Bata India continues to drag its feet on growth; trail remains rough

- Bata's problem is that revenue growth refuses to pick up. June quarter marks the fifth consecutive quarter of subdued performance. Will a steady network rollout and product revamp push growth?

Bata India Ltd’s shares have lost more than 6% since the company's June quarter results (Q1FY25). It’s not as if the stock was having a super run before it. In the past year, it has fallen 14% versus the Nifty 50’s 25% gain.

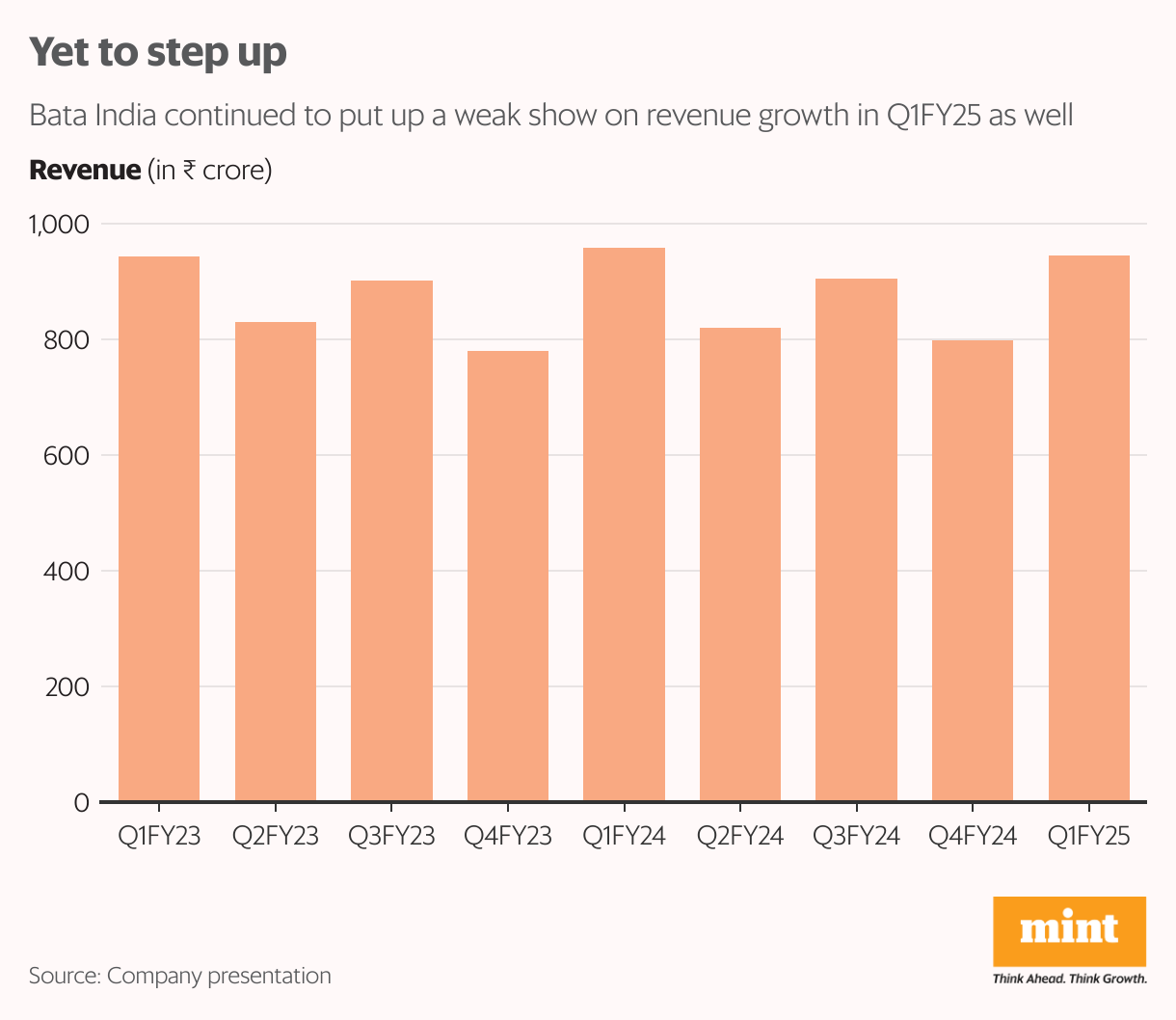

The footwear maker’s problem is the same: revenue growth refuses to pick up. Q1 consolidated revenue decreased by 1.4% year-on-year to nearly ₹945 crore. June quarter marks the fifth consecutive quarter of subdued revenue performance with growth being flattish in FY24 after two years of strong show.

In the March quarter earnings call, Bata’s management had said it was seeing initial signs of demand recovery. While that did continue for some time in Q1, the latter part of the quarter was adversely impacted by factors such as heatwave and election. Gross margin was up 11 basis points to 54.9%, although Ebitda margin contracted sharply, mainly due to one-time expenditure towards technology investments and higher marketing cost.

Encouragingly, some brands are doing relatively better for Bata. For instance, Floatz contributed about 5% to retail sales last quarter. Bata has 16 Floatz kiosks and plans to reach 30 by December. Further, the Power brand is seeing double-digit growth momentum and the company intends to launch two big products this quarter.

In Q1, Bata launched its second Power EBO (exclusive brand outlet) in the North and aims to reach 15 EBOs by December. In Power Apparel, the company is seeing quarter-on-quarter sales improvement and intends to touch 100 stores by December from 70 now.

These efforts should push growth. “A steady network rollout and a product revamp (including apparel and sneakers) could support growth going ahead," said a report by Motilal Oswal Financial Services. It also points out that persistent softness, particularly in the mass segment (below ₹1,000 average selling price), remains a drag.

Overall, Bata added 33 franchise stores in Q1 (taking the total count to 566), primarily in tier 3, 4 and 5 towns to cater to branded products' demand and achieve better returns on capital. Further, it added 21 company owned, company operated (COCO) stores, taking the total count to 1,350.

Also Read: Metro Brands is treading on soft demand track after dull Q4

“Given lower than expected Q1FY25 performance, we trimmed our FY25/FY26 estimated earnings by 0.5%/4.0% and changed rating to ‘reduce’ with a revised target price of ₹1,380," said Centrum Broking analysts in a report.

Bata India’s shares now trade at nearly ₹1,419. The stock trades at about 43 times FY26 estimated earnings, showed Bloomberg data. This does not offer much comfort in the backdrop of dull demand recovery prospects.