Markets

Markets

Boiling oil menaces macro math, market outlook

")

Summary

- While oil is trading close to $90 currently, the spectre of prices breaching $100 is haunting policymakers.

Three things are certain in life—death, taxes, and West Asia erupting into conflict at regular intervals. The latest string of alarming headlines comes after Iran launched drones and missiles towards Israel, retaliating against a deadly strike on its consulate in Syria, and ratcheting up tensions in a region already grappling with the grisly Gaza conflict.

The US and other G-7 countries have rushed in to cool tempers, but if history is any indication, Israel and self-restraint can rarely be used in the same sentence.

Untangling the complex web of internecine feuds in this perennial tinderbox might frankly be a cognitive dead-end, but global markets have a more pressing, and unabashedly selfish, concern: crude oil prices.

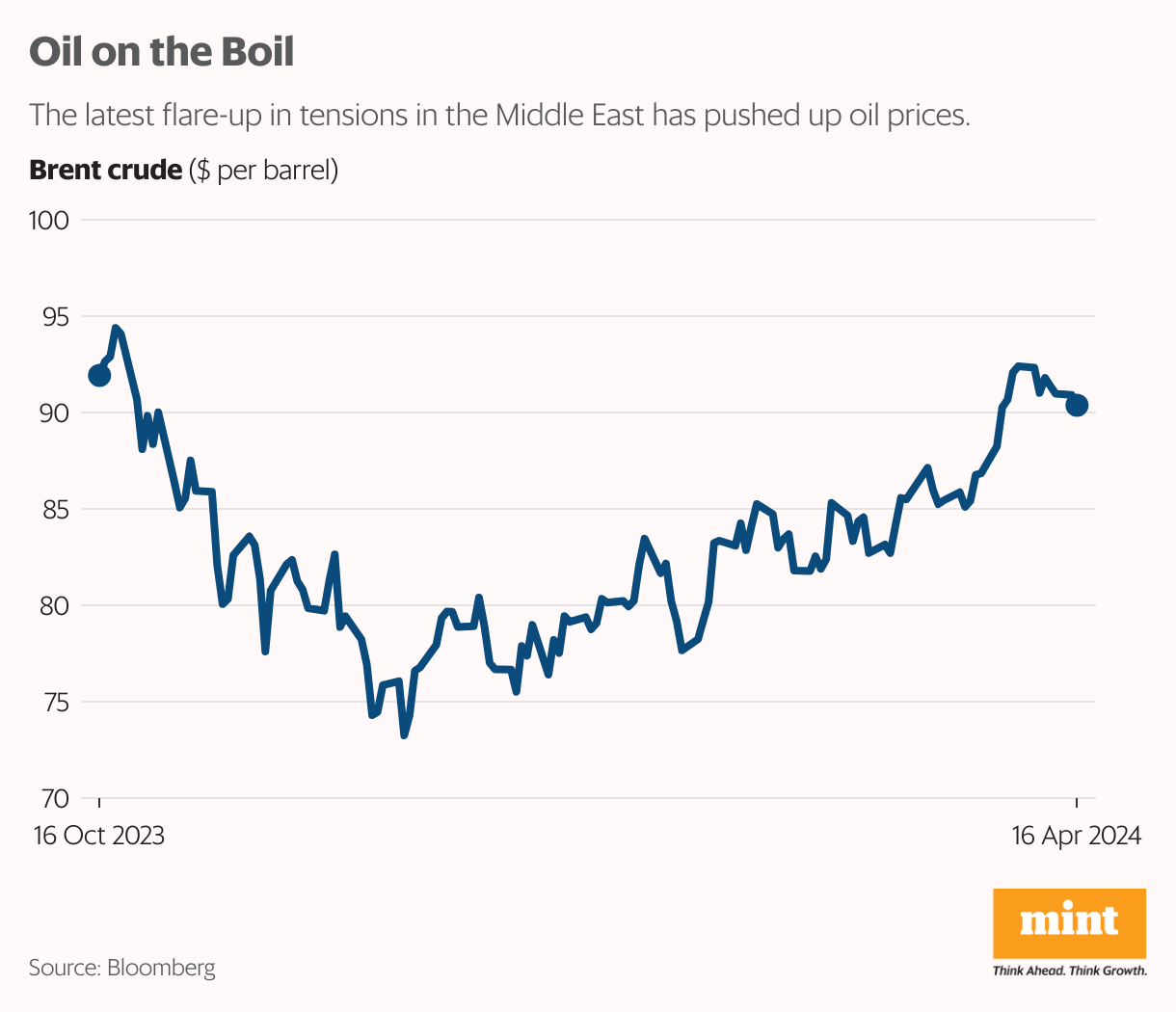

Global oil benchmark Brent crude darted up to near six-month highs of $92 per barrel last week, in anticipation of Tehran’s belligerence.

While oil is trading close to $90 currently, the spectre of prices breaching $100 is haunting policymakers.

For India, oil prices touching the three-figure-mark bodes ill. The country is the world’s third largest oil consumer and importer, after China and the US. India meets over 85% of its oil requirement through imports, making it particularly vulnerable to global price shocks.

Also Read: Will a West Asia conflict ruin the interim budget math?

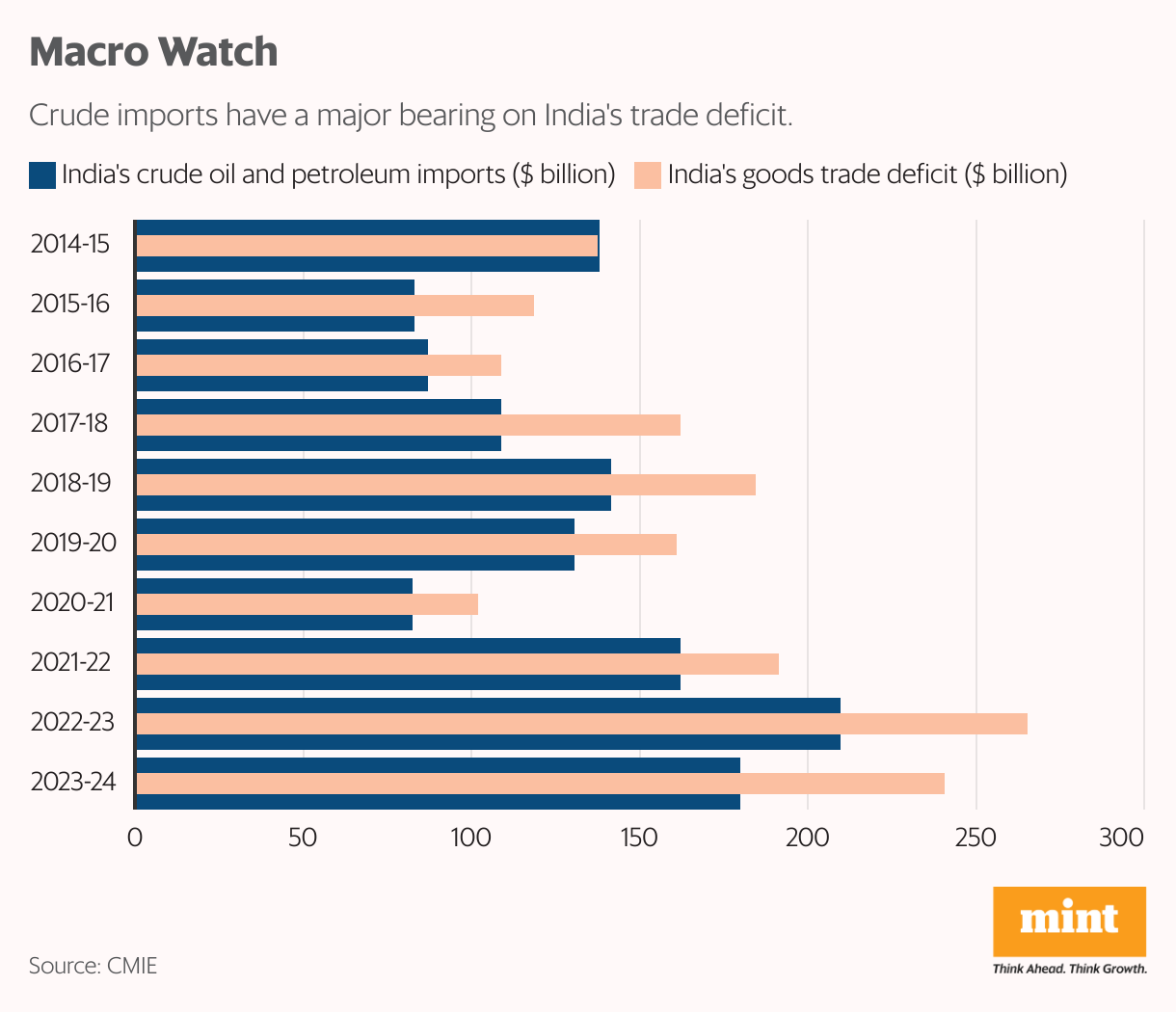

India’s crude oil imports in the first 11 months of FY24 rose 0.4% year-on-year to 212.6 million tonnes, as per latest data.

In 2015, the Centre had set a target to reduce reliance on oil imports to 67% by 2022 from 77% in FY14, but the position has only deteriorated since. In FY23, the import dependency stood at an all-time high of 87.4%, with industry insiders projecting a similar, or even slightly higher, figure for 2023-24.

This expectedly puts a huge strain on the exchequer.

New Delhi’s crude import bill swelled to $158 billion in 2022-23 from $121 billion in the previous year. In FY24, the figure stood at $101.3 billion till January, with the full-year numbers set to be lower on the back of softer energy prices.

Red-hot crude also weighs on other vital parameters of India’s macroeconomic health.

India’s trade deficit—the gap between its imports and exports—narrowed to $240 billion in FY24 from $265 billion in FY23, thanks to benign oil prices. But crude shooting up in response to the Middle East tensions would reverse this positive trend, as oil constitutes around a third of India’s import basket.

This, in turn, will have a spillover effect on the currency by spurring dollar demand.

Though the Reserve Bank of India's forex market interventions have propped up the rupee, there’s a limit to the central bank’s arsenal. So, it was not without reason that the rupee slumped to a lifetime low of 83.53 against the US dollar in intra-day trade on 16 April.

Elevated oil prices also stoke inflationary pressures on the economy by driving up prices of petrol and diesel, which has a cascading effect on prices of other goods and services.

While retail inflation moderated to 4.85% year-on-year in March, it is still above the RBI’s target of 4%. However, weather-related idiosyncratic events (which can propel food inflation) and rising oil prices are among the most potent threats to the moderating trend in inflation, analysts at Morgan Stanley said.

It would not be an exaggeration to say that crude oil is the fulcrum on which India’s macro vigour depends.

“Rising crude oil prices and resurgence in commodities and soaring geopolitical tensions are increasing risks to India’s external sector. Even as non-IT sector exports remain strong and global growth helps to limit the downside to merchandise exports, we remain watchful of the emerging risks," Elara Capital said in a note dated 16 April.

Macro worries aside, the market is also fretting about the repercussions on the corporate sector.

Tyre and paint manufacturers, fast-moving consumer goods (FMCG), carbon black and lubricant makers and specialty chemicals firms are heavily reliant on crude oil and its derivatives. Soaring crude prices can put pressure on their margins by increasing raw material costs.

The biggest blow, of course, will be on state-owned oil marketing companies in the event of pump rates not being hiked—highly probable as we head into the all-important general elections.

“Overall, we see elevated crude/refined product prices as negative for integrated margins of oil marketing companies. Every Re 1 change in gross marketing margin impacts consolidated Ebitda of HPCL/BPCL/IOCL by 25%/22%/23% for FY25," domestic brokerage firm Motilal Oswal said.

While the Q4 earnings season will not see any impact, companies will keep a wary eye on the geopolitical temperature in the current fiscal year.

The Sensex tumbled by over 1,300 points in two sessions following Iran’s drone strikes—the first time that it has attacked Israel directly—but market experts say their base case scenario remains that de-escalation efforts will douse the flames.

While death, taxes and West Asian crises may be the three certainties of life, there is a fourth factor that perhaps trumps them all. And that is hope.