Markets

Markets

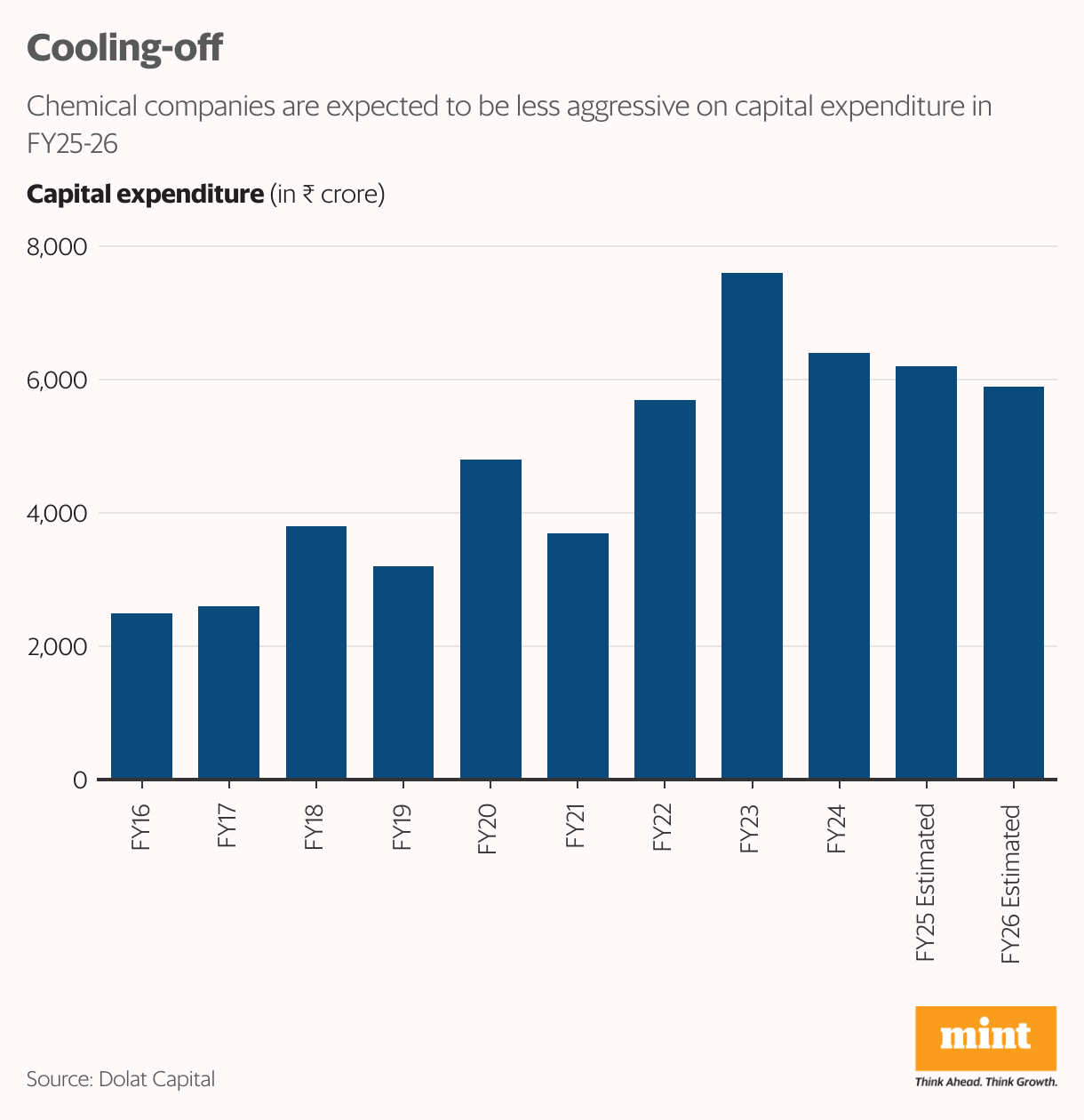

Chemicals companies’ capex intensity is poised to take a breather

")

Summary

- After three years of investing significantly in capacity building, the focus is likely to be on ramping up output, operating leverage and improving cash-flow generation

Chemical companies are set to further moderate their capital expenditure intensity after having invested significantly in capacity building over the past three years. FY24 was a tough year for the sector. Listed chemical makers grappled with issues such as excessive inventory and Chinese dumping of excess produce, exported at low prices across geographies.

A demand slowdown and pricing pressures severely hurt the earnings growth of Indian companies. Analysts at Dolat Capital Market said FY24 was particularly weak, with chemical companies that they cover posting a decline in revenue/Ebitda for the first time in 10 years. Additionally, Ebitda margins slid to a multi-year low.

In this backdrop, chemical companies are expected to realign their capital allocation requirements. Large companies in this sector have softened their near-term stance on capex. SRF Ltd has targeted ₹2,000-2,100 crore of capex in FY25 after spending about ₹3,000 crore in FY24.

The managements of Atul Ltd and Sudarshan Chemical Industries Ltd said their capex cycles are largely done. In FY25 and FY26, the focus is likely to be on ramping up production, operating leverage and improving cash flow generation. For now, companies are not expected to borrow more to invest in non-critical projects.

However, the anticipated moderation in capex intensity brings no good news for the sector’s debt levels. The increase in working capital needs is expected to push net debt higher in FY25 and it could remain elevated.

India Ratings & Research Ltd expects the sector’s net debt to rise to ₹18,000 crore in FY25 from ₹17,000 crore last year. The sector’s debt has been on the rise since FY22 due to a contraction in Ebitda margins and sustained capex. It remains to be seen whether net debt peaks in FY25.

Meanwhile, the global demand environment remains challenging, with a recovery likely only in the second half of FY25. Overseas demand, especially from Europe, is expected to be muted due to elevated inflation.

On the bright side, domestic demand is expected to be on a better footing, aided by end-use industries such as paints and pharmaceuticals. That said, the sector’s margins and realisations are unlikely to recover quickly in FY25.

Investors should temper their expectations of the earnings performance of chemical companies in FY25. Unless the key parameters improve, the threat of further downgrades to FY25/FY26 earnings estimates remains.

Also Read: Recovery in sight for SRF’s chemicals biz