Markets

Markets

Bank of Baroda’s balance sheet expands, but can investor interest pick up?

Summary

Despite a 14% growth in bulk deposits, retail deposits lagged at 9.7%. The upcoming FY25 results will reveal if advances translate to improved fee income.Bank of Baroda’s business update for FY25 on balance sheet parameters largely epitomises the problems faced by the banking sector in terms of domestic deposit mobilisation even as growth of domestic advances remains strong.

Sure, the overall loan-deposit ratio (LDR) for FY25 was comfortable at 82% for the second-largest public sector bank in India by market capitalisation. Still, lower deposit mobilisation meant that incremental LDR for the year was elevated at 117%.

The update is broadly in line with the management’s guidance for FY25, estimating loan growth at 11-13% and deposit growth at 9-11%. Domestic advances grew by 13.7% year-on-year to ₹10.2 trillion, led by a robust 19.4% growth in retail advances.

Also Read | Loan growth slows for banks in Q4 as liquidity stays tight, deposits lag

It will be interesting to see the composition of the 9.3% year-on-year growth in domestic deposits to ₹12.4 trillion when the results are announced. Going by past trends, overall deposit growth is likely to be driven by term deposits.

Cost of deposits

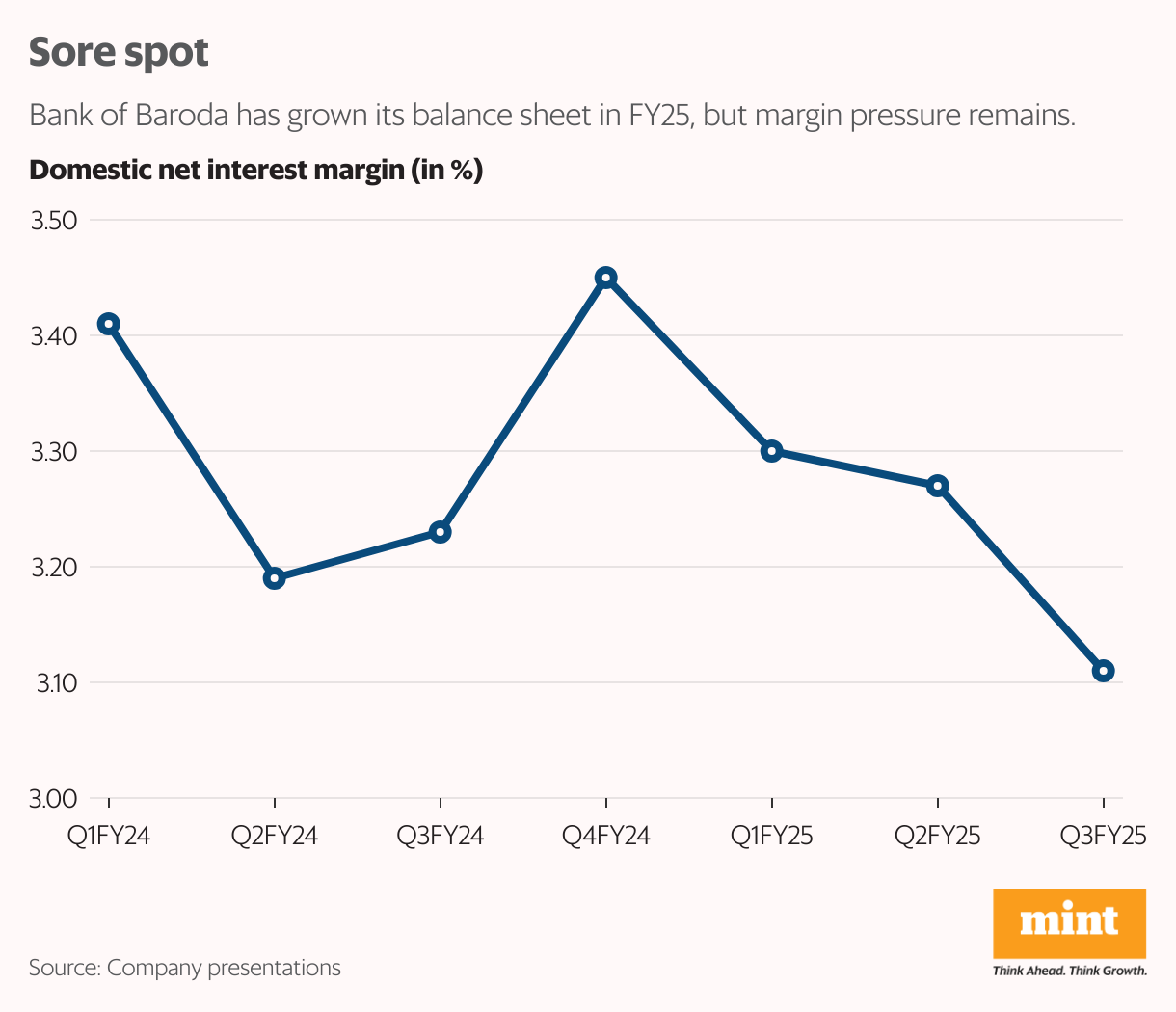

During the first nine months of FY25, CASA (current and savings accounts) deposit growth rate at 6.5% was below the term deposit growth rate of 11.1%. Thus, the cost of deposits has shown a linear trend as it inched up to 5.2% in Q3 from 5.1% in Q1 of FY25.

During this period, the yield on advances has shown a linear compression to 8.87% from 8.99%. Consequently, the net interest margin narrowed to 3.11% from 3.3%.

The bank’s management has stated that it aims to focus more on CASA deposits and relatively stable retail term deposits instead of bulk/wholesale deposits that are volatile in nature. The bank’s growth rate in bulk deposits at 14% had outpaced the growth rate of retail deposits at 9.7% in the first nine months.

Idle funds

Competition for CASA deposits has intensified, with most banks offering automatic transfer of excess funds from savings accounts to fixed deposit accounts, effectively reducing the idle funds in savings accounts.

Also Read | Why RBI gave banks a knuckle rap for their misaligned retail focus

Notwithstanding Bank of Baroda’s good growth in advances and deposits, it remains to be seen whether that translates into any improvement in fee-based income. Fee income had marginally declined by 1% year-on-year in the first nine months even when total business (loans plus deposits) rose. This will be worth tracking when the FY25 results are declared.

The bank’s valuation continues to be undemanding at just about 0.8x of book value for FY26, based on Bloomberg consensus estimates. Still, investor interest may not pick up as the earnings growth forecast for FY26 is almost flat.