HDB IPO: How investors may read India's biggest offer of the year

")

As HDB Financial's grey market price is now close to the IPO price, the focus now shifts towards bad loans, profitability and how it compares with peers.

HDB Financial Services Ltd.’s ₹12,500 crore initial public offering, the largest so far this year, will test investor appetite for fresh scrips in a dull market.

The three-day initial public offer (IPO), which opens on Wednesday, has priced shares of the non-banking financial company (NBFC) at ₹700-740 apiece. While that was a 40% discount to its grey market price before the IPO was announced, prices in the two markets have converged. The focus now shifts towards its fundamentals.

Low returns

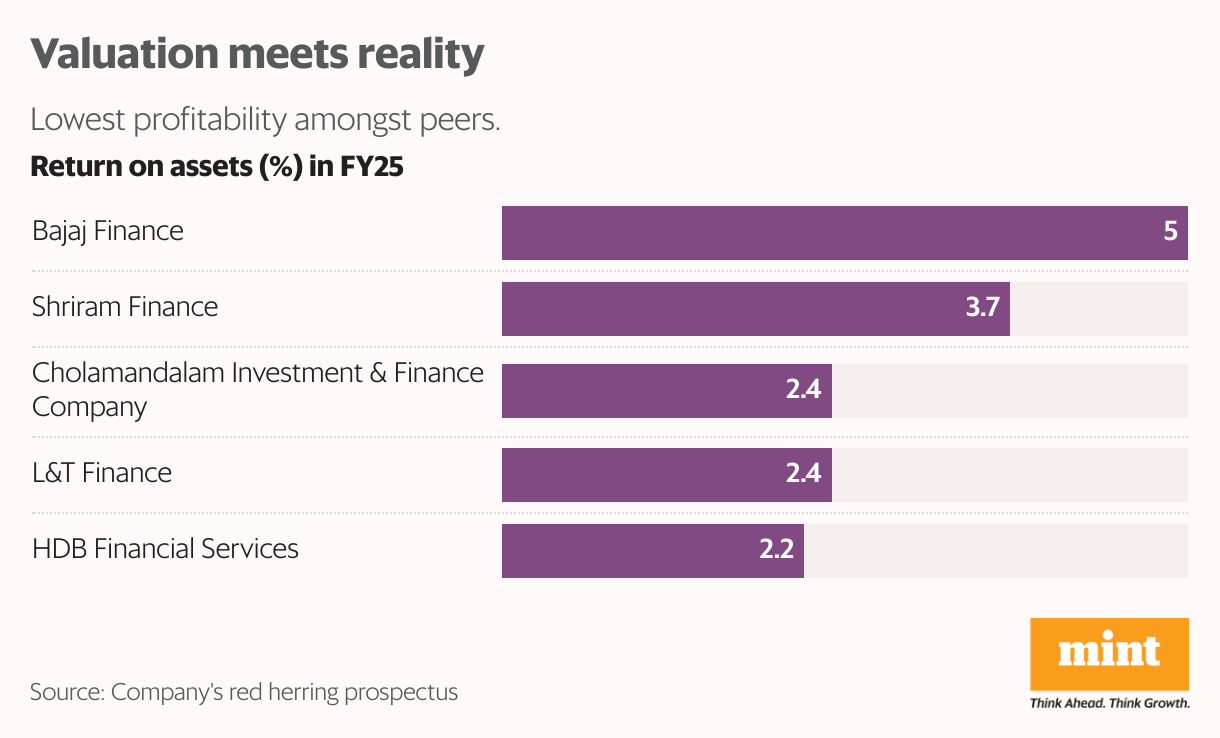

With one of the lowest return on assets (RoA) among key listed peers in FY25, HDB’s profitability lags that of its competitors because of the rising cost of operations and managing bad loans, its red herring prospectus showed.

HDB’s issue price adequately reflects the risks of its relatively lower RoA and higher credit cost and gross non-performing asset (GNPA) ratios, said Narendra Solanki, head of fundamental research at Anand Rathi Shares and Stock Brokers’ investment services division. “As such, its more profitable peers are valued at least 40-50% higher in terms of their (FY25) price-to-book (P/B) ratios."

HDB Financial has been valued at 2.7 times its expected average loan book value in FY27, while its much larger competitor,Bajaj Finance, trades at 4.3 times its FY27 P/B ratio, said analysts.

Bajaj Finance, India’s largest NBFC, has five times HDB’s customer base(19 million)and 4 times its loan book size ( ₹1.07 trillion) as of FY25—its major focus is on unsecured urban consumer lending. With a fully digital, high-margin operating model, the company stands out with the highest ROA of 5% and lowest GNPA of 1.2% among all peers.

Also read | Sebi raises concern over $1.5 bn HDB Financial Services IPO

In comparison, HDB Financial operates on a hybrid model, mainly targeting tier-4 and rural consumers, yielding an RoA of 2.1%, albeit with a higher GNPA of 2.3%. Since more than 70% of its borrowers are underserved, earn low income and have no credit history, their risk profile is also higher.

Growth opportunities

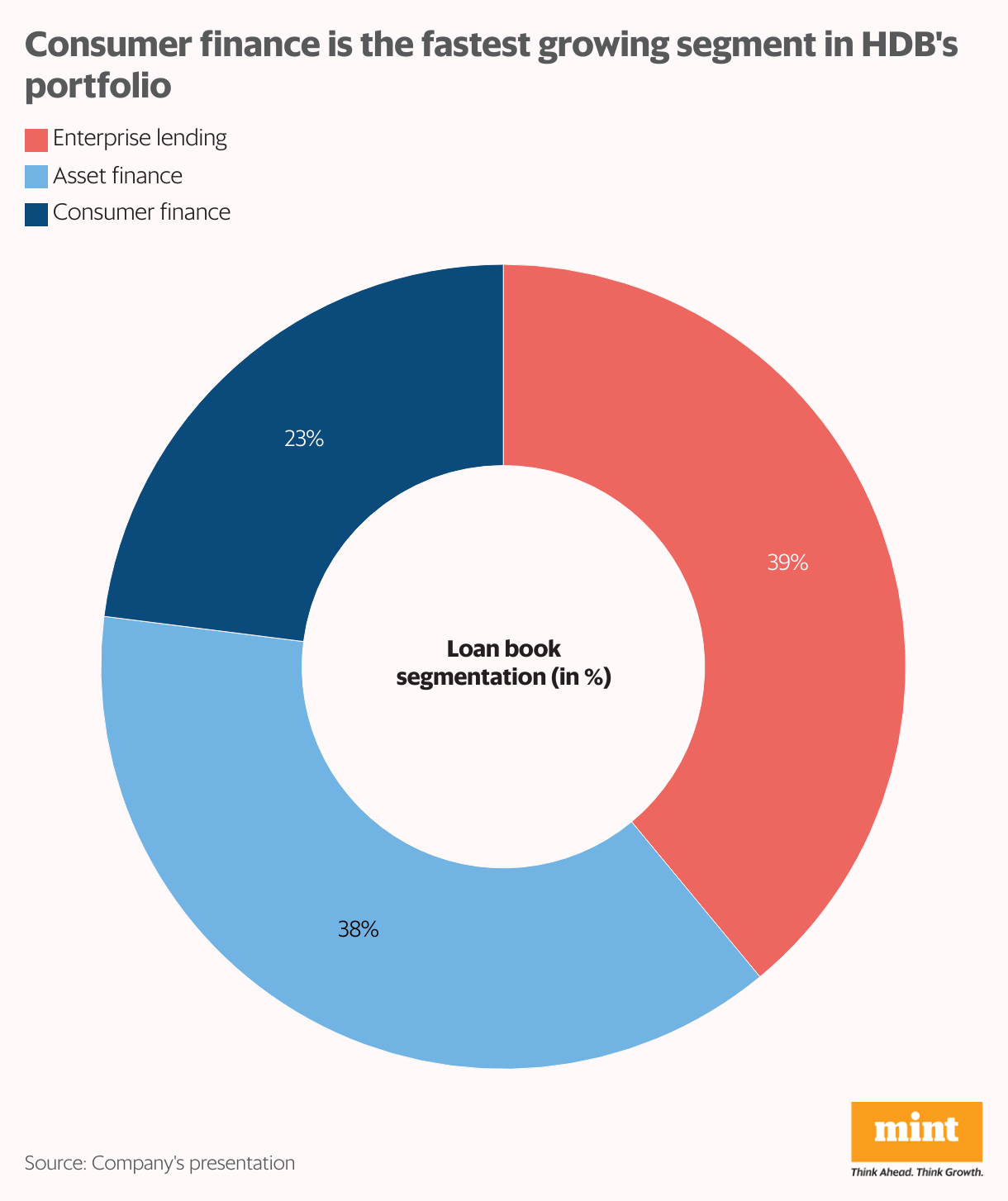

Still, analysts believe that HDB’s business has a long growth runway ahead as India’s digitization story and demand for credit are likely to penetrate deeper into the country’s hinterland in the coming years. The company’s customer base has grown at a compounded annual growth rate of almost 26% in the last two years, owing to its aggressive push into consumer lending.

“While all segments are poised for growth, our consumer finance business is set to grow relatively faster given the large market available in this space," Jaykumar Shah, chief financial officer at HDB Financial Services, toldMint.

To be sure, 73% of HDB’s FY25 loan book is still secured by collaterals like properties, gold and commercial vehicles. But the company has been increasingly disbursing more unsecured consumer loans since FY23, said an SBI Securities IPO note.

Read this | Why HDFC Bank turned down MUFJ's overtures on HDB Financial

According to Solanki from Anand Rathi Shares, consumer lending would likely continue to lead HDB’s growth in FY26 and beyond. “India remains a largely untapped market when it comes to providing financial services to retail borrowers in semi-urban and rural areas," he said. “HDB operates at a granular level and offers long-term growth potential, mainly driven by rural expansion and the strategic advantage of being part of the HDFC ecosystem."

Backed by HDFC Bank, HDB Financial enjoys a strong parentage pedigree. As a result, it is deemed an upper-layer NBFC with an AAA credit rating. It has access to low-cost funding from a wide range of lenders, including banks and the corporate bond market.

Pressure on NIM

However, at 7.9% interest rate, HDB’s average borrowing cost is 46-basis-point higher than Bajaj Finance’s and around 20-50 bps higher than that of secured vehicle financiers such as Sundaram Finance and Mahindra and Mahindra Financial Services. This ultimately impacts its net interest margin (NIM) or profitability.

However, analysts believe that the Reserve Bank of India’s (RBI) 100 bps rate cut so far since February, and the latest liquidity-easing measures will reduce HDB’s funding costs, along with those of other NBFCs. This should happen before they reduce interest rates for their borrowers, aiding their NIM expansion in the short term, according to analysts, because most NBFCs have a higher share of fixed-rate loans in their portfolios.

But the improvement may be gradual rather than immediate. JM Financial estimates mostly flattish-to-marginal (10-15 bps) NIM improvement in FY26 over FY25 figures.

Cost inefficiencies

Despite improving NIMs, HDB Financial’s profitability can still remain under pressure, analysts said. The company’s major weakness is its high cost of operations, reflected in the highest cost-to-income ratio among peers. This mainly arises from its back office services to HDFC Bank, said a recent Macquarie Equity Research report.

Also read | HDB Financial Services IPO: Two concerns that could hurt the HDFC Bank subsidiary’s valuation

The costs of business process outsourcing (BPO) services provided to HDFC Bank offset income generated from back office services offered to other clients, said the report. While HDB has been trying to control costs by significantly reducing its BPO team in FY25, its income from such services has also fallen. Macquarie notes that if the company’s cost-cutting efforts are not in line with the fall in income from this low-margin business, its profitability would be impacted harder.

The company’s rising credit cost is also likely to weigh on its profitability as the ongoing stress of bad loans continues to burden unsecured lenders across the industry. This is particularly visible in HDB’s credit cost and GNPA ratios, which rose 81 bps and 36 bps to 2.14% and 2.26% in FY25, respectively, according to its red herring prospectus.

Rising delinquency rates in the face of high inflation and sluggish income growth, particularly in the microfinance segment, led RBI to caution against unsecured consumer lending last year. As a result, HDB’s main source of strength has also turned into its weakness.

“Although MFI remains the most affected, some stress is emerging in other unsecured segments as well," said Solanki.

Hence, asset quality remains a key concern for HDB, with seemingly little respite ahead.

Also read | Rich valuation pricks Bajaj Finance as it cuts guidance

“As per our interactions with certain banks, (HDB’s) collection efficiency has not improved materially in Q1 as compared to last quarter," said Anusha Raheja, research analyst at Dalal & Broacha Stock Broking.

According to the JM Financial report, even foreign investors think that until the income levels of the larger population increase, there will be neither any material improvement in asset quality nor credit growth in FY26.

Moreover, HDFC Bank owns 94.4% of HDB Financial, and its stake would be diluted to around 74% after the IPO. Analysts anticipate an oversupply of HDB’s shares, limiting its upside potential. More so, if HDFC decides to reduce its share in the company to 20% in the next two years to comply with RBI’s proposed regulations on bank-owned NBFCs.

If HDFC’s stake falls below 51%, the NBFC could see funding costs rise and face branding-related issues, said Macquarie.

“We view the IPO as a tactical bet only, given the limited upside at current valuations and recommend caution until asset quality improves and operational efficiency gains traction," said broking firm Investec.

And read | Bajaj Finance pivots to profitability with AI, scales back payments ambitions