Markets

Markets

Why Angel One needs to look beyond the broking business

")

Summary

- Angel One's peers are either trying to make money through client funding facility or using the client base to earn from cross-selling opportunities such as wealth management products

Angel One Ltd's mainstay is its broking business, accounting for almost 70% of its total revenue. But is that enough?

Angel One's pretax profit growth of 27% in the March quarter to ₹459 crore was muted as compared with its gross broking revenue, which jumped 59% to ₹924 crore.

Even after adjusting for brand-building costs through spending on the Indian Premier League, pretax profit growth would have been 33%.

The growth in broking revenue was mainly driven by a 79% surge in total orders, as there is hardly any scope to increase the brokerage rate with most of the industry moving to a flat fee structure. Revenue per order was down 11% to ₹19.6 in Q4.

In fact, the flat fee structure is being threatened as some brokers like mstock by Mirae, and Shoonya by Finvasia have moved to zero brokerage by charging a small upfront fee in some instances. Kotak Securities has also launched zero brokerage for all intra-day trades.

Most of them are either trying to make money through client funding facility, essentially a lending business, or using the client base to earn from cross-selling opportunities such as wealth management products.

Also Read: Broking community divided on extending hours for equity derivatives trading

The ownership of retail or individual investors in Indian equities has gone up from ₹17 trillion to ₹35 trillion over the three years to December 2023. However, the higher ownership of retailers does not fully translate into higher brokerage for most in the industry including Angel One.

The company derives more than 80% of its gross broking revenue from the F&O market. Though it charges intra-day cash transactions at a maximum of ₹20 per order, it has waived the brokerage on delivery transactions. Most of the trading volumes are now concentrated in options with low value to avoid securities transaction tax in high-value transactions of equities and futures.

Notably, Angel One has also raised ₹1,500 crore from QIP a couple of weeks back to meet its increasing margin funding requirement. The management has clarified that there will not be any savings in interest cost as the funds raised from equity will not be used for repaying the gross debt, which stands at ₹2,535 crore at March-end.

It is more of a growth capital as it is also pursuing ancillary businesses by setting up asset management company, foraying into wealth management, among other things. However, competition across the financial services industry is increasing.

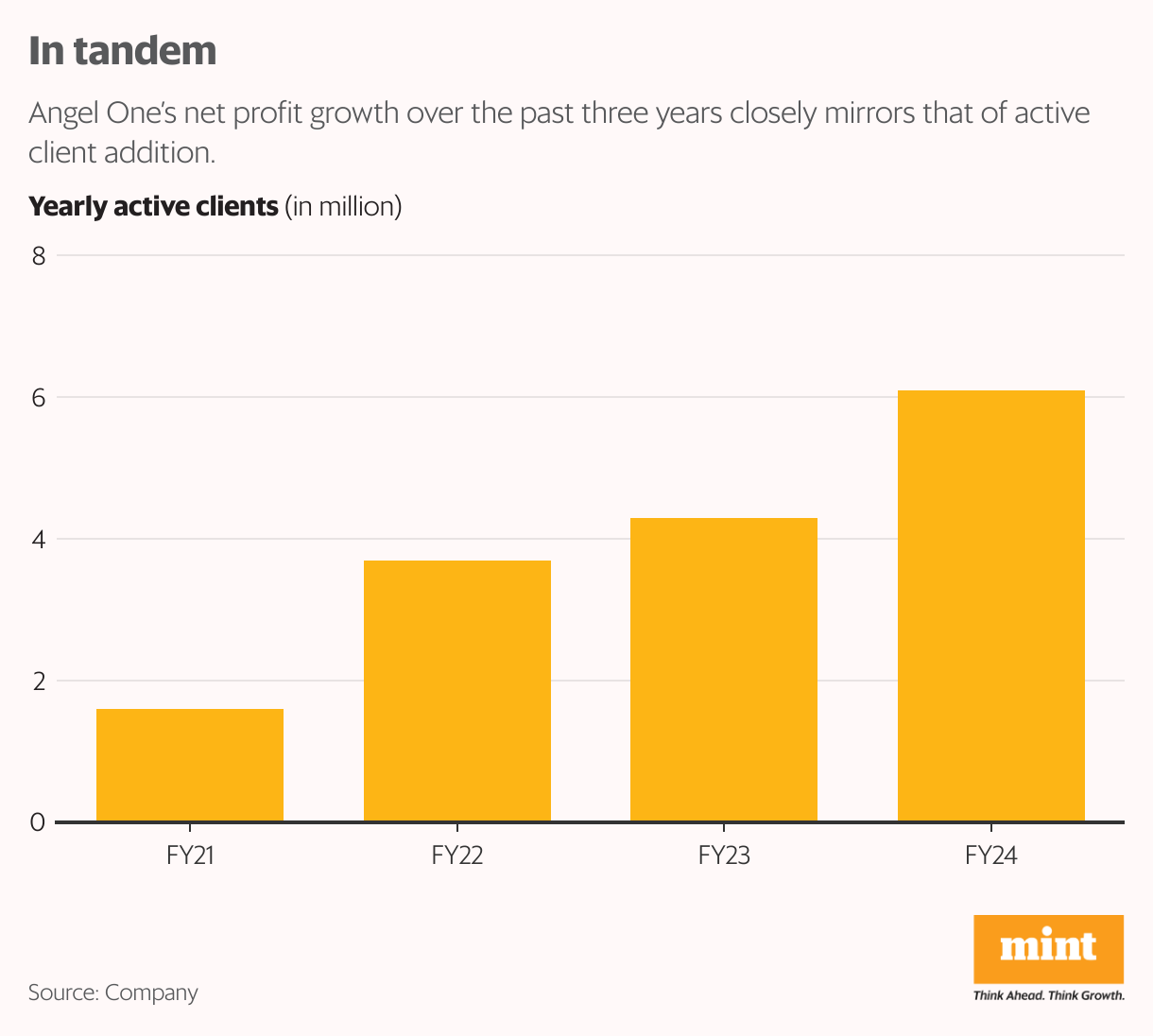

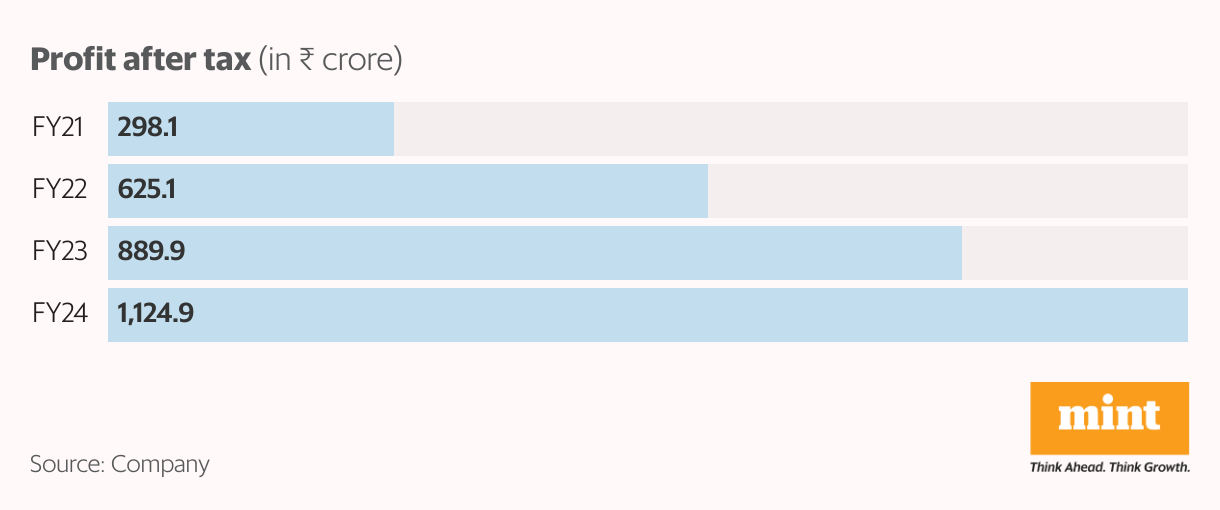

Angel One’s net profit growth over the last three years to FY24 closely mirrors that of active client addition. Both have grown at a nearly similar CAGR of 56%.

The current stock price discounts FY24 earnings by 23 times after considering fully diluted equity base of 8.9 crore shares post the QIP. The future trajectory of the share price will depend more on how the company’s current broking-dependent business model evolves through diversification of revenue stream.