Defence stocks are soaring again, but can fundamentals support the rally?

")

Defence stocks have rallied sharply on export growth and budget boosts, but stretched valuations and slowing order inflows suggest cautious optimism for sustained gains ahead.

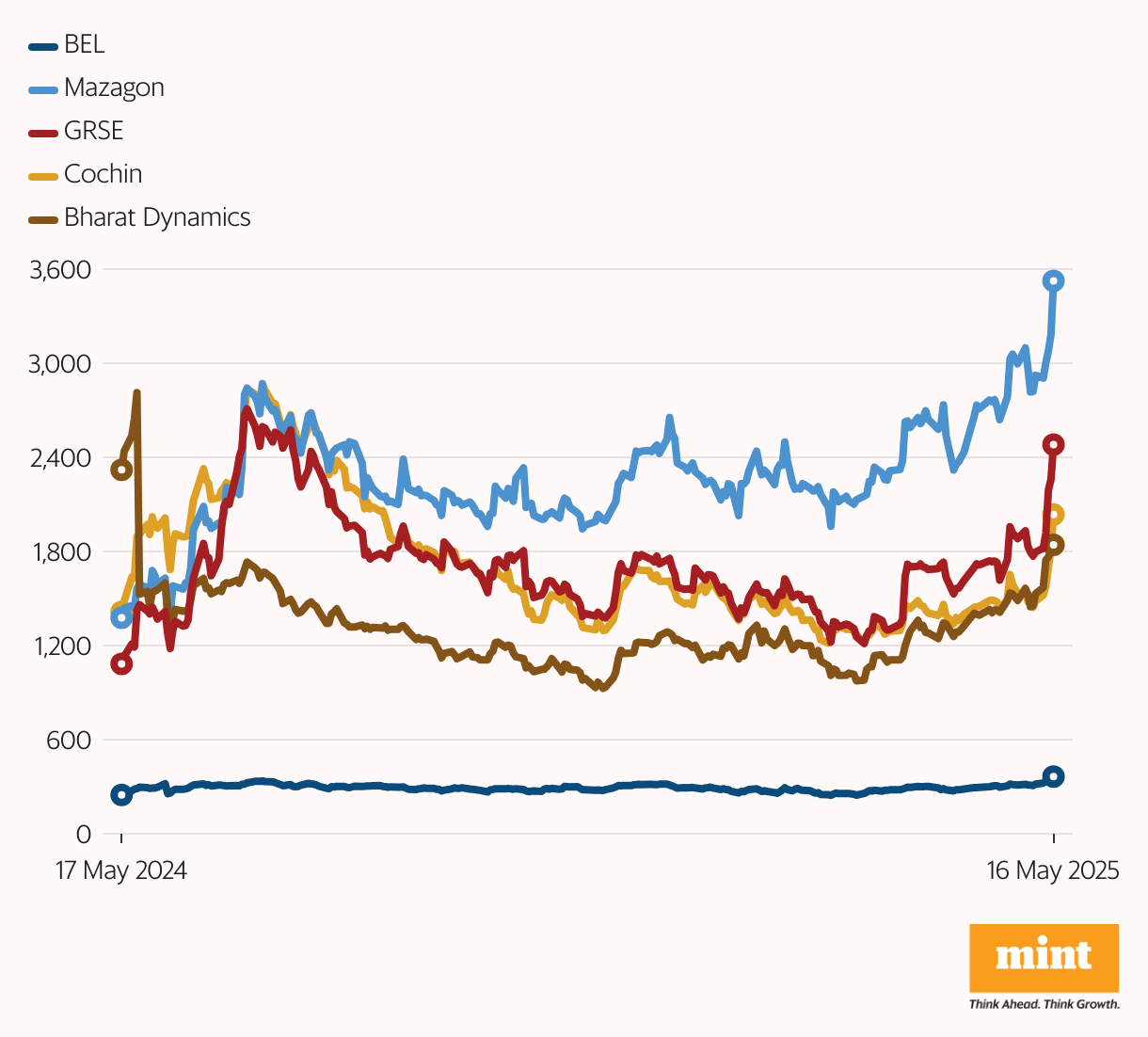

India’s defence stocks are back in the spotlight. After cooling off for nearly a year, the Nifty India Defence Index soared nearly 15% last week, hitting a record high of 8,309 on 16 May—eclipsing its previous July 2024 peak.

Garden Reach Shipbuilders led the charge with a 37% jump, followed by Cochin Shipyard (35%), Paras Defence (28%), Mazagon Dock (19%), and Bharat Dynamics (18%).

With defence stocks back in the spotlight, the big question is—what’s driving this sudden surge, and can it sustain?

We break down the key triggers behind the rally and assess whether it has staying power.

What's behind the surge in defence stocks?

Operation Sindoor was a key trigger for India's defence manufacturing ambitions. It underlined the strength of its indigenous capabilities and drew global attention.

Several countries are now reportedly in talks to purchase the BrahMos missile system. Russia has also proposed manufacturing its S-500 missile defence system in India.

Also read: Indian defence firms skyrocket after Pakistan skirmish

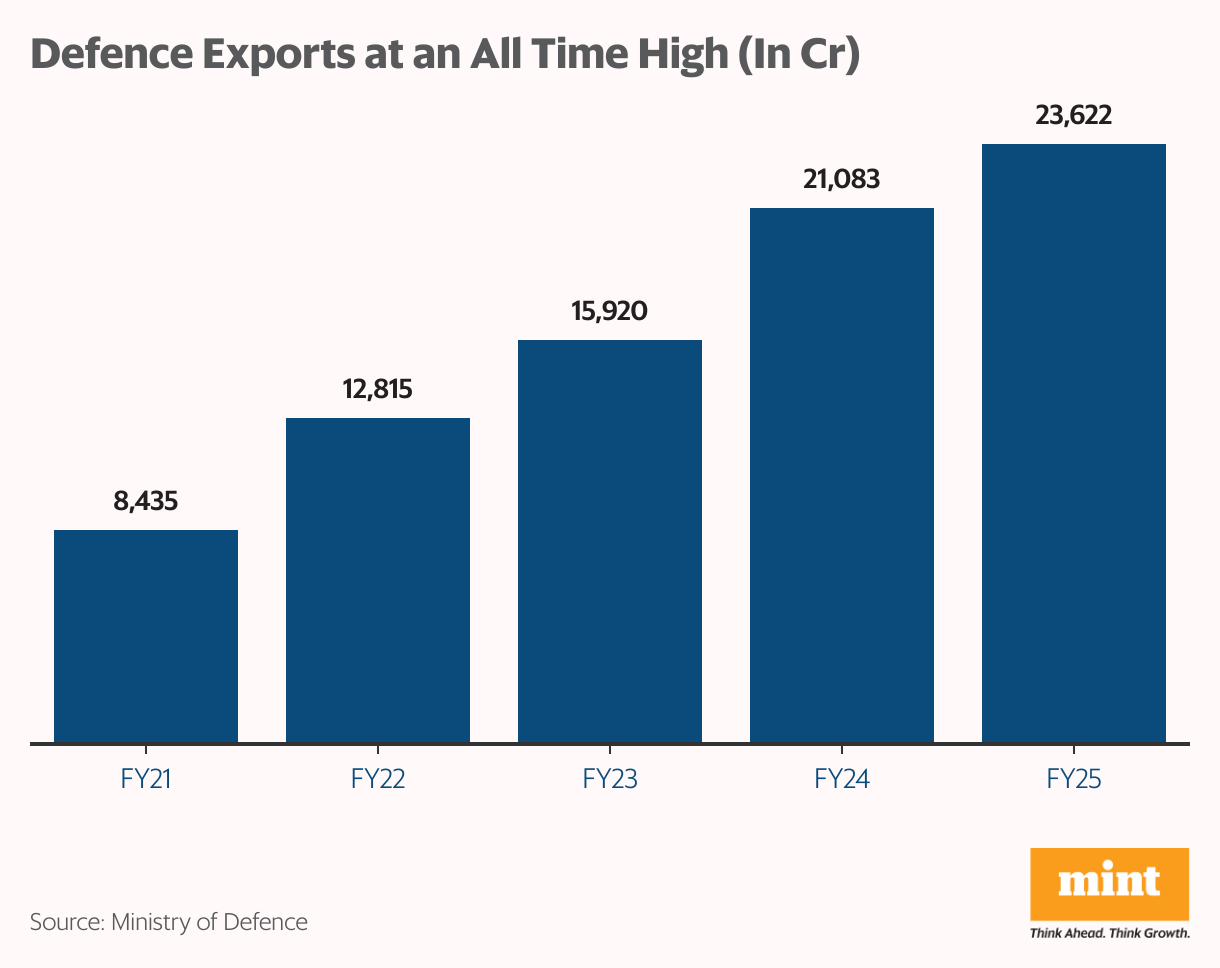

India’s defence exports hit a record ₹23,622 crore in FY25—nearly triple FY21 levels—and are projected to more than double again to ₹50,000 crore by FY29. Exports surged 12% from last year and have nearly tripled from ₹8,435 crores in FY21.

Most of this growth came from defence public sector undertakings (PSUs), whose exports rose 43% to ₹8,389 crore. This shows that indigenous defence products are gaining acceptance globally. However, the private sector’s export remained flat at ₹15,233 crore. Despite that, they account for 64.5% of the total, while PSUs contribute the remaining 35.5%.

India is also eyeing major export markets in Southeast Asia, Europe, and Africa—a shift that could open up new opportunities. The sector is also expected to benefit from NATO's planned spending of €800 billion over the next 3-4 years. Indian companies, mainly private players, will likely benefit from this increased spending.

According to Nuvama, global defence spending is expected to grow at a compounded annual growth rate (CAGR) of 5% to $3.2 trillion in CY28, from $2.4 trillion in CY23. This suggests a long runway for export-driven growth and may remain a key driver of the ongoing rally.

Budget boost

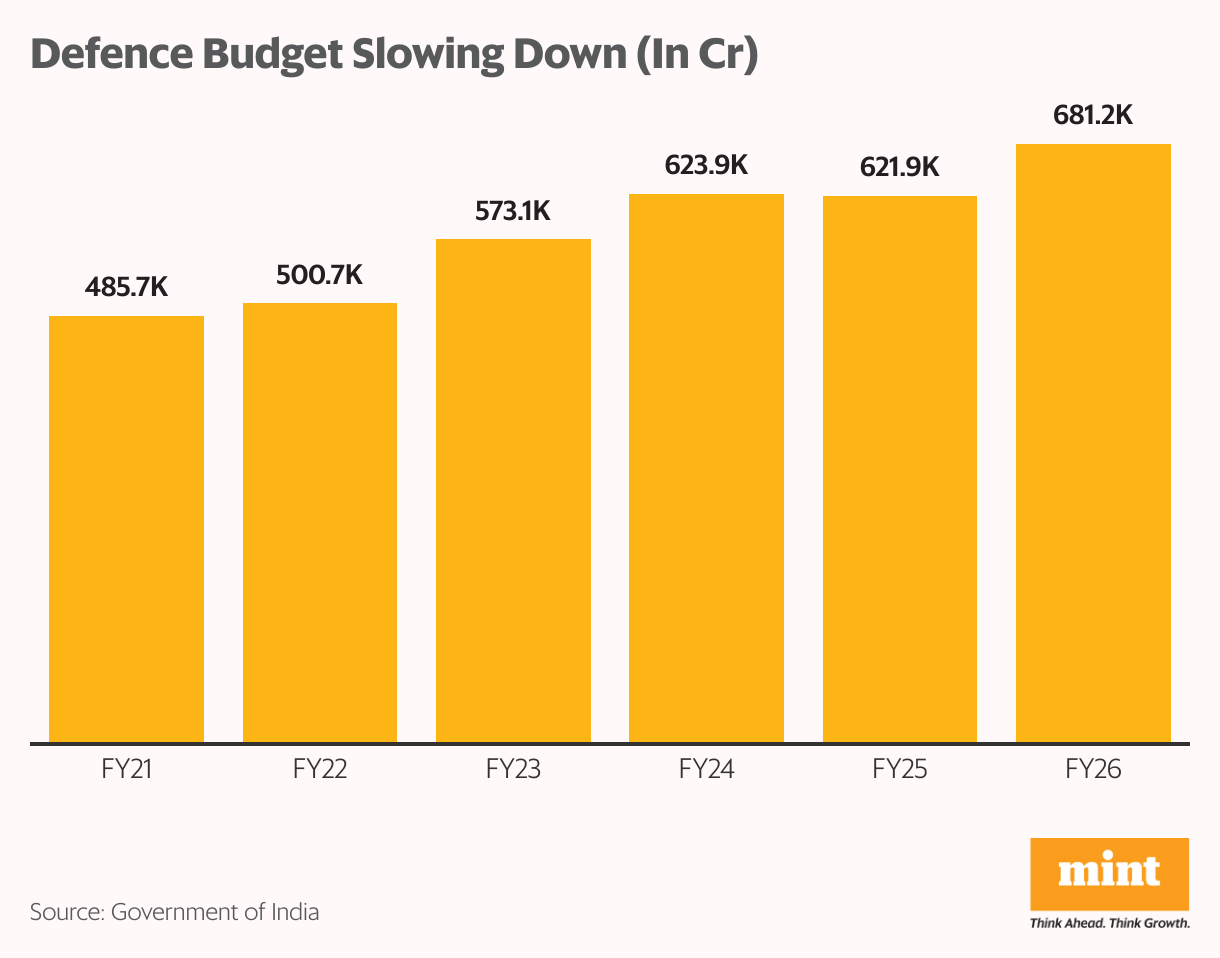

India's FY26 defence budget may see a significant boost with a potential ₹50,000 crore supplementary allocation, raising the total to ₹7.3 lakh crore from the initial ₹6.8 trillion.

This is expected to fuel defence research and weapons procurement, particularly benefiting indigenous manufacturing. But with valuations now stretched, investors may need to weigh optimism against earnings visibility.

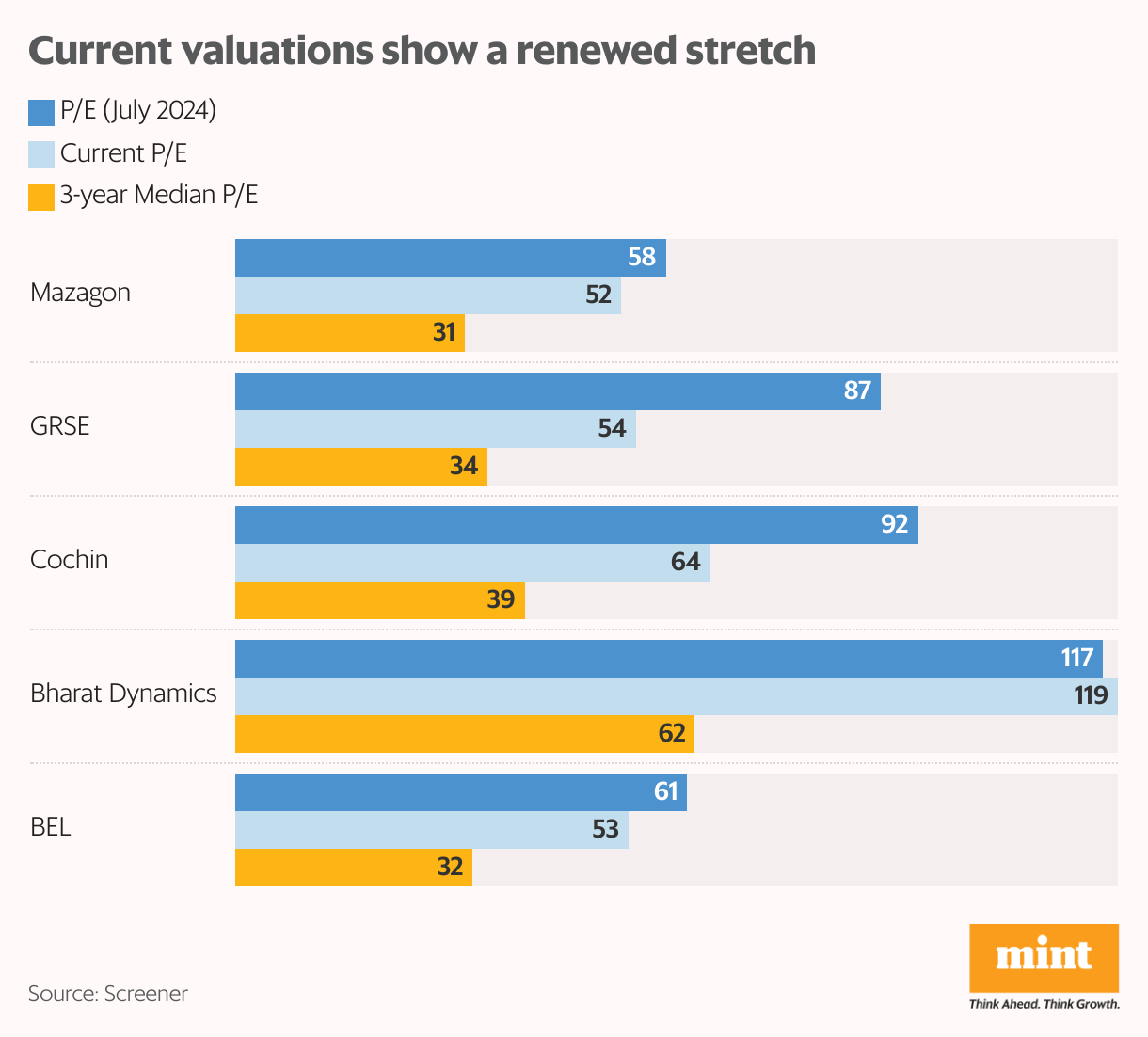

Valuations: Back in the danger zone

This period saw a significant rerating of defence stocks (June 2023-July 2024). The rally was driven by low initial valuations, strong order inflows, better earnings visibility, and supportive government policies.

However, this led to frothy valuations by July 2024, triggering a sharp correction where some stocks fell up to 50% before stabilising around their 3-year median P/E ratios.

The recent rally has once again pushed valuations well above the historical average, setting a high bar for earnings growth. Take BEL, for instance– it's currently trading at a P/E of 53, implying investors are paying ₹53 for every ₹1 of profit. The valuation factors in a lot of earnings optimism.

However, recent earnings show mixed performance. In FY25, Cochin Shipyard's profit surged just 3.6% from last year. Garden Reach Shipbuilders & Engineers Ltd (GRSE) fared better, reporting 46% profit growth, while Bharat Dynamics' profit declined by 15% in 9MFY25. Mazagon and BEL were the exceptions, with 64% and 46% profit growth, respectively.

Still, except for Mazagon, these growth rates failed to justify their high P/E multiples. Improving earnings from a high base of FY25 will also be challenging. Another concern is the limited free float in many defence PSUs, which can distort price movements.

For example, the Government of India holds 84.8% in Mazagon Dock, well above the 75% shareholding norms. This limits price discovery, allowing relatively small buying volumes to increase prices. It's not a surprise that Mazagon's share price has surged by about 10x in the last two years.

Also read: Operation Sindoor: What's next for Indian defence stocks?

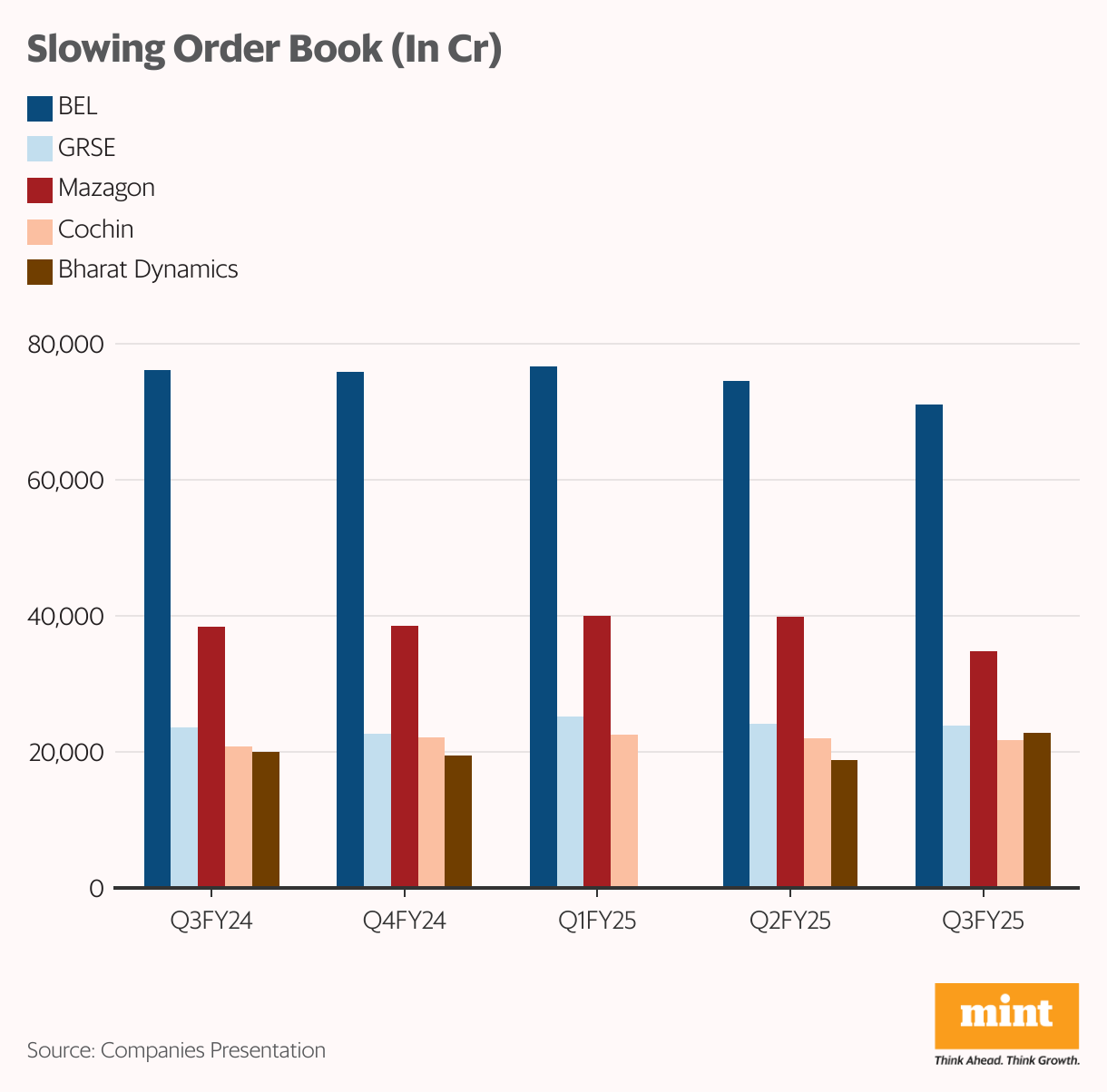

More importantly, the earnings outlook now hinges on the strength of future order inflow. However, recent data suggests that order inflows may be slowing. This poses a risk to sustaining the current valuation levels, especially since much of the existing order book may already be priced in.

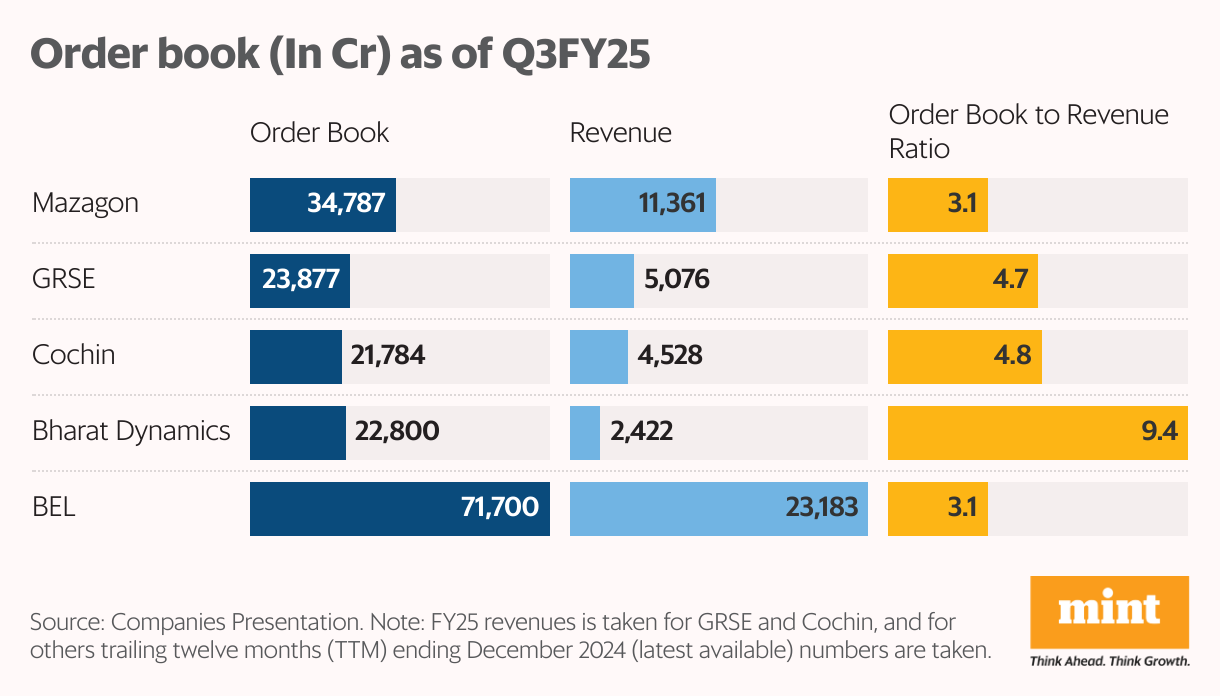

Order book trends

On the surface, order book-to-revenue ratios appear healthy across most defence companies and offer revenue visibility. However, a close look shows that the momentum in fresh orders has slowed over the last 12 months, partly due to elections-related disruption in FY25.

Note: FY25 revenue data is used for GRSE and Cochin Shipyard; for other companies, the trailing twelve months (TTM) revenue ending December 2024 is considered.

Adding to the sector's slowdown, the Union Budget 2025 allocated ₹1.8 trillion for military modernization capital expenditure in FY26, a modest 4.6% increase. This limited growth suggests potential constraints on near-term order inflows for defence companies.

Company-level data supports this trend. Bharat Electronics Limited (BEL)'s order book decreased to ₹71,100 crore in Q3FY25 from ₹76,200 crore in Q3FY24. Garden Reach Shipbuilders & Engineers (GRSE)'s orders peaked at ₹25,231 crore in Q1FY25 and subsequently fell to ₹23,877 crore. Mazagon Dock Shipbuilders and Cochin Shipyard also experienced similar declines in their order books.

While Bharat Dynamics saw its order book rise, its revenue declined from ₹2,817 crore in FY22 to ₹2,369 crore in FY24, though net profit grew modestly by over 20% to ₹613 crore. Its TTM figures show revenue at ₹2,422 crore and profit at ₹566 crore. Despite this mixed financial performance, BDL's stock delivered an impressive 73% CAGR between FY22 and FY25.

Also read: Hindustan Aeronautics: Here’s all you need to know before investing

BEL demonstrated relatively stronger financials with a 13% revenue CAGR and a 24% profit CAGR over the same period, resulting in a 67% stock return CAGR.

However, the shipbuilding companies significantly outperformed both BDL and BEL. Mazagon Dock Shipbuilders led with a 33% revenue CAGR and a 47% profit CAGR, and its stock price soared with a 190% CAGR. GRSE and Cochin Shipyard also witnessed their stock returns substantially exceed their financial growth, with GRSE compounding at 102% and Cochin Shipyard at 132%.

Taken together, the data reveals a divergence. Barring Mazagon and GRSE, most companies have not seen an equivalent improvement in earnings. Yet, stock prices have surged, pushing valuations higher. That sets a high bar for future performance and leaves little room for disappointment.

What's next?

BEL management expects an order inflow of ₹25,000 crore from the Army and ₹15,000 crore from the Navy in FY26. Motilal Oswal Financial Services estimates an order inflow of ₹36,000 crores (in FY26) and ₹41,400 crores in FY27.

Execution remains the key for Bharat Dynamics. Despite a strong order book, its execution remains patchy, mainly due to dependency on imported components. Nuvama expects about ₹32,000 crore of orders in FY26 and ₹24,000 crore in FY27.

Shipbuilders may see stronger momentum. Antique estimates Mazagon's order book to grow to ₹1.3 trillion by FY27–3.7 times its current order book. GRSE's order book could swell to ₹1.2 trillion by FY27—about 5 times its current book.

These inflows are crucial to justify the current valuation, as they can provide long-term revenue visibility. However, execution will still be key. Still, near-term earnings may slow down due to lower order flows, and higher base of FY25, which would be tough to beat.

To conclude, the long-term prospects for the defence sector remain promising. But stretched valuations leave little room for error. This becomes even more challenging given the high base set in FY25, especially as order inflows have slowed. To sustain the rally, free order inflow and executions must accelerate.

Also read: Drone startups looking beyond defence to serve agriculture, quick commerce

About the author: Madhvendra has over seven years of experience in equity markets and has cleared the NISM-Series-XV: Research Analyst Certification Examination. He specializes in writing detailed research articles on listed Indian companies, sectoral trends, and macroeconomic developments.

Disclosure: The writer does not hold the stocks discussed in this article.

The purpose of this article is only to share interesting charts, data points, and thought-provoking opinions. It is NOT a recommendation. If you wish to consider an investment, you are strongly advised to consult your advisor. This article is strictly for educational purposes only.