Butterfly needs to take off for Crompton to get second wind

- It's crucial for Butterfly's business – which clocked an Ebit loss of nearly Rs2 crore in Q3FY24 – to rebound if Crompton's stock is to perform well.

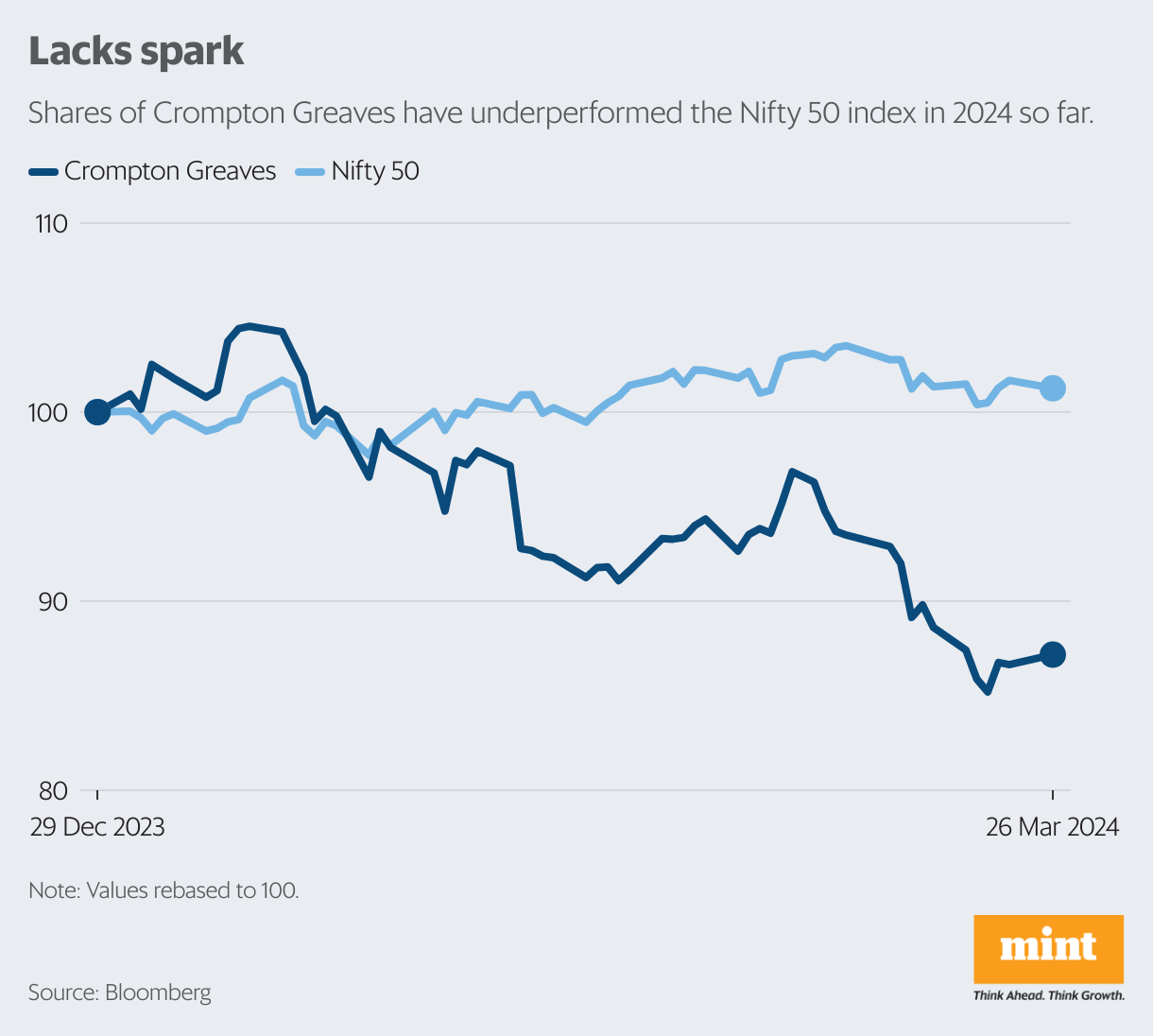

Investors in Crompton Greaves Consumer Electricals Ltd are a worried lot, with the stock down by 13% so far in 2024. A key factor souring investor sentiment is the delay in the turnaround of Butterfly Gandhimathi Appliances Ltd, in which it has a 75% stake.

It may be a while before there’s respite on this front, but there are some comforting factors at the moment. Crompton’s management recently told analysts that its fans portfolio is seeing strong traction, which will lead to a healthy March quarter (Q4FY24). Moreover, demand for fans is likely to be firm in the coming months as this year’s summer is expected to be severe.

Crompton has also hiked the price of its fans significantly, which will aid margin. “Of the total cost increase of 15% necessitated by the new energy norms, the company recovered around 8 percentage points through value engineering and has clawed back most of the rest through price increases," Kotak Institutional Equities wrote in a report on 25 March, after its analysts met representatives of Crompton. It’s worth noting here that despite the price hikes, Crompton has seen market-share gains, the Kotak report added.

Another area where Crompton has hiked prices is the pumps business. The company views this business as a cash cow, and its growth will be driven by demand for agriculture and solar pumps. The PM-KUSUM scheme, in which the government plans to install 1.4 million solar agriculture pumps, also offers opportunities.

Fans and pumps are part of the electric consumer durables segment, which contributed more than 72% of Crompton’s consolidated revenue in the nine months to December (9MFY24). Here, the impact of rising competition remains a key factor to monitor. In the lighting segment, Crompton has managed to arrest the revenue drop but price erosion remains a sore spot.

Antique Stock Broking, which also met the company’s management, noted that innovation and marketing spends would lead to market-leading revenue growth. “However, it will also exert pressure on margins in the near term. Crompton expects these initiatives to reap dividends and help regain its mid-teens operating margins in the medium term," read the Antique report. In 9MFY24, Crompton clocked a consolidated Ebitda margin of 9.5%.

Against this backdrop, it is crucial for the Butterfly business – which clocked an Ebit loss of nearly Rs2 crore in Q3FY24 – to rebound. Management expects to complete the restructuring of the business by Q1FY25. The pace at which it picks up after that will determine to a large extent how Crompton’s stock performs.