Markets

Markets

Bharat Forge: Can narrative overshadow the joker in the pack?

")

Summary

- Bharat Forge needs to achieve 15% consolidated sales growth in FY25 to meet Bloomberg consensus estimates

- However, the consensus consolidated Ebitda estimate factors in a margin expansion of 200 bps. To achieve that, the subsidiaries must clock an Ebitda margin of almost 6% from 1% in FY24

Bharat Forge Ltd shares have doubled over the past one year, beating the Nifty Auto index’s 70% returns. The product portfolio of India's largest exporter of auto components is immune to technological changes - a factor that could have aided the stock’s outperformance. Whether vehicles use traditional fuels, lithium-ion batteries or hydrogen, they all need forged metal.

The company has diversified its forging business by adding aluminium forging even as steel is still dominant.

The domestic auto sector has been buoyant in recent years. However, Bharat Forge can weather adversities in the local market because exports contribute 70% of total auto sales. Even if there is a slowdown in the auto industry worldwide, its performance is still cushioned as non-auto sales - mainly consisting of industrials - form about 47% of total sales.

Also Read: Chart Beat: For Bharat Forge, non-auto segments to keep the ball rolling

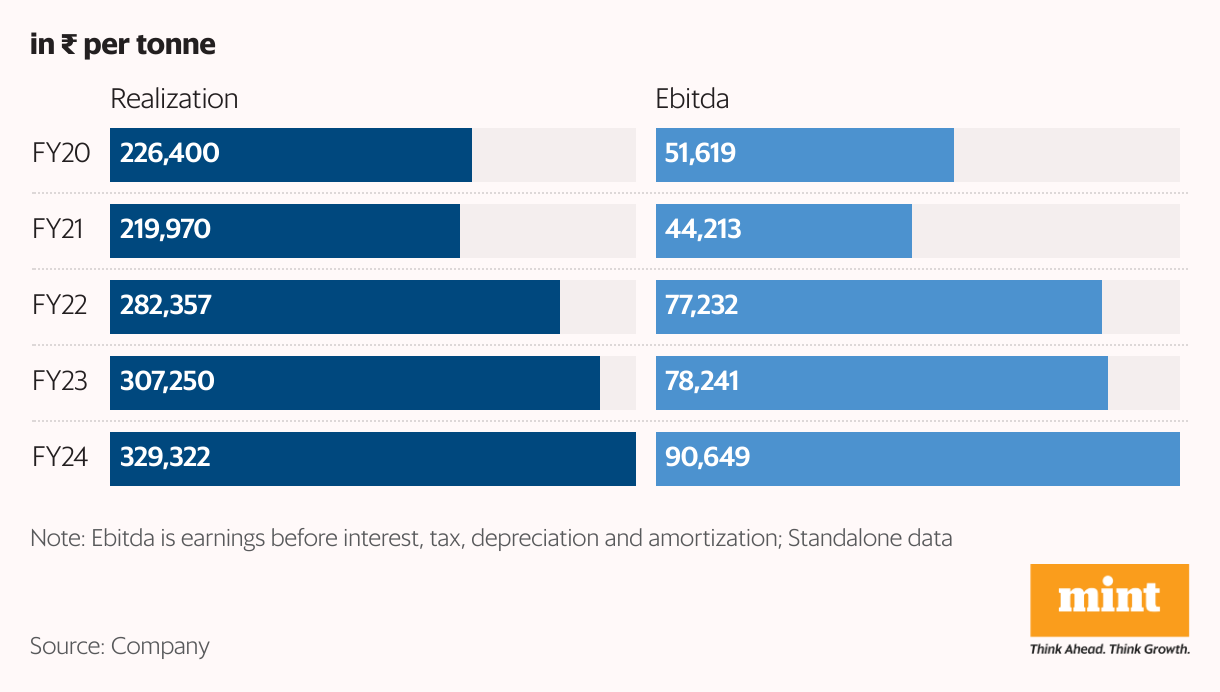

So far, so good, although this strong narrative ends here. While Bharat Forge’s consolidated FY24 Ebitda margin expanded 250 basis points (bps) year-on-year to 16.3%, this needs to be analysed closely by bifurcating the numbers into standalone and subsidiaries.

The standalone business continues to chug along with 20% CAGR in sales and Ebitda during FY22 to FY24. But the subsidiaries have been erratic with 26% CAGR in revenue growth, and Ebitda at ₹268 crore in FY22, then turning negative in FY23 at ₹147 crore, before just about breaking even in FY24. The overseas subsidiaries have posted net losses in the past two years.

Bharat Forge’s management expects subsidiaries in Europe and the US to be profitable in FY25, but it has not given an indicative margin range.

Defence orders

There could be another factor responsible for the excitement about the stock. That is the transfer of the defence business to Kalyani Strategic Systems Ltd, a wholly owned subsidiary. While the management has not officially commented on this, investors seem to be busy discounting the potential value unlocking.

Bharat Forge’s defence order book was ₹5,200 crore in FY24, with almost 80% from the global markets. The company expects global defence spending to increase, which should help in ramping up the business. Additionally, potential orders for ATAGS (Automated Towered Artillery Guns System) in India could boost domestic order inflow.

Also Read: Gunning for growth: Inside Bharat Forge’s defence bets

Based on the market capitalisation (mcap) to annual sales ratio for FY24 of more than 10 times for companies like Hindustan Aeronautics Ltd and Bharat Electronics Ltd, the defence subsidiary of Bharat Forge could get a valuation of about ₹10,000 crore even if 50% discount is assumed for lower scale and Ebitda margin. This translates into a valuation of ₹200 per share of Bharat Forge. The stock currently trades at ₹1,690 apiece.

In FY25, Bharat Forge needs to achieve 15% consolidated sales growth to meet Bloomberg consensus estimates. However, the consensus consolidated Ebitda estimate factors in a margin expansion of 200 bps.

To accomplish that, the company’s subsidiaries have to clock an Ebitda margin of almost 6% from 1% in FY24, assuming standalone operations maintain their margin year-on-year. But can such a big improvement be achieved with operating leverage?Essentially, this remains the joker in the pack for Bharat Forge.

The problem is that even after deducting the valuation of the defence subsidiary, the expansion in valuation multiple seems to have factored in most of the positives. The stock trades at 43 times the Bloomberg consensus EPS estimate for FY25, even adjusted for the euphoria about the separation of defence business.