Colgate’s Q3 is dull, and near-term growth woes cannot be brushed off

")

Summary

- Colgate-Palmolive (India) faces challenges from soft urban demand, stiff competitive, and margin pressures. While innovation remains a bright spot, analysts are cautious, downgrading earnings forecasts amid tough macroeconomic conditions.

Shares of Colgate-Palmolive (India) Ltd have fallen approximately 30% from their 52-week high of ₹3,890 on 30 September. However, this decline isn’t without cause.

“Enhanced execution by the management in the core portfolio has helped Colgate re-rate in the past," pointed out an Emkay Global Financial Services report, adding, “But given the demand pressure, surge in competitive intensity, and peak margin, the stock has seen a de-rating in the last four months."

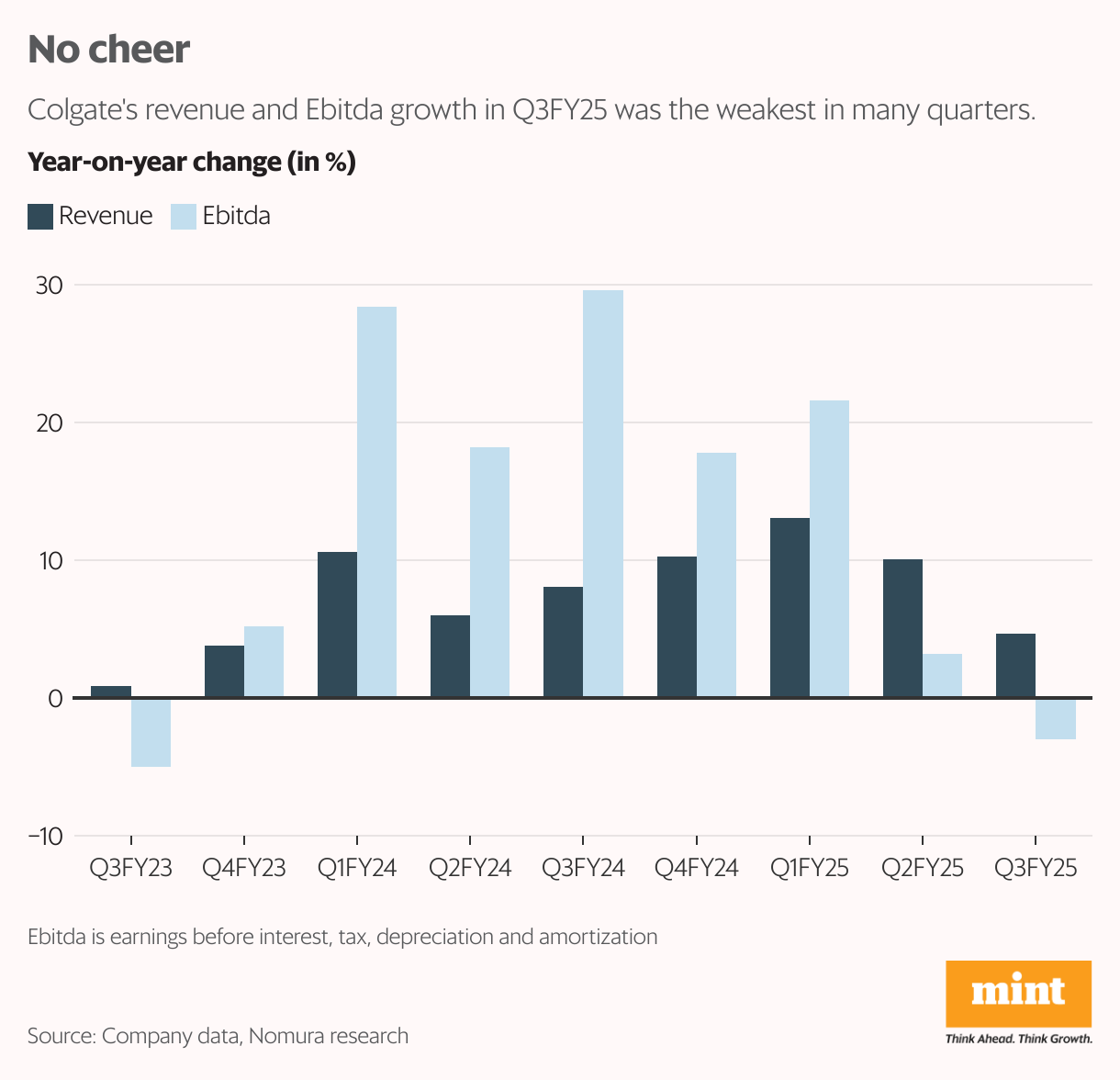

Unfortunately, Colgate’s December quarter (Q3FY25) results will be of no major help in reversing this downward trend. A year-on-year (YoY) revenue growth of 4.7% marked the lowest in several quarters. Domestic growth stood at 3.2%, which is a tad lower than the mid-single digit growth clocked by Hindustan Unilever Ltd in its oral care segment led by Closeup.

Colgate also struggled with soft urban demand and a more competitive market. Toothpaste volume growth was in the mid-single digits, which is relatively resilient amid tough market conditions, but any recovery is expected to be gradual.

Read this | Godrej Consumer Q3: A perfect storm of cost pressures, weak demand

“We expect price hikes to rise gradually in the coming quarters, but volumes could remain strained as the company starts to cycle a high base," said a report by Nomura Global Markets Research.

Colgate’s Q3 margin contracted by 248 basis points YoY to 31%, despite lower staff and advertising costs. Consequently, Q3 Ebitda declined 3% to ₹454 crore.

The Colgate management has said it continues to see positive momentum in its premium portfolio, bolstered by science-backed innovations. Last quarter, the company launched a tech-driven initiative offering artificial intelligence (AI)-generated dental screening reports, followed by recommendations and connections to free check-ups with dentists in partnership with the Indian Dental Association.

Additionally, the company’s innovation pipeline remains robust, including the launch of MaxFresh Sensorial range on e-commerce, building on the success of Visible White Purple.

However, given the challenging macroeconomic conditions, several analysts have downgraded earnings estimates. Nomura has reduced its FY25-27 earnings per share forecast by around 2%, reflecting the weak Q3 performance. The brokerage now values Colgate shares at a P/E multiple of 42x, down from 49x earlier, in line with its 10-year average. This revision accounts for the company cycling a high-volume, high-margin base, which is likely to strain its fundamentals.

Also read | Another tough year for consumer staple companies?

Investors will be watching volume growth closely in the coming quarters and whether urban demand trends improve.