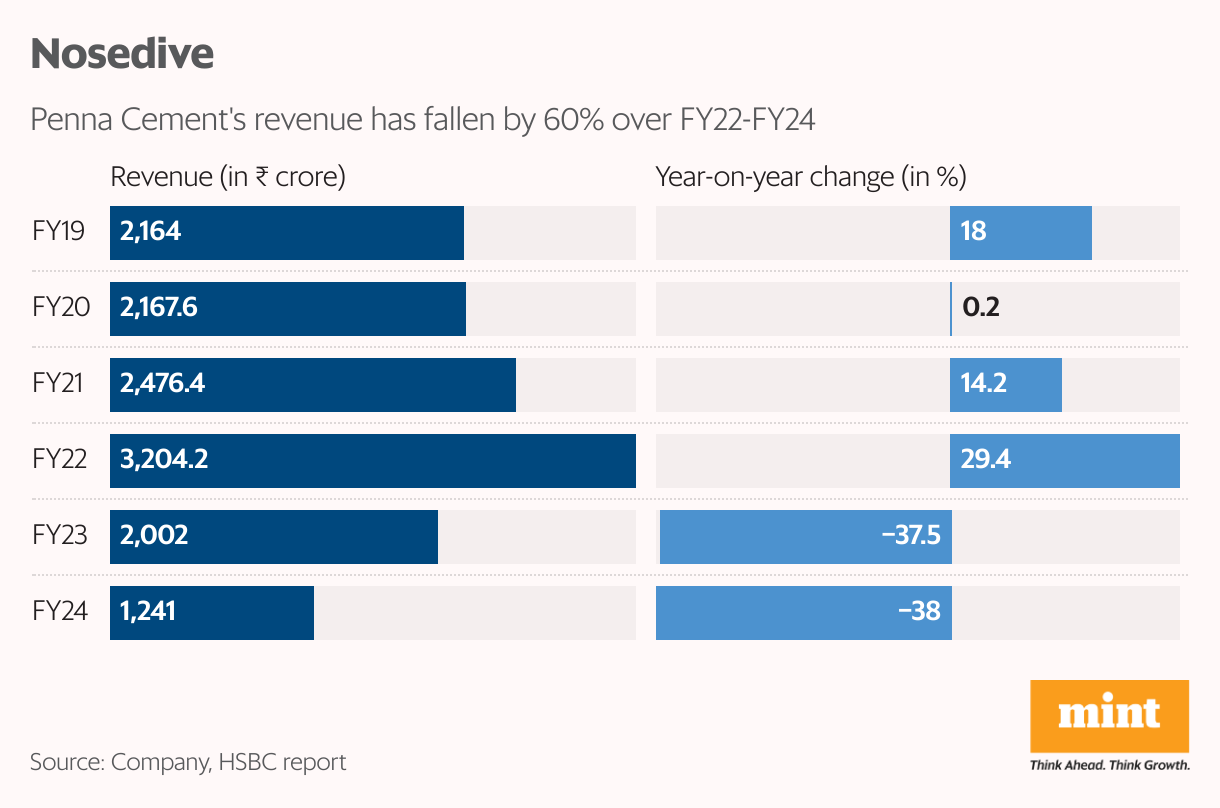

Also, Penna's capacity utilization is estimated to have dropped to 25% in FY24 from 65% FY22, as it was starved for cash to operate at a higher scale. Ambuja's management appears confident of correcting that with its own strong balance sheet.

Ambuja aims to improve Penna’s cement price realization by ₹5 to ₹10 per bag leveraging the premium for the Ambuja-ACC brands. (One cement bag weighs 50 kg.) Apart from that, there is scope for cost-reduction using synergies with the Adani group’s other cement plants.

But Andhra Pradesh and Telangana are witnessing increased competitive pressures with demand lagging supply, keeping cement prices muted. So, meeting the targets on realizations and capacity utilizations may be easier said than done.

In short, Ambuja's investors need to brace for a near-term drag on profitability, hurt by Penna's weak financial performance.