Startup IPOs have made a scorching comeback. Beware the optical illusion

")

- Ten new age companies have made their stock market debuts in 2024 so far, including Go Digit, Awfis and Ola Electric. Their shares have maintained momentum post listing as well. But investors must draw lessons from a lethal military formation described in the Mahabharata.

New Delhi: Kurukshetra. Eons ago.

Abhimanyu, the sixteen-year-old son of the mighty archer Arjuna, was displaying breathtaking bravery in the Mahabharata war. He not only killed a number of prominent warriors on the enemy side, but also managed to break the flagstaff of Bhishma, the supreme commander of the Kauravas, in a hugely symbolic moment.

The energy and momentum of youth was firmly holding sway over the grizzly veterans on the field.

After 12 days of fierce battle, the rattled Kauravas decided that something had to be done. A final test to separate the boys from the men.

The Kauravas then laid out the chakravyuh—a lethal military formation comprising a labyrinth of defensive walls, manned by their legendary fighters like Dronacharya, Karna, Duryodhana and others.

Abhimanyu, with his trademark spunk and velocity, smashed through the formation. However, unlike experienced warriors like his father, he did not know how to get out. The enemy knew this, and cynically exploited this fact, leading to the tragic death of the promising youngster.

And not for the last time, the promise and potential shown by a newcomer withered away in the face of a stern test.

A tale as old as time. But does this have any significance for the lakhs of investors shovelling money into one of the hottest segments of Dalal Street currently?

Start Me Up!

After a lull in 2023 and 2022, startup initial public offerings (IPOs) are back with a bang this year. A total of 10 new age companies have made their stock market debuts in 2024 so far, including prominent players like Go Digit, Awfis, ixigo, FirstCry and Ola Electric.

")

To put this in context, just three startups listed on the exchanges in 2022, followed by five last year.

“2022 and 2023 were marked by geopolitical tensions and a funding winter. While the former has not improved much, the latter seems to be over, as was attested by a record number of funds raised to support early-stage and growth-stage startups," said Gaurav V.K. Singhvi, co-founder at Avinya Ventures, a Sebi-approved venture capital firm.

This shift, coupled with the renewed focus among startups from merely chasing growth through substantial cash burn to actually pursuing profitability and positive unit economics has revitalized the IPO markets with new-age startups opting for public listings, Singhvi added.

That said, a bigger factor seems to be the conducive market conditions.

Just like promoters in other sectors, India’s new age companies are finding it hard to resist the siren call of this raging bull market.

“India is seeing a major mindset shift. It is one of those periods when bank interests are high, but individuals are not driven to making bank deposits. All of this money is flowing towards the capital markets either directly or through mutual funds. A clear indication of the level of interest is the substantial rise in demat accounts, which crossed 124 million by the first quarter of 2024. This domestic liquidity is the single biggest factor driving investments," Vishal Agarwal, partner at Grant Thornton Bharat, told Mint.

With the capital markets at historic highs, startup IPOs are seen as exciting new opportunities in companies that could represent the new way of doing business, he added.

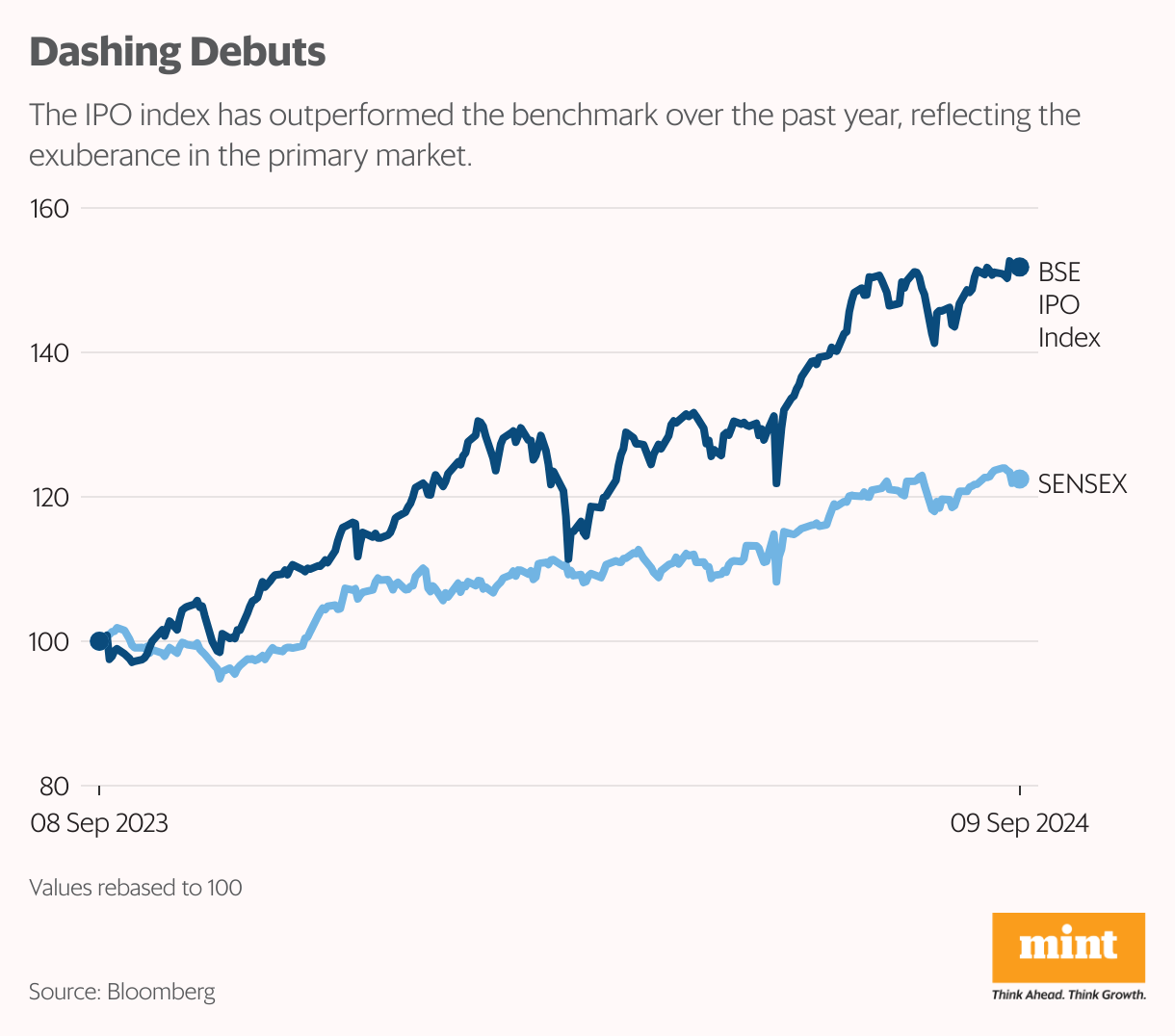

The Street’s enthusiasm for the GenNext of India Inc. can be gauged from the blockbuster listings of these players.

The IPO of e-commerce SaaS (software as a service) platform Unicommerce was oversubscribed a whopping 168 times, while that of co-working space provider Awfis saw oversubscription of more than 100 times. Even a mega issue like Ola Electric, which raised ₹6,145 crore, sailed through with oversubscription of 4.4 times.

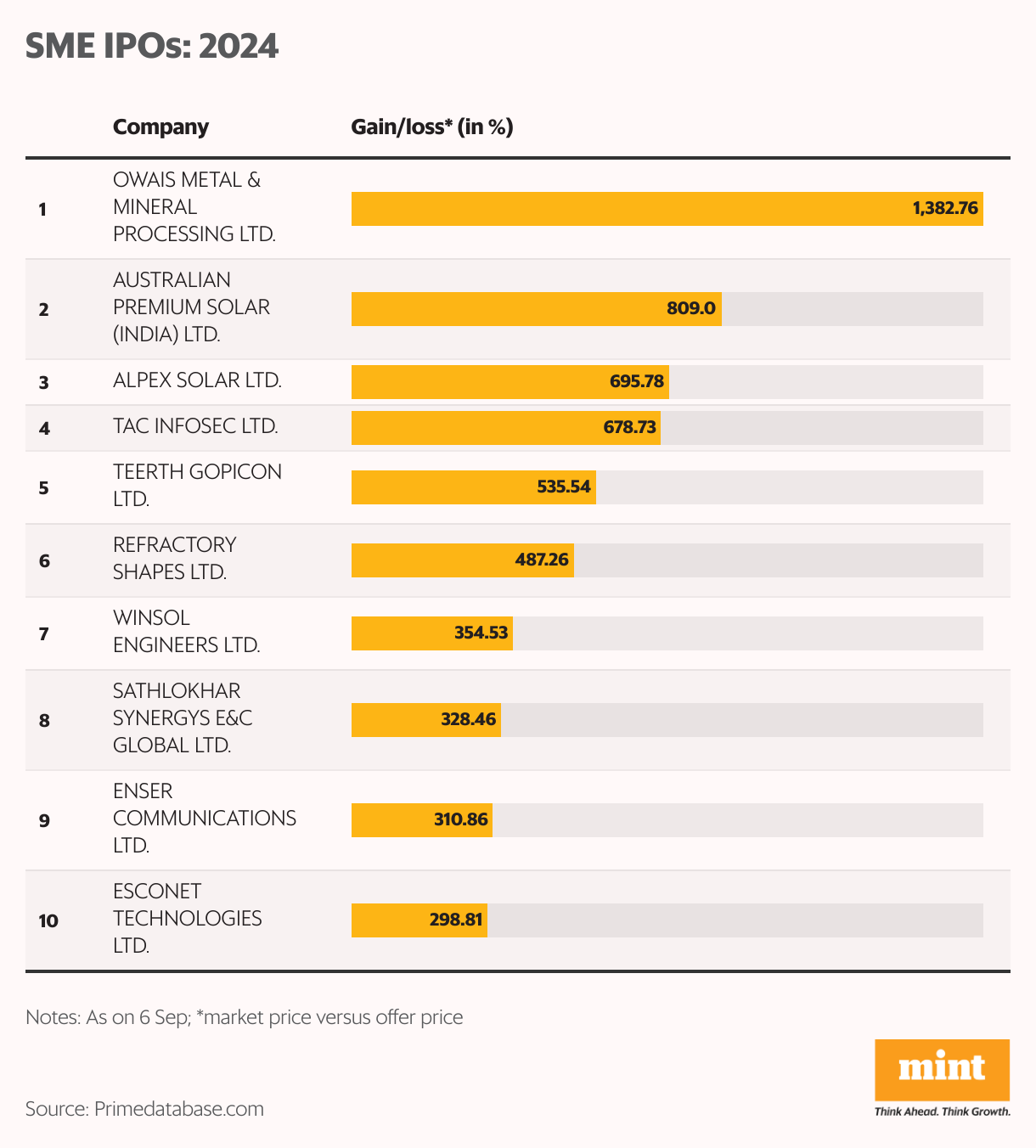

Meanwhile, small and medium-sized enterprises (SME) IPOs, which currently seem to be flouting all laws of mathematics as well as gravity, saw even more exuberant numbers. Cybersecurity startup TAC Infosec’s ₹30-crore IPO was oversubscribed 422 times and men’s grooming brand Menhood garnered bids for 200 times the shares it put on offer.

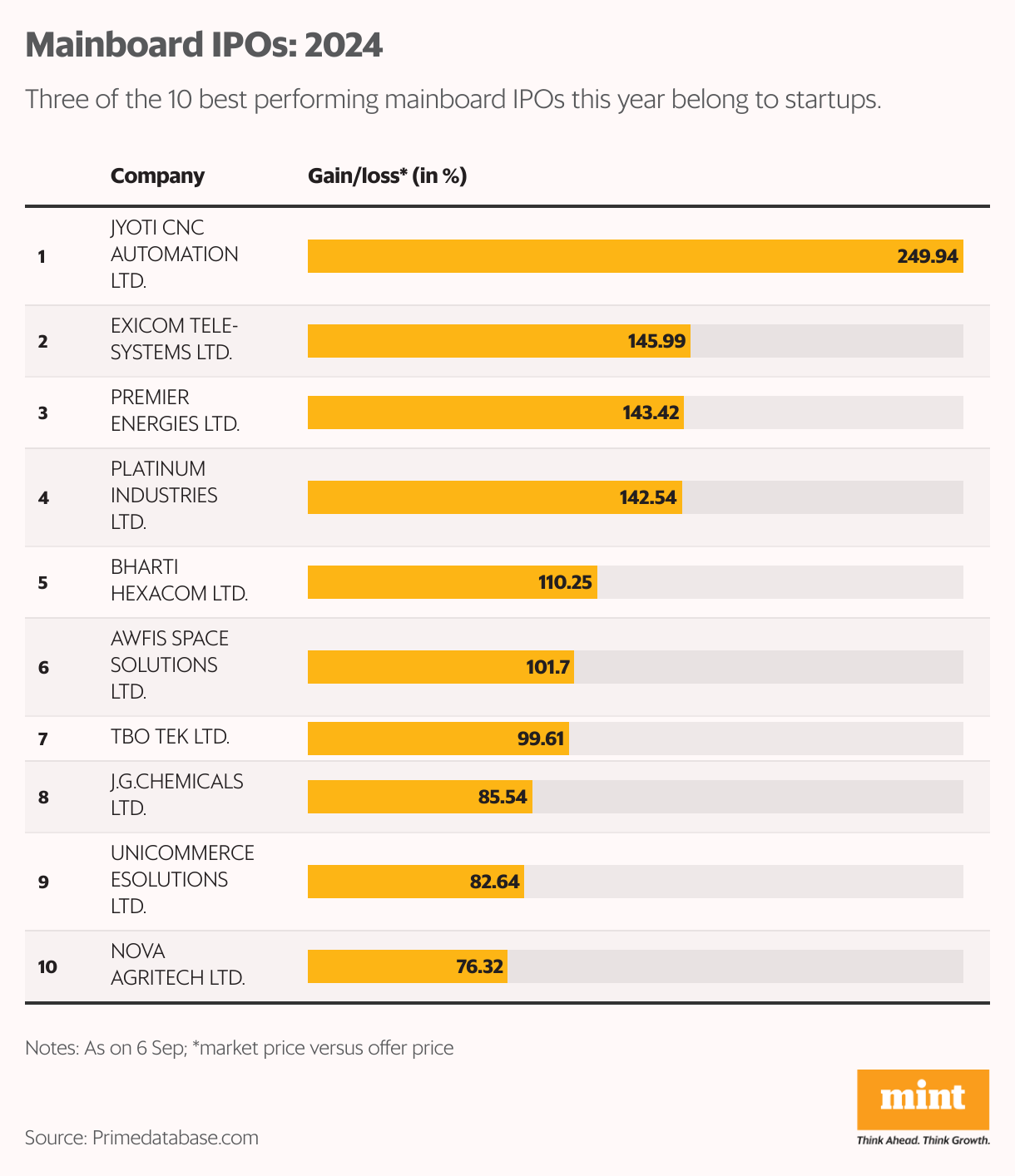

It is also not as if the flaming affair lasted only till the IPO period. Startup shares have maintained their momentum post listing as well. In fact, out of the 10 best performing mainboard IPOs of this year so far, three belong to new age companies—Awfis, TBO Tek and Unicommerce—all of which have soared about 100% within just three months.

TAC Infosec has delivered an astounding 640% returns—the fourth best performer among all SME debuts in 2024 so far.

Bull market exuberance in full display? No doubt. But surely some other factors are at play too?

Dial L for Liquidity

The metamorphosis of the Indian saver into an investor has been among the most far-reaching developments in the Indian economic landscape.

The number of unique mutual fund investors has swelled from 22 million in March 2020 to 47 million as of June 2024.

Similarly, the number of unique demat account holders has ballooned from 36 million as of March 2020 to nearly 100 million now.

This has unleashed the biggest force which drives markets higher—liquidity. Loads and loads of liquidity.

At an industry event in Mumbai last month, Ananth Narayan, market regulator Sebi’s whole time member, highlighted this very aspect.

“During the six years from FY16 to FY21, mutual funds, other domestic institutional investors (DIIs), and individuals net infused around ₹40,000 crores on average each year into our equity secondary markets. Since then, for the three years FY22 onwards, they have brought in on average around ₹3.1 trillion annually into our secondary markets—nearly eight times higher than before."

")

To be sure, these numbers are reflective of India’s stable macroeconomic environment, robust corporate earnings and an efficient technology architecture in the capital markets to enable the seamless onboarding of such vast number of investors.

That said, this huge tidal wave of liquidity is bound to have some second-order effects.

“The ₹3.1 trillion of net demand for paper brought in by mutual funds, DIIs and individuals into the secondary market every year the past three years, far exceeds the roughly ₹2 trillion of annual primary market issuance spanning IPO, FPO (follow-on public offer), preferential allotment, QIP (qualified institutional placements), rights issue, and even OFS (offer for sale)," Narayan pointed out.

“Prolonged mismatch of this nature can leave us with more of asset price inflation, rather than capital formation. Anecdotally, the price of over 30% of mid-cap and small stocks have more than tripled over the last three years," he added.

In other words, Economics 101. If the demand for any product is 100 units, but the supply is just 55 units, then the supply constraint will automatically translate into higher prices of the product. Not just that, the suppliers’ rush to meet the market demand inevitably leads to compromises on the quality front.

“The fear is that with the euphoria around this space, and the hunt for immediate alpha and the liquidity, the likelihood of these being bubbles cannot be ruled out. Startup investing is difficult even for seasoned investors that look beyond pure financials and at the idea, the promoters, the work ethic, the team, the plan. None of these are being tested or discussed at the IPO level and the risk is infinitely higher," Grant Thornton Bharat’s Agarwal added.

But there’s another factor that’s commonly overlooked by equity investors, especially in the IPO segment. And this often leads to some disastrous decision making.

Signal vs Noise

Here’s another lesson from Economics 101—when price goes up, demand for a good reduces. However, the opposite is true in the stock market. When the price of a stock goes up, demand rises too, especially during a bull market.

")

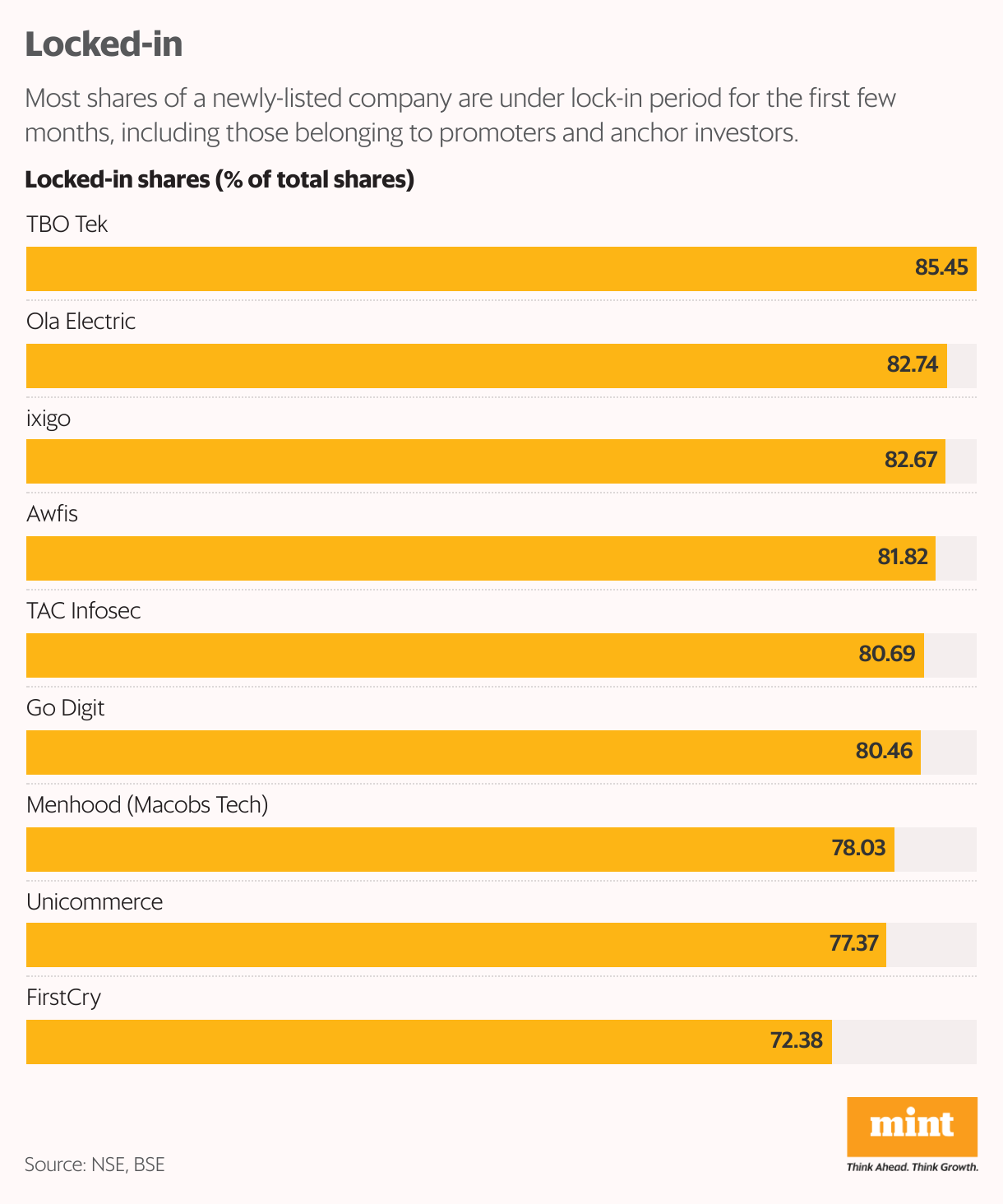

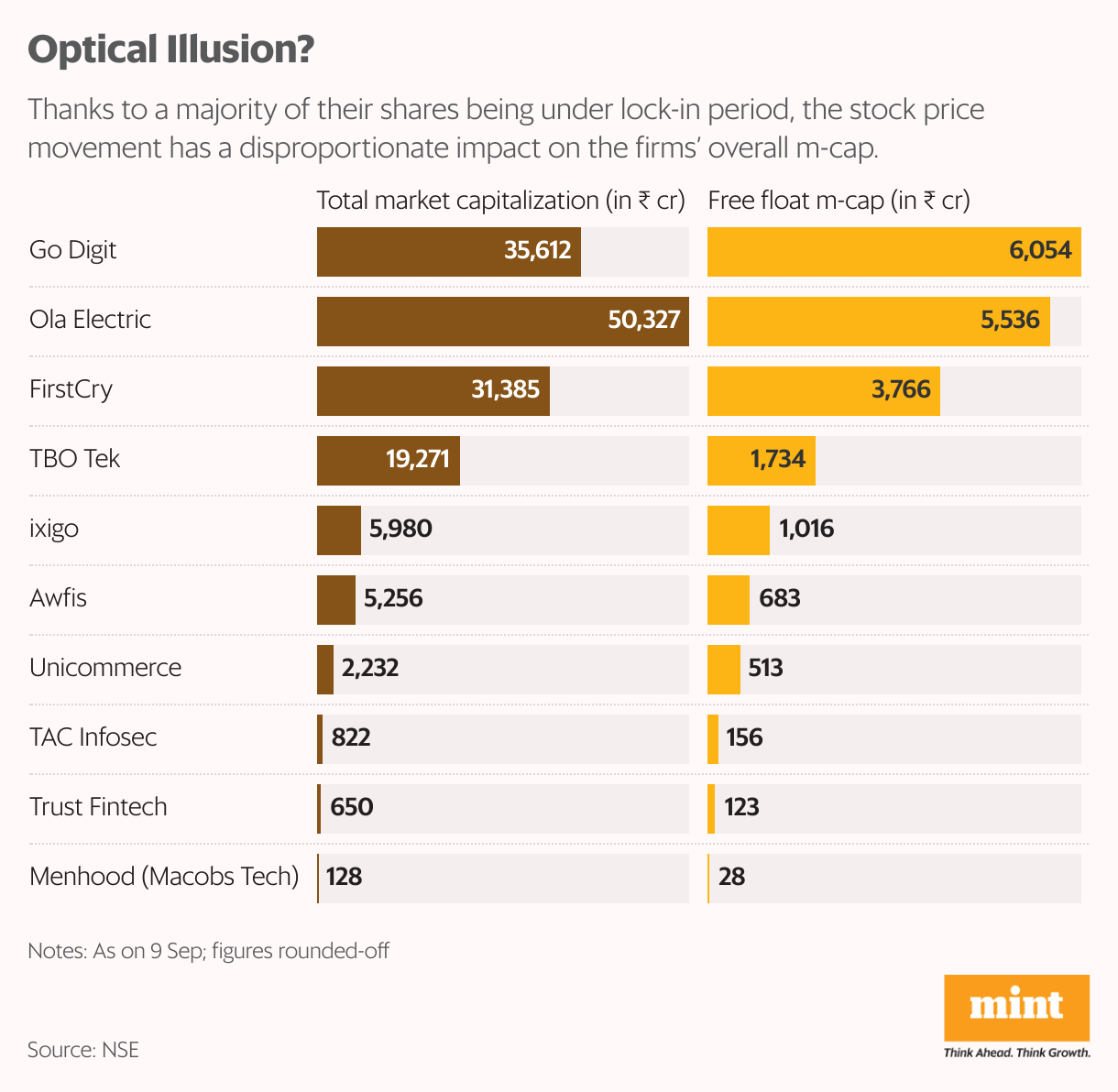

A daily supply of rah-rah headlines on IPO performance can tempt people into thinking that all these stocks will become multi baggers, but inexperienced investors rushing to grab a piece of the action often gloss over a fundamental fact—most shares are under a lock-in period during the first few months.

According to the regulations, for company promoters, 20% of the post-issue paid-up capital must be locked in for 18 months, while any allotment exceeding this 20% threshold is subject to a lock-in period of six months.

For anchor investors, 50% of the allotted shares is locked in for 30 days from the date of allotment, with the remaining 50% locked in for 90 days. The lock-in period for non-promoters ends after six months.

Look at Ola Electric, for example. Nearly 83% of its shares are under the lock-in period at the moment. For Brainbees Solutions (the parent company of FirstCry), the corresponding figure is 72.38%, while that of Awfis is 81.82%. And so on.

For companies with such a low free float (i.e. shares available for trading), even modest inflows can lead to stock prices moving up very quickly.

Which means investors must take a more nuanced view when interpreting the price signals. Just because a startup (with only around 15% free float shares) is seeing a surge in its stock price, it doesn’t mean it will turn out to be the “next Amazon" or the “next Tesla".

Even the most promising startup will have to beat incredible odds to emerge as a market leader. And this process will likely take many years, if not decades.

From an equity market perspective, the true test of such companies is when the lock-in shares are released in the market. This is where most domestic startups seem to be floundering.

The report card of the startups listed over the past two years makes for a sobering read.

Out of the five startups listed in 2023, two are deep in red (ideaForge down 46%, Yudiz Solutions down 65%), one is barely in the green (Yatra Online up 3%) while only two have delivered respectable returns (Zaggle Prepaid up 124%, Honasa Consumer up 65%).

Even for the last two companies, stock prices have stagnated after around six months, coinciding with the release of lock-in shares.

Out of the three startups listed in 2022, Delhivery is down 25%, Tracxn Technologies has inched up 2% and DroneAcharya has delivered a modest 12% returns.

Games People Play

One of the most fascinating features of a bull market is that every stock seems to be “the next best thing". As an investor, it can be hard to avoid the fear of missing out (FOMO). But an over-heated environment is precisely the time you should have your ‘bullshit antennae’ on high alert.

IPO oversubscription of 100 times or 200 times should not be taken as a ringing endorsement of the company’s fundamentals. This is because not everyone is playing the same game in the market.

You might be looking to build a medium to long-term portfolio of quality companies, but a horde of excitable investors may just be itching for listing day gains. In fact, this is exactly what is happening right now.

According to a Sebi study released last week, about 54% of IPO shares (in value terms) allotted to investors (excluding anchor investors) were sold within a week from listing. Individual investors sold 50% of the shares allotted to them by value within a week of listing, and 70% of shares by value within a year.

Casinos might be banned, but casino culture is harder to eradicate.

But all this does not mean you should avoid startup IPOs altogether. Far from it.

“While one cannot discount that markets are sentiment driven in the short term, in the long term, fundamentals will win. Of course, growth of markets will not be without corrections," Aakash Agrawal, associate director, digital and new-age business at Anand Rathi Investment Banking, told Mint.

“Technology companies that have gone public in the recent past are no longer startups. They are large companies which in some cases house many businesses, some profitable and mature, others in investment mode. Trailblazers like Zomato that were loss making at IPO have churned quarter after quarter of growing profits while not compromising on growth. Another healthy sign is inorganic growth from the acquisition of companies like Blinkit and now potentially Insider (from Paytm)," he said.

The Street has rewarded such performance and technology-driven rapid growth potential. Technology companies with robust underlying fundamentals can be cash flow generating machines if led by strong leadership teams, Agrawal added.

India’s digital economy too presents a huge opportunity.

“Today, digital contribution (excluding IT services) to India’s GDP of $3.4 trillion is approximately $150 billion, which is about 5%. In contrast, China’s digital contribution to GDP is 40% of an $18 trillion economy, while the US is even larger at 60% of a $27 trillion economy! In another 10 years, or by 2035, India’s GDP could well exceed $10 trillion and it would not be entirely unreasonable to expect a 20% contribution from the digital economy. There is a very real opportunity for technology-led companies to create almost $2 trillion of value over the coming decade," he added.

That said, investors would need to filter companies based on their fundamentals, growth potential and management quality. Ignoring these basics can mean creating a chakravyuh for your financial future. And as history shows, that is a war very few can win.

- After a lull in 2023 and 2022, startup IPOs are back with a bang this year.

- New age companies want to take advantage of the raging bull market.

- Startup shares have maintained their momentum post listing as well.

- But startup investing is difficult. The euphoria around this space can prevent investors from spotting bubbles.

- Investors must take a more nuanced view when interpreting the price signals.

- IPO oversubscription of 100 times or 200 times should not be taken as a ringing endorsement of the company’s fundamentals.

- The true test is when the lock-in shares are released in the market—this is where many startups seem to be floundering.

- Investors need to filter companies based on their fundamentals, growth potential and management quality.