Apollo Hospitals' healthy capacity addition to drive future growth

")

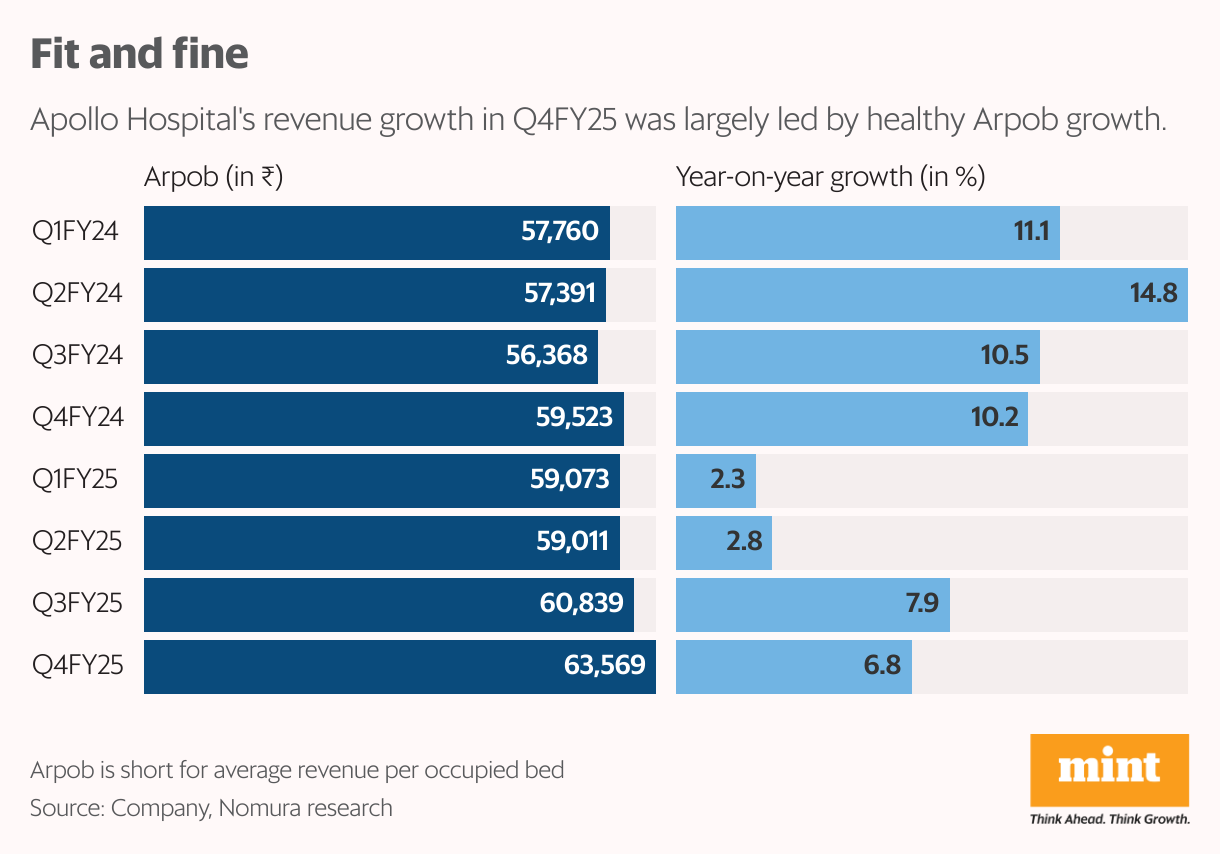

Apollo Hospitals' average revenue per occupied bed (Arpob) increased by 6.8% to ₹63,569 per day. The healthcare division's revenue rose 10% to ₹2,843 crore, driven by Arpob growth. The company plans significant bed additions in the next few years to enhance capacity.

Apollo Hospitals Enterprise Ltd’s average revenue per occupied bed (Arpob) continued its upward trajectory in the March quarter, rising 6.8% from a year ago and 4.5% from the previous quarter to ₹63,569 per day. The highest increase came from the western region.

This metric for the western and eastern regions has consistently languished below the overall Arpob for the past eight quarters at least. This also means that when Apollo manages to lift the Arpob of the two underperforming regions, the overall figure could get a boost.

The other two key variables for Apollo Hospitals are capacity (operating beds) and capacity utilisation (occupancy rates). The number of operating beds grew 1% year-on-year to 8,025 and occupancy rates expanded 200 basis points (bps) to 67%.

Despite the muted growth in occupied beds, the healthcare division’s revenue grew 10% to ₹2,843 crore, with almost 65% of the growth coming from the rise in Arpob.

According to the management, visa restrictions imposed by India on patients from Bangladesh following the political upheaval in that country impacted its hospitals in the eastern region in general and Kolkata in particular. The management said the issue has affected its FY25 revenue growth rate by 150 bps and Ebitda margin by about 50 bps.

Nonetheless, the healthcare division has growth drivers in place. While the addition to operating beds has been less than 5% over the past two years to FY25, a course correction is under way.

Apollo plans to add 4,300 beds over the next 3-4 years, with about 2,000 beds already in progress. The expansion includes increasing beds in existing hospitals and setting up new hospitals.

Also Read | Apollo Hospitals to deepen presence in Bengaluru, Hyderabad

The capital expenditure on adding beds is estimated to be ₹7,400 crore over the next three years. With most of the bed additions in the metro cities, the share of metro beds is expected to rise. Arpob in metro hospitals tends to be higher than in non-metro hospitals.

Healthcare, pharmacy

The healthcare division contributed half of Apollo Hospitals’ revenue in Q4, but its Ebitda of ₹686 crore accounts for almost 75% of the company’s Ebitda as the retail health and pharmacy segments are still struggling to make any meaningful impact. The Ebitda margin of healthcare rose 110 bps year-on-year to 24%.

The management expects to maintain the healthcare Ebitda margin at 24% in FY26 even as there could be initial costs and a gestation period for the stabilisation of new hospitals. The existing hospitals are likely to grow in the low-to-mid-teens and are expected to make up for the loss from new hospitals.

Also Read | Apollo Hospitals to invest ₹6,000 crore to add 3,500 new beds as chronic diseases rise

Beyond healthcare, Apollo Hospitals’ investors would like to see a growth impetus from the pharmacy business, Apollo HealthCo. The business is being restructured to bring the online, offline, retail and wholesale pharmacy segments under one umbrella.

The pharmacy business combined proforma FY25 revenue was ₹16,377 crore. The management expects this to reach ₹25,000 crore by FY27, which would mean a 24% CAGR.

There is likely to be substantial improvement in profitability as well with the Ebitda margin expected to be 7-8% from the current level of 3.2%, aided by a reduction in the loss of digital consultation and treatment business of Apollo 24*7.

Also Read | Apollo Hospitals driving up high complexity care, to continue focus on core metros

Neither the decent results nor the healthy growth outlook led by capacity expansion in the core hospital business moved the stock on Monday. Nomura has a ‘neutral’ rating on the stock with a sum-of-the-parts-based target price of ₹6,856.

The target price implies an EV/Ebitda of 28x based on FY26 estimates of the brokerage. This is a fair value zone, given that most hospital stocks in India have traded at 25x-35x one-year forward EV/Ebitda.