MCX vs BSE valuation: Is the premium justified? A deep dive into commodity vs equity exchanges

Both MCX and BSE show strong return on average equity, but MCX's earnings from volatile commodities raise concerns about sustainability, particularly if crude oil prices stabilize.

Exchange stocks are in focus after Securities and Exchange Board of India chairman Tuhin Kanta Pandey said over the weekend there were no obstacles for the National Stock Exchange of India’s initial public offering. The two prominent listed exchange stocks are the Multi Commodity Exchange of India Ltd (MCX) and BSE Ltd.

Exchanges are a lucrative business with either a duopoly or triopoly and a healthy Ebitda margin at more than 50% in most cases. The margin can continue to expand as it is a highly scalable model with low incremental capital expenditure and operating expenses. As a result, the return on average equity (RoAE) remains strong.

UBS and other brokerages released reports on MCX on 24 June, with the former setting a target price of ₹10,000. The stock jumped over 5% following the reports, touching a new 52-week high of ₹8,808.

As per Bloomberg consensus estimates, BSE’s shares trade at 39x its FY27 earnings per share versus 49x for MCX. Both are likely to have a similar RoAE of 37% for FY27, going by Bloomberg estimates.

Is MCX’s valuation premium over BSE justified? Brokerages cite volatile commodity prices in view of geopolitical tensions, new product launches such as monthly bullion contracts versus bi-monthly earlier and diversification efforts into electricity derivatives as tailwinds.

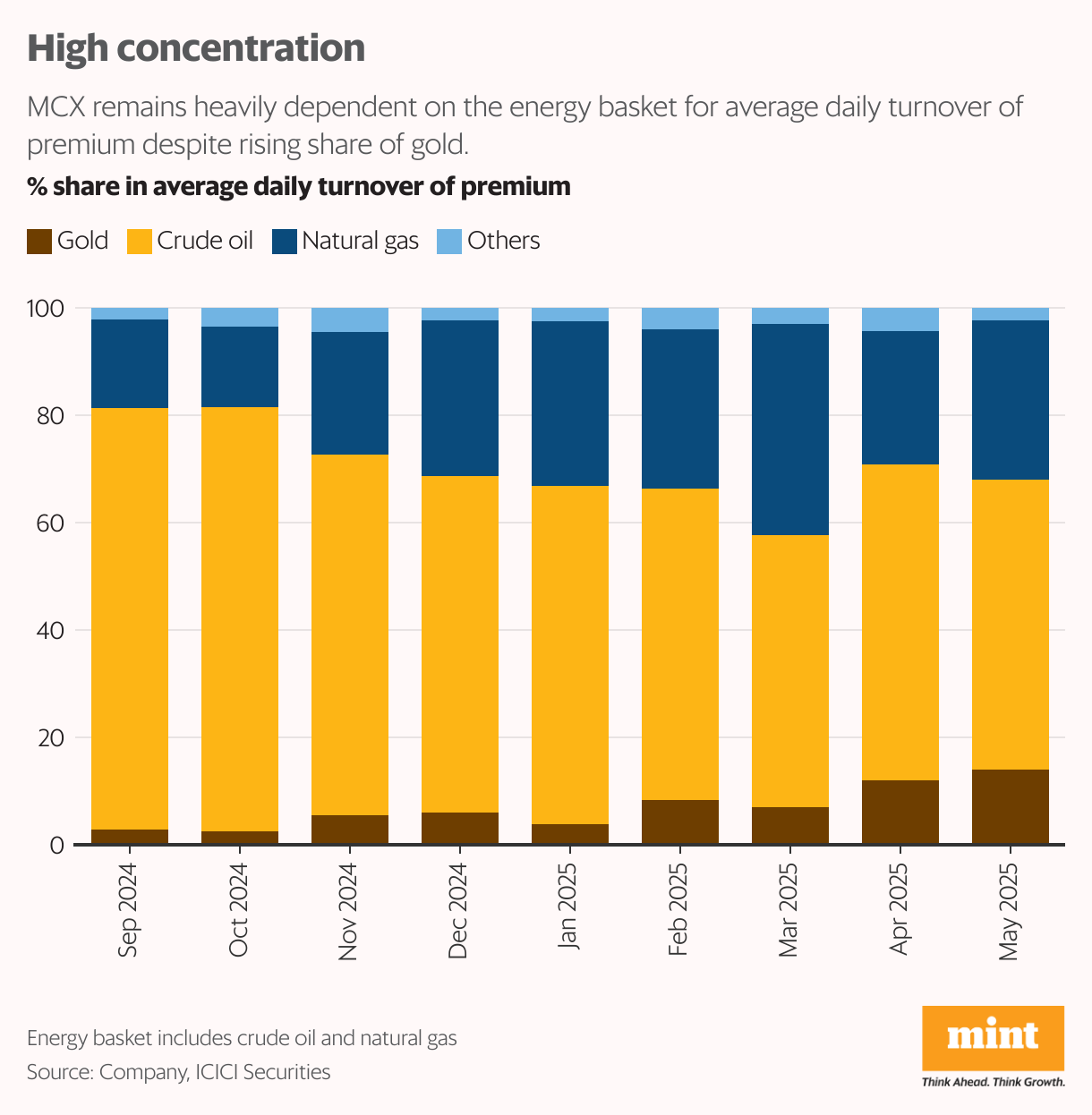

However, the earning profile of a commodity exchange could be more volatile than that of a stock exchange. In FY25, MCX's transaction charges from derivatives formed almost 87% of its total revenue.

About 70% of the transaction charges came from options trading. Within options, the share of energy options premium (mainly crude oil) still remains high at 84% so far in Q1FY26 (April and May) even though it fell from 90% in Q4FY25.

The bulk of the remaining is bullion options premium, which remains small despite growing fast after the shift from bi-monthly expiry to monthly expiry introduced in November.

Downside risk

If volatility in crude oil prices subsides as geopolitical tension eases, there could be a downside risk in transaction charges from crude trading as the options premium is linked directly to volatility in the underlying commodity.

The diversification beyond crude oil is yet to happen. UBS estimates electricity derivatives may contribute only 3% of total revenue by FY28.

In comparison, transaction charges formed 69% of BSE’s total revenue in FY25, while listing and other fees from companies listed on the bourse accounted for 17%. Annual listing fees are recurring in nature and likely to grow in future as more companies get listed.

The Street could be assigning a valuation premium to MCX over BSE because of its near-monopoly status. MCX has a 98% market share in commodity futures, according to its FY25 presentation.

Thus, NSE, with its cash equity market share at 95% and equity options premium market share at 80% in FY25, would have been a better comparable exchange if it was listed. Data from the unlisted market shows NSE quotes at a price-to-earnings multiple of about 47x based on FY25 earnings, which means the multiple should drop for FY27 estimates. So, even compared to NSE, MCX looks fully priced.

The MCX stock has surged by more than 60% since 31 March as the Street might have factored in robust June quarter (Q1FY26) results. MCX’s average daily trading volume in futures and options premium is up 50% QoQ and 30% QoQ, respectively, so far in Q1.

Unless there are more positive surprises in store, further upside could be capped in the short term. Moreover, the scarcity premium for exchange businesses may reduce if the NSE’s IPO fructifies.