Markets

Markets

Could Apollo Hospitals’ expansion plan help its stock recover?

Summary

- The stock is languishing below the ₹6,258.60 level it was at on 26 April, when the company announced it was selling a 12.1% stake in its pharmacy business to a PE firm at a lower-than-expected valuation.

Apollo Hospitals Enterprise Ltd investors are yet to get over the disappointment of a lower-than-expected valuation in the stake sale of its pharmacy business.

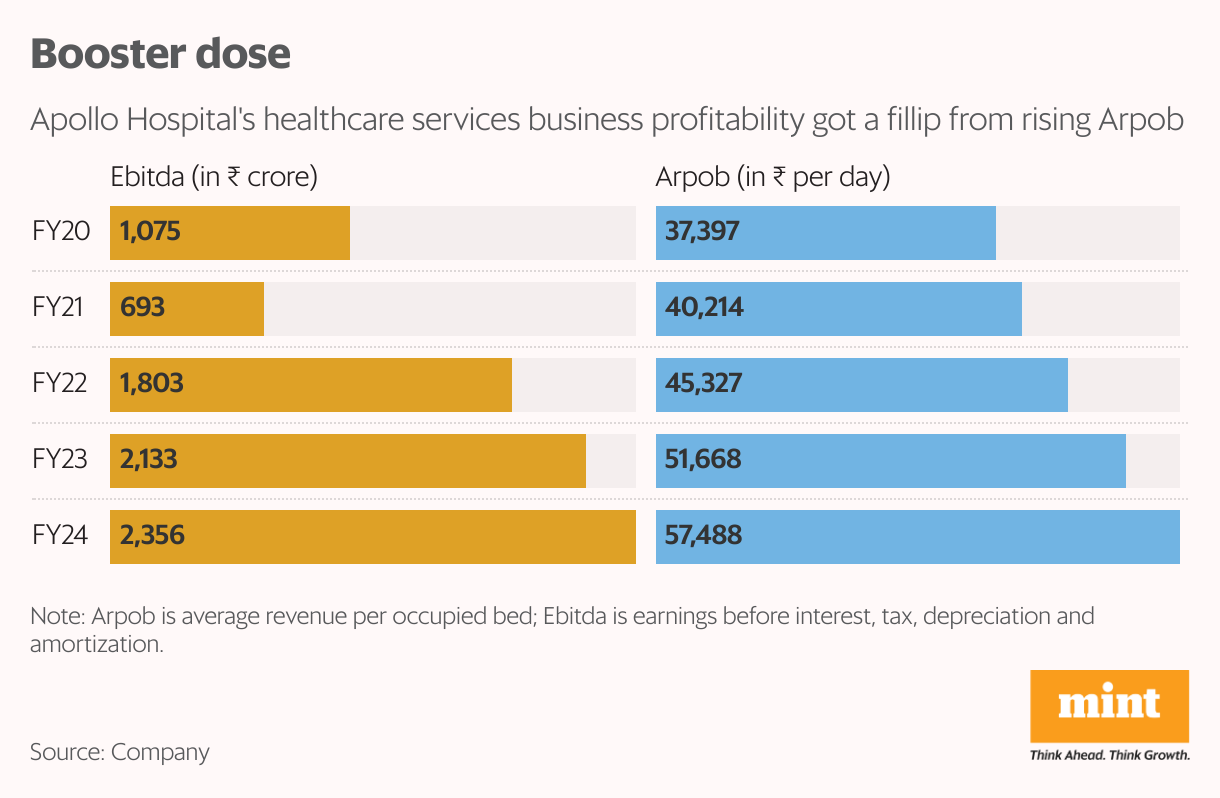

The stock is languishing below the ₹6,258.60 level it was at on 26 April, when the deal was announced. It has largely been indifferent since the company announced its FY24 results after market hours on Thursday. The mainstay healthcare-services business saw 10% year-on-year growth in Ebitda to ₹2,356 crore in FY24, largely on the back of an almost equivalent rise in average revenue per occupied bed (Arpob) to ₹57,488. The double-digit Arpob growth was due to a reconfiguration of general-ward beds into semi-private and private sections in certain locations, with case mix also playing a part.

Also read: Apollo to Aster, Manipal to Max, hospital chains ready for a big-bang expansion

Note that the 24% Ebitda margin of the healthcare business is almost four times that of the adjusted-Ebitda margin of the pharmacy business. Here, the pharmacy business includes offline, online, digital app Apollo 24/7, and promoter group company Keimed, which will be merged with the existing pharmacy business as a part of the deal. The adjusted-Ebitda margin for pharmacy has been arrived at by adding back Esop and new business costs of Apollo 24/7.

Stake sale to Advent International

Based on an equity transaction by Advent International Private Equity, the pharmacy business forms just about 15% of the company’s total market capitalisation of ₹85,250 crore. The PE fund acquired a 12.1% stake for ₹2,475 crore, which means the 59% stake of Apollo Hospitals is worth ₹12,000 crore.

The remaining market capitalisation can be ascribed mainly to healthcare services as the retail health and diagnostics business is still tiny. Negligible net debt in the healthcare-services business means the market capitalisation and enterprise value are the same. Based on FY24 results, the EV/Ebitda multiple works out to nearly 30x. This valuation must be seen in the context of the business’ growth prospects over the short-to-medium term.

Also read: Avendus launches ₹3,000-cr late-stage fund to invest in tech, healthcare firms

For FY25, management has guided for 15% growth in healthcare services, with an Ebitda-margin target of 25%, up from 23.7% in FY24. Over the next three years, the company aims to grow its operating bed capacity at a CAGR of 9% to FY27.

To be sure, the real boost to earnings comes from increasing the occupancy rate and Arpob. Management has been adding new doctors across cities by spending on advertising and marketing to achieve higher occupancy. It remains to be seen whether that bears fruit as the occupancy rate for FY24 was 65%, below the pre-covid high of 67% in FY20. Arpob provided succor, clocking 11% CAGR from FY20 to FY24.

Little room for multiple expansion

Notwithstanding lower valuations from the Advent deal, investors may be pleased if management delivers on its goal of increasing revenue to ₹25,000 crore over the next three years, with an Ebitda margin of 8% for the entire pharmacy business.

In FY24, revenue and adjusted Ebitda for the pharmacy business were ₹15,600 crore and ₹890 crore, respectively. The valuation of the pharmacy business and Apollo Hospital Enterprises’s holding could therefore double in tandem with Ebitda, even if the valuation multiple remains the same as it was in the stake sale. The incremental value of holding of the pharmacy business could thus be another 15% of the current market cap.

Also read: Why Tata Capital Healthcare Fund is wary of healthtech bets

After deducting the pharmacy valuation from the market cap, the implied EV/Ebitda multiple of Apollo's healthcare business is 23 times projected FY25 earnings, which is in line with the historical average multiple of the entire company. With little room for the multiple to expand, the stock’s returns will track the company’s growth trajectory.