Markets

Markets

Is India’s cement sector finally turning a corner?

")

Summary

- Marginal price gains signal hope for India’s cement sector, but will that be enough?

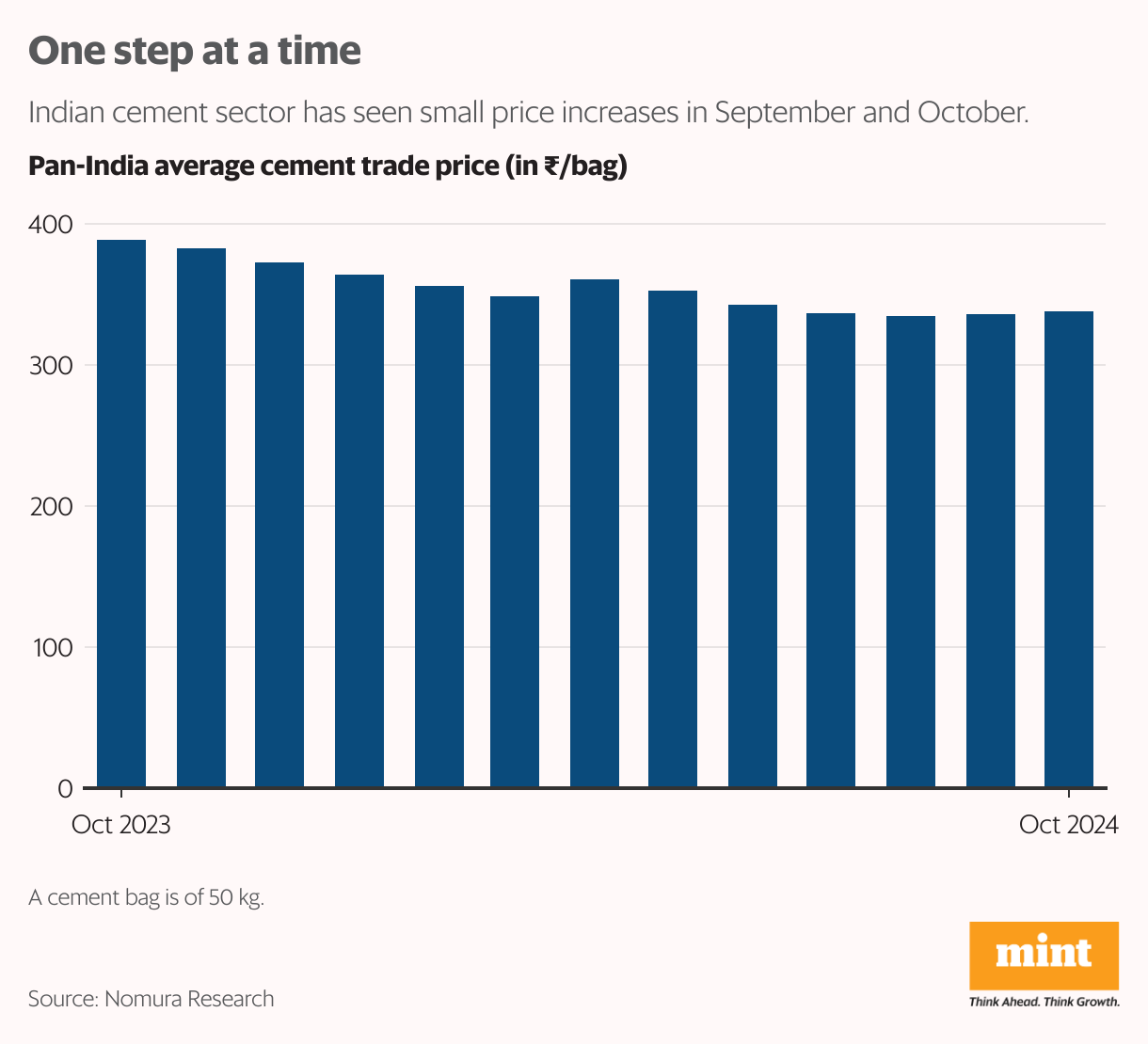

For a second consecutive month, cement prices have inched higher in October. While the increase is marginal, it does offer some relief to investors as weak price trends lately have been hurting the sector’s realization outlook.

After all, cement prices hit a three-year low in the September quarter (the financial second quarter of 2024-25). Pan-India average trade price in October so far has increased slightly, by ₹2/bag month-on-month, to ₹338/bag, according to a dealers channel check by Nomura Global Markets Research on 9 October. In the trade segment, cement is sold by companies to dealers, who in turn sell the product to consumers.

In September, cement price was up ₹1/bag month-on-month.

But the increase is not uniform and is led by better traction only in certain markets. For instance, west India has seen the highest increase of ₹8/bag month-on-month even as other regions struggle. “The volume share tussle in eastern India and rains in the central region have resulted in a price moderation of ₹5/bag and ₹3/bag, respectively," Nomura said in its report.

A bump-up in demand

A few months ago, cement companies had to roll back price increases due to muted demand amid elevated competition. Demand in the second half of FY25 is expected to be relatively better than in the first half, but the sustainability of price increases remains to be seen.

Cement demand is expected to rise post-festival season in the ongoing third quarter (October-December) and then pick up meaningfully in the fourth quarter, which is a seasonally strong period for the sector as infrastructure and home-building activities tend to pick up. But after subdued sales volume growth in the first half of FY25, cement manufacturers are likely to push volumes strongly in the second half of the year, thus keeping the pricing outlook bleak.

Plus, the capacity addition spree by large cement makers, especially through the inorganic route, could prompt companies to keep sacrificing on realizations for volumes. The pace of consolidation in the sector is expected to further increase, thus giving more production/market share muscle to larger companies.

However, incremental cement supply from recent acquisitions does not bode well for prices if demand fails to recover meaningfully. So, even if these small price hikes are sustained, they may not be enough to turn around the sector’s near-term realization outlook.

As for demand, overall, volumes are likely to grow 4-5% in FY25 (on account of the general election, a slowdown in construction activities, and a higher base), slower than the initial expectations of 7–8% year-on-year growth, estimates Nuvama Research. This would be a sharp deceleration from the around 9% year-on-year growth witnessed in FY24, it said in a report on 11 October.

Easing costs

The only breather for the cement sector comes from easing input costs. Costs of imported petroleum coke and coal softened sequentially in the second quarter, the benefits of which are likely to reflect with a lag in the third and fourth quarters of FY25. This should aid profitability and help offset the adverse impact of weak prices to some extent.

As things stand, cement companies remain exposed to the threat of more earnings downgrades, especially after a weak financial first half. Large cement stocks UltraTech Cement Ltd, ACC Ltd and Ambuja Cements Ltd have given 5-13% returns in 2024 so far, with valuations remaining unattractive.

“We expect Q2FY25 to be a washout quarter, but a reversal with a price hike in September and seasonal tailwinds of H2 suggest a sequential recovery in margins in H2FY25E," Kotak Institutional Equities said in a report dated 10 October. The brokerage has trimmed its earnings and fair value estimates for cement stocks under its coverage universe and sees significant risk to consensus earnings for FY26.