Markets

Markets

Street race for Ashok Leyland after margin spike in last fiscal

Summary

Softer raw material costs and slower growth in staff costs were the chief drivers of profitability.

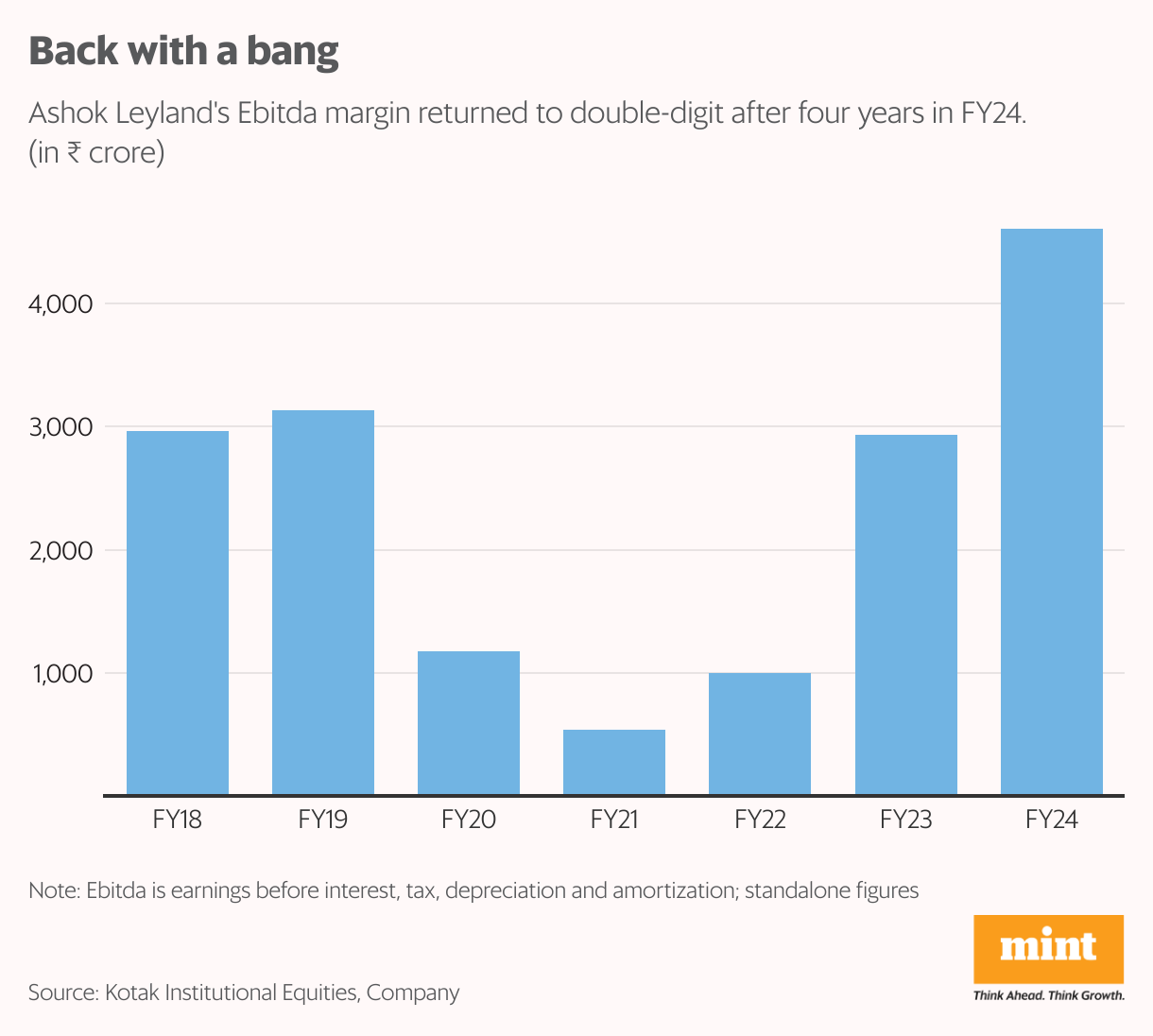

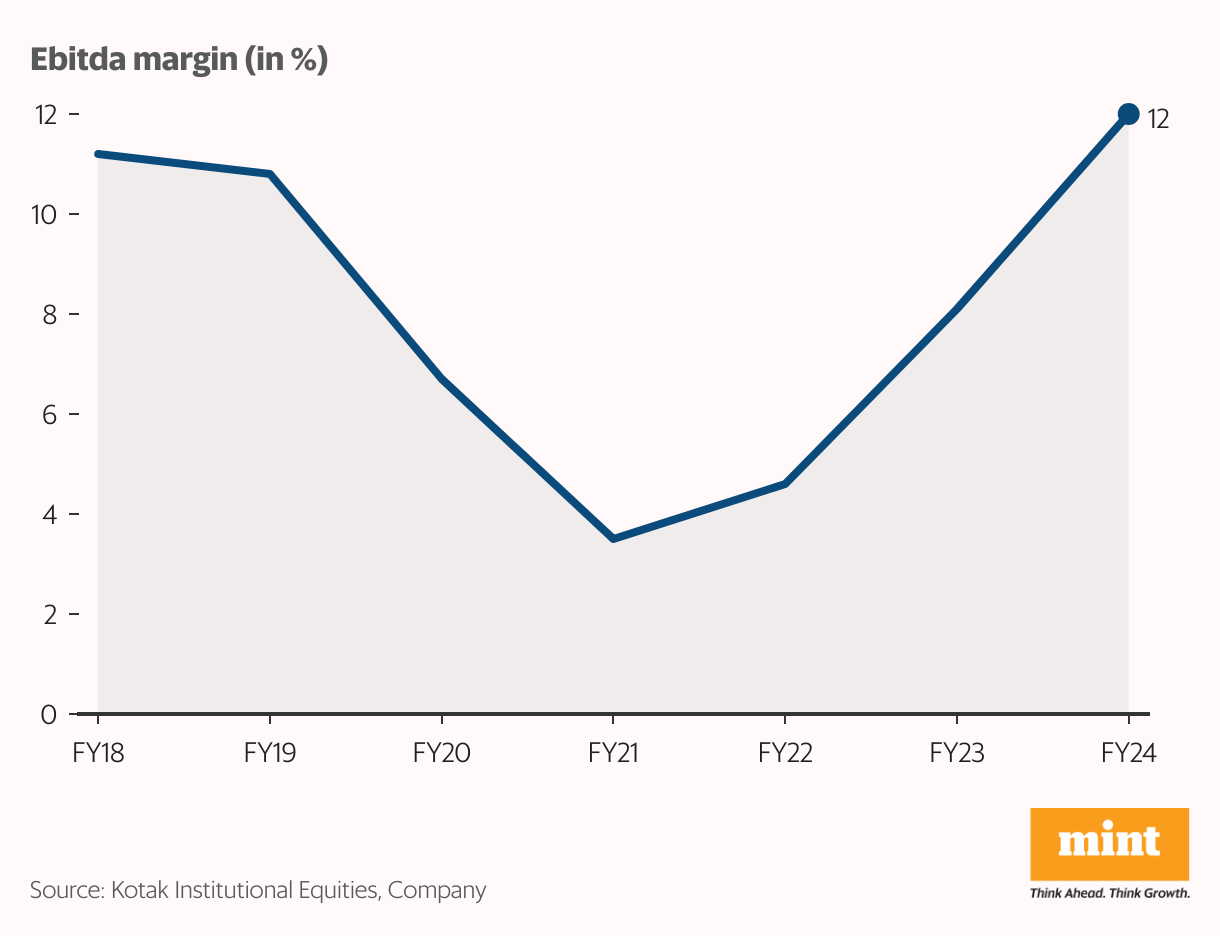

After four years, Ashok Leyland Ltd clocked a double-digit Ebitda margin—a striking feature of the commercial vehicle maker’s results for 2023-24. Standalone margin expanded by as much as 390 basis points (bps) year-on-year to 12%. One basis point is 0.01%.

The last time Ashok Leyland’s margin for the full year was in double digits was in FY19. Ebitda growth in FY24 improved 57% year-on-year to ₹4,607 crore, on a revenue growth of just 6%, which was on a relatively high base. Softer raw material costs and slower growth in staff costs were the chief drivers of profitability.

Similar trends played out in the March quarter, too. Ebitda margin rose 316 bps year-on-year to 14%, surpassing analysts’ estimates. This is better than Tata Motors Ltd’s ebitda margin of 12% in its standalone India commercial vehicles segment.

The upshot: Ashok Leyland’s fourth-quarter ebitda growth came in at nearly 25% despite revenue falling by 3% as volumes dropped 6%. Robust gross margin improvement and better realization lent support to the company's March-quarter earnings.

Also Read: Ashok Leyland margin a show stopper in Q3

On Monday, the shares jumped nearly 7.5%, also scaling a new 52-week high of ₹228.30 apiece; returns for the last one year stand at a cool 56% roughly.

Following the results, some analysts have raised their estimates of Ashok Leyland’s earnings for this year and the next. Over the medium-term, Ashok Leyland’s management is keen that its ebitda margin reach mid-teens, helped by discipline on discounts, pricing actions, and cost control initiatives.

Optimistic future

The company is optimistic on volume prospects in FY25, and believes that fears of an election-related slowdown have not played out.

In the light commercial vehicle (LCV) segment, Ashok Leyland has planned a slew of launches for the coming quarters, and intends to expand the LCV addressable market to 70-80% from the current 50%.

Further, the company expects the defence segment to be a promising area of growth. Its capital expenditure for FY25 is pegged at ₹500-700 crore, versus ₹500 crore in FY24. Ashok Leyland has also guided for investments towards its electric vehicle subsidiary, Switch.

Also Read: Rough road ahead for Ashok Leyland

Some analysts are cautious, though. “We are building in flat volumes for domestic M&HCV goods industry in FY25E, before a 10% dip in FY26E, thus, factoring in Ashok Leyland’s M&HCV volume CAGR at -6% over FY24-26E, assuming steady market share," ICICI Securities said in a report.

Thus, how demand plays out will be crucial for the Ashok Leyland stock. For now, investors seem to have factored the positives adequately, evidenced by the stock’s returns. A sturdy margin show ahead may support the stock.