Markets

Markets

As JK Lakshmi Cement pushes the pedal on capex, beware debt pinch

Summary

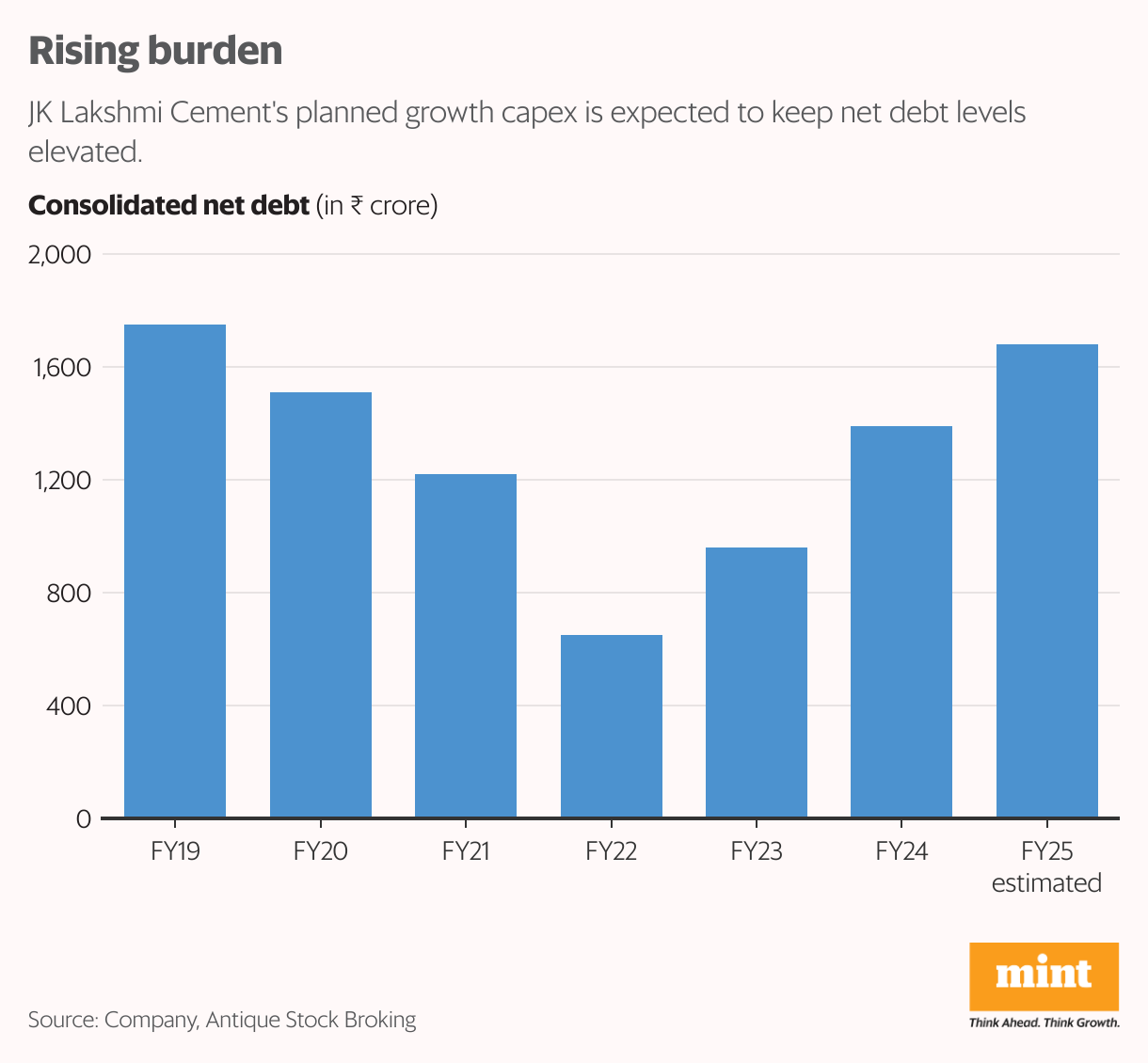

- The company's plans for ₹1,200 crore of capex in FY25, ₹1,000 crore in FY26, and ₹1,200 crore in FY27 could increase its consolidated net debt from ₹1,400 crore in FY24 to more than ₹2,500 crore by FY27, said Antique Stock Broking.

JK Lakshmi Cement Ltd’s March quarter (Q4FY24) results were a mixed bag. Tight cost control led to better-than-anticipated operating performance. On the other hand, capacity constraints meant year-on-year volume growth was flat at 3.3 million tonnes. Realisations dipped on muted cement prices in key markets of north, west and east India.

Nonetheless, JK Lakshmi’s thrust on capital expenditure (capex) continues. It has plans for ₹1,200 crore of capex in FY25, ₹1,000 crore in FY26, and ₹1,200 crore in FY27. The capex guidance for listed subsidiary Udaipur Cement Works Ltd was set at ₹300 crore for FY25. For comparison, the combined capex of JK Lakshmi and Udaipur Cement Works was around ₹1,010 crore in FY24.

Capacity addition plans are on track, said management. The company is expanding its cement-grinding capacity in Surat, Gujarat, from 1.35 million tonnes per annum (mtpa) to 2.7mtpa and expects to complete this by Q4 FY25. It is also expanding clinker capacity at its integrated cement plant at Durg in Chhattisgarh by putting up an additional clinker line of 2.3 mtpa and four cement grinding units aggregating to 4.6 mtpa. The company aims to increase its grinding capacity from 16.4 mtpa to 30 mtpa by 2030.

Also read: As post-covid demand cements itself, this sector is eyeing a shift in gears

The ongoing capacity additions are positive and provide long-term volume growth visibility. But amid elevated competition and a race to gain market share, the company’s target of 10% volume growth in FY25 seems ambitious.

When will demand recover?

East India, where it is adding new capacity, is already seeing surplus supply from other cement manufacturers. So if cement demand fails to recover, prices in this region may take longer to revive, hurting the company’s realisations outlook. Note that cement prices remain subdued across India so far in Q1 FY25 and are expected to improve only in the second half of the fiscal year.

Also read: JSW Infrastructure plans ₹2,500 crore capex for FY25

The repercussions of elevated capex will also be felt in its debt profile. Consolidated gross debt stood ₹2,000 crore in FY24, and is expected to rise due to planned capex, management said. Antique Stock Broking expects the company’s consolidated net debt to increase from ₹1,400 crore in FY24 to over ₹2,500 crore by FY27. Consequently, the net-debt-to-Ebitda ratio could rise from 1.3 times to 1.6 times over this period.

JK Lakshmi’s stock has declined by 12% so far in 2024. It trades at an FY25 EV/Ebitda multiple of around 9x, according to Bloomberg data, a discount to its large-cap peers. Despite its cost-efficiency, the valuation gap is likely to persist unless volumes or realisations improve significantly.