Markets

Markets

Can BHEL reclaim its crown?

Summary

- Despite a 5% drop in BHEL stock due to disappointing FY24 results, there seems potential for growth largely because of the outstanding order book that stands at ₹1.3 trillion.

- But long-term challenges remain due to a shift towards renewable energy and competition in thermal power.

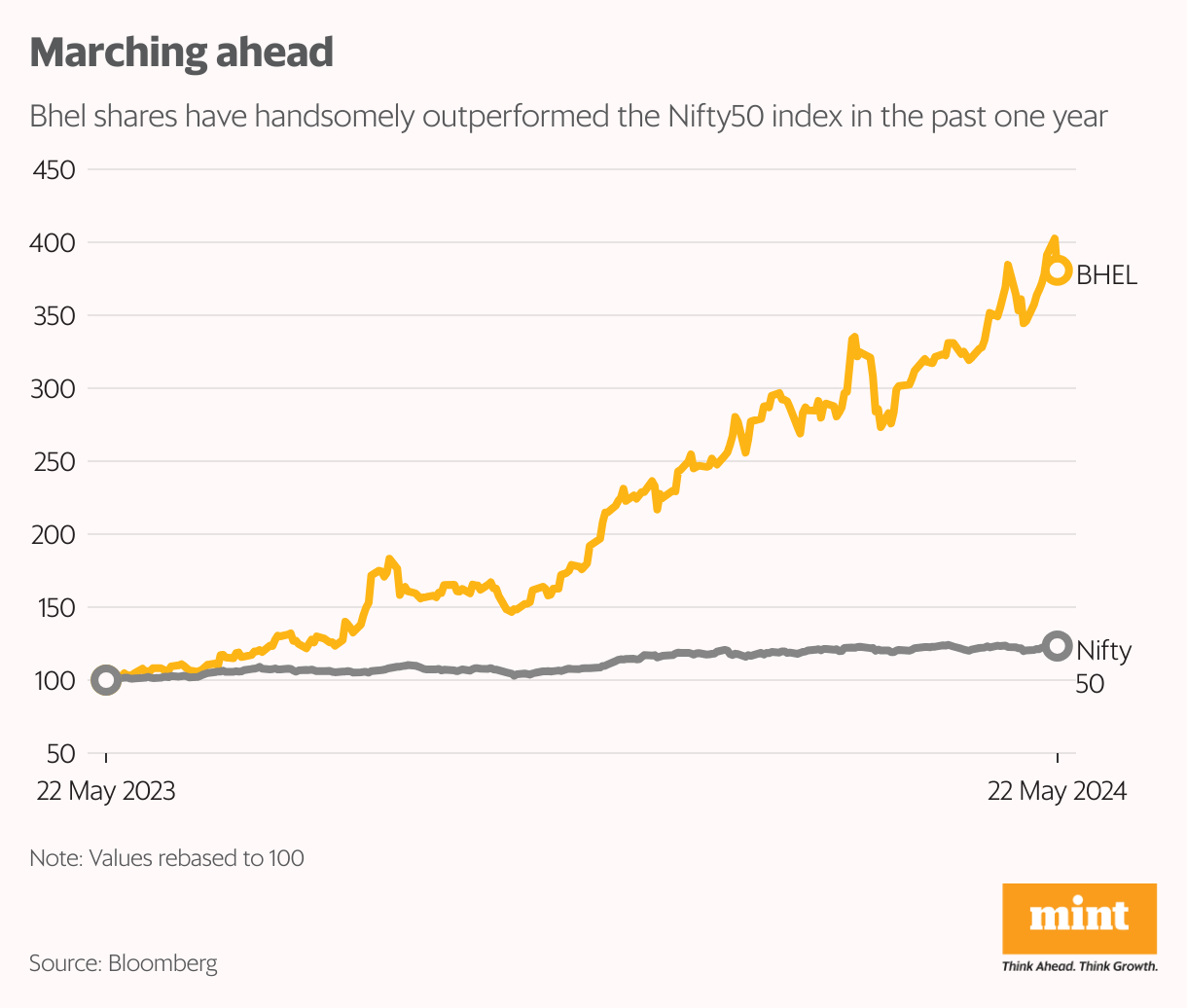

Bharat Heavy Electricals Ltd’s (BHEL) shares have largely moved in line with its swelling order book over the past year. However, disappointing results for the fiscal year ended March 2024 saw the stock lose 5% of its value on Wednesday.

FY24 Ebitda (earnings before interest, taxes, depreciation, and amortization) fell by 36% year-on-year to ₹613 crore, thanks to the doubling of other expenses. Additionally, the balance sheet worsened with borrowings rising by 64% to ₹8,808 crore. More debt was taken to finance working capital as receivables went up and payables declined, which meant that finance cost jumped up by 40%, causing pre-tax earnings to drop by a sharp 68% to ₹220 crore.

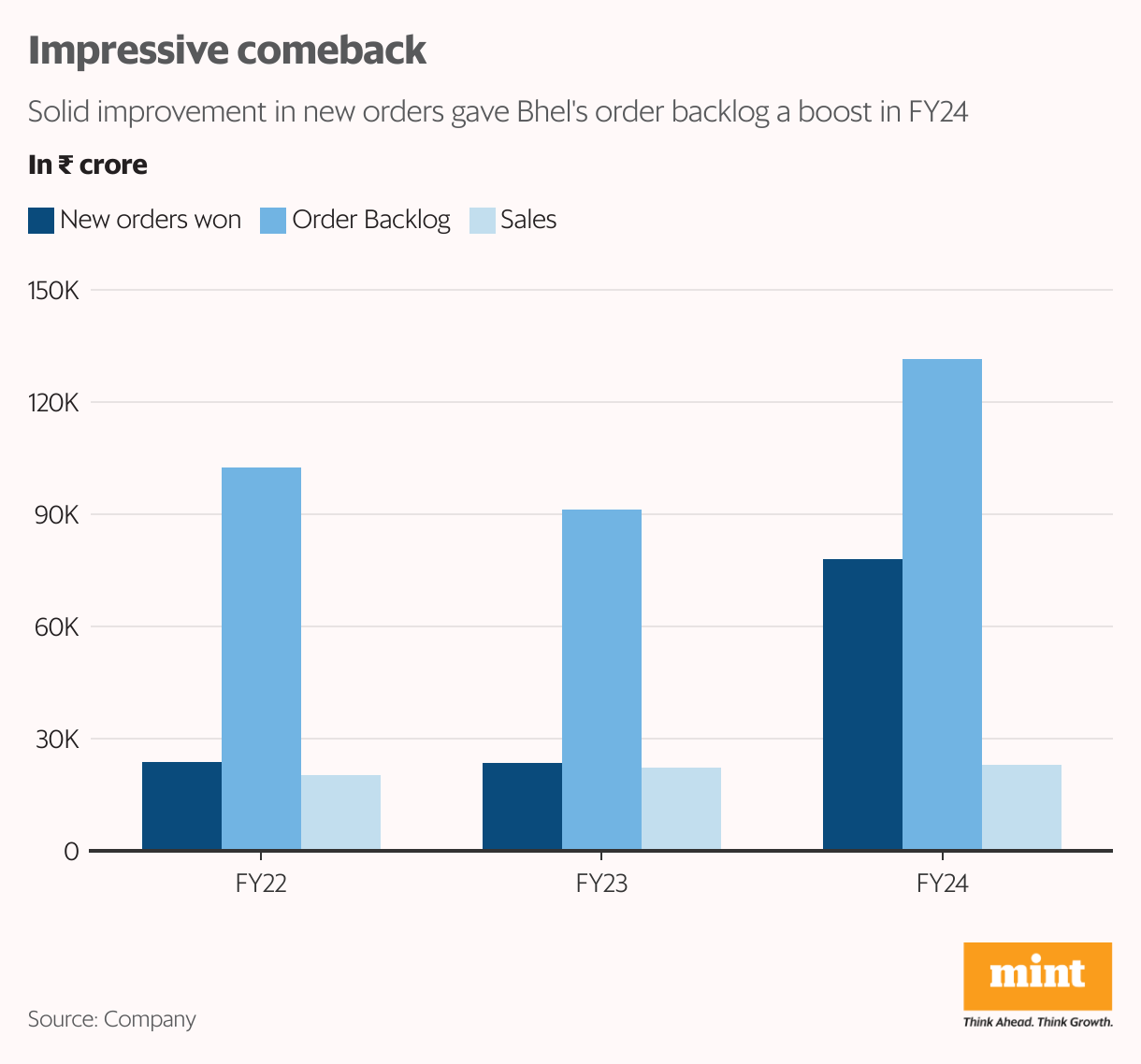

Though earnings appear modest, investors may be anticipating a better outlook. This optimism is due to the outstanding order book expanding to ₹1.3 trillion, a 44% increase, attributed to the highest ever yearly order booking of ₹77,907 crore, nearly 3x the previous year.

Read This: BHEL is on right track, but a slow one

In recent years, the bill-to-book ratio has been about 25%, meaning annual turnover is about one-fourth of the outstanding order book of the previous year, reflecting a typical execution cycle of four years.

Applying this criterion, the best-case scenario for BHEL is a topline of ₹33,000 crore for FY25. With a gross margin of 30% and other costs at FY24 levels, this should translate into an Ebitda of ₹3,400 crore, nearly 5x the FY24 Ebitda due to operating leverage. However, the current market capitalization is already 30x the potential Ebitda.

Note that BHEL’s financial performance peaked in FY13 when it reported an operating income of around ₹50,000 crore with gross and Ebitda margins at about 40% and 20%, respectively. The revival in thermal power capacity addition is unlikely be enough to return to the glory days of peak performance.

Plus, the revival may not be for a sustained period as there is a visible shift towards renewable energy. At the same time, the defence and railway orders, though good for headline news, may not provide any significant boost to the annual numbers because of the long execution lifecycle of the orders.

The company’s share in the Vande Bharat order stands at ₹13,500 crore, won in consortium with Titagarh Wagons for supplying 80 trainsets and servicing them for 35 years. BHEL is also set to supply 20 super rapid naval guns worth ₹3,800 crore to the Indian Navy.

And This: BHEL could be headed for a big turnaround if it can resolve its receivables

Despite diversification attempts over the years, BHEL’s core strength remains its expertise in setting up thermal power plants. This edge does not deserve high valuation multiples that other capital goods companies such as ABB and Siemens are enjoying because they have technological capabilities in sectors beyond power. For instance, ABB is also known for its robotics and Siemens for its medical devices.

Even if the demand for setting up thermal power plants remains intact, the technology is not so complex to prevent the entry of new players as was seen in the past when Larsen & Toubro,JSW EnergyandThermax had all invested heavily in power equipment manufacturing.

While it is difficult to predict numbers in companies like BHEL as they follow percentage of completion method of accounting, the management expects revenue CAGR of 12%-15% for the next few years. It will be mainly due to the revenue recognition beginning from new projects in Bhopal, Jhansi and Bengaluru.

But beyond that, the revenue visibility is bleak as orders for thermal power capacity are likely to dry out. Hence, investors need to look at the terminal value for BHEL rather than getting excited about the current surge in the order inflow of thermal power capacity.