Cummins India revs up its growth engine, but a risky ride awaits

- The engine maker is confident of growing at twice the rate of India’s GDP, which translates to 13-14% growth in FY25. But risks – such as weaker-than-expected demand in key industries, rising commodity prices, stiff competition and a sluggish export recovery – persist.

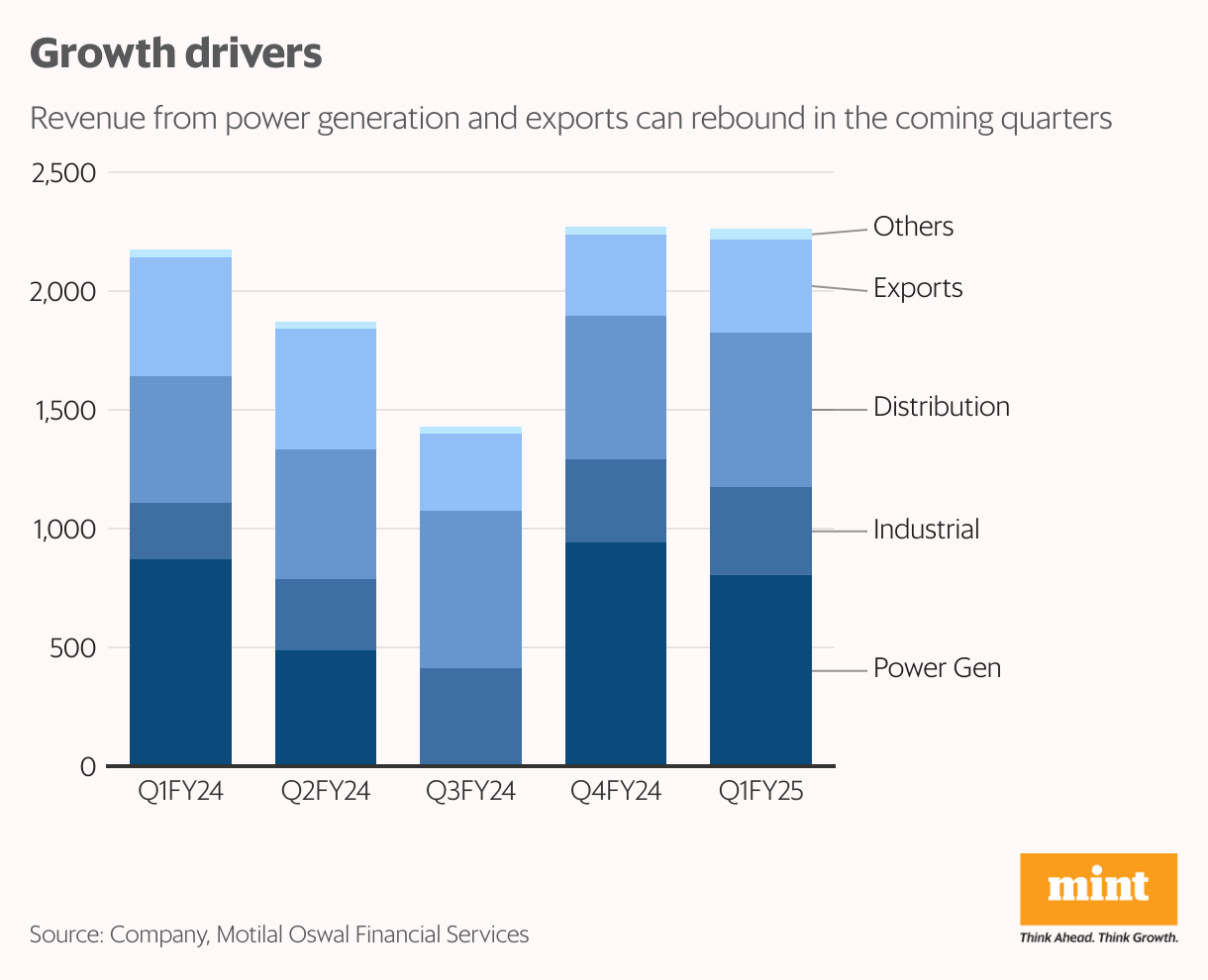

Cummins India Ltd is showing resilience in a market reshaped by stringent emission norms and shifting dynamics. True, strong domestic demand has helped at a time when exports aren’t picking up. In FY24 and the June quarter (Q1) of FY25, the capital goods company saw growth in domestic revenues, but its exports revenues fell.

Cummins derives a large portion of its domestic revenue from its power generation vertical, which could prove to be the joker in the pack as clarity emerges on the impact of the new CPCB IV+ emission norms, which took effect on 1 July. The prices of various genset categories have risen 15-25% under the new norms, so much depends on how consumers take to the higher prices.

Implemented by the Central Pollution Control Board (CPCB) in July 2023, the CPCB IV+ emission norms are more stringent than the previous CPCB II standards and aim to reduce the environmental impact of diesel generators by lowering harmful pollutant emissions.

Also read: Why the Street is excited about Gujarat Gas’s restructuring despite concerns

“From our recent interaction with management, Cummins India appears to be well-positioned to benefit from the change in emission norms for diesel gensets," analysts at Motilal Oswal Financial Services said in a report published on Friday. “Demand for data centres is growing in high double digits, and Cummins’s HHP (high horsepower) portfolio is constantly benefiting from this demand," said the brokerage. Solid demand and pricing gains are expected to drive growth in the foreseeable future. “In the CPCB IV+ segment, the market will stabilise in the coming quarters, with only CPCB IV+ products being available," said the Motilal Oswal report.

In a sweet spot

Despite government initiatives to boost power capacity and the growing viability of batteries as alternatives, the demand for gensets as backup power remains robust, and Cummins is well-positioned to capitalise on this. Plus, with CPCB IV+, the company is undergoing a strategic shift from a commodity player to one that invests in technology and high-warranty products.

Also read: Indian manufacturers’ confidence has taken a hit. There may be more pain ahead.

Meanwhile, Cummins’s distribution business has grown steadily over the past few years, helped by a growing installed base and better utilisation rates. It should benefit from increased market penetration, particularly in tier-2 and tier-3 cities, and demand for spares and services related to the pricier CPCB IV+ gensets. The introduction of the Ashwasan 4+ extended warranty for new gensets in Q2FY25 is likely to further increase customer loyalty.

So far, so good. But as mentioned earlier, exports revenues have been a sore spot and are down 18% and 22% year-on-year in FY24 and Q1FY25, respectively. Exports comprised 19% total revenue in FY24 and 17% in Q1FY25. Factors that hurt exports include price disruptions caused by dumping from other countries throughout FY24 and a general weakness across segments and countries.

Signs of a recovery

The pain seems to be easing, though. Cummins is seeing green shoots of a recovery in the Middle East and Africa, but Europe remains flat. The company is strategically positioning its CPCB IV+ products in anticipation of a recovery in global demand.

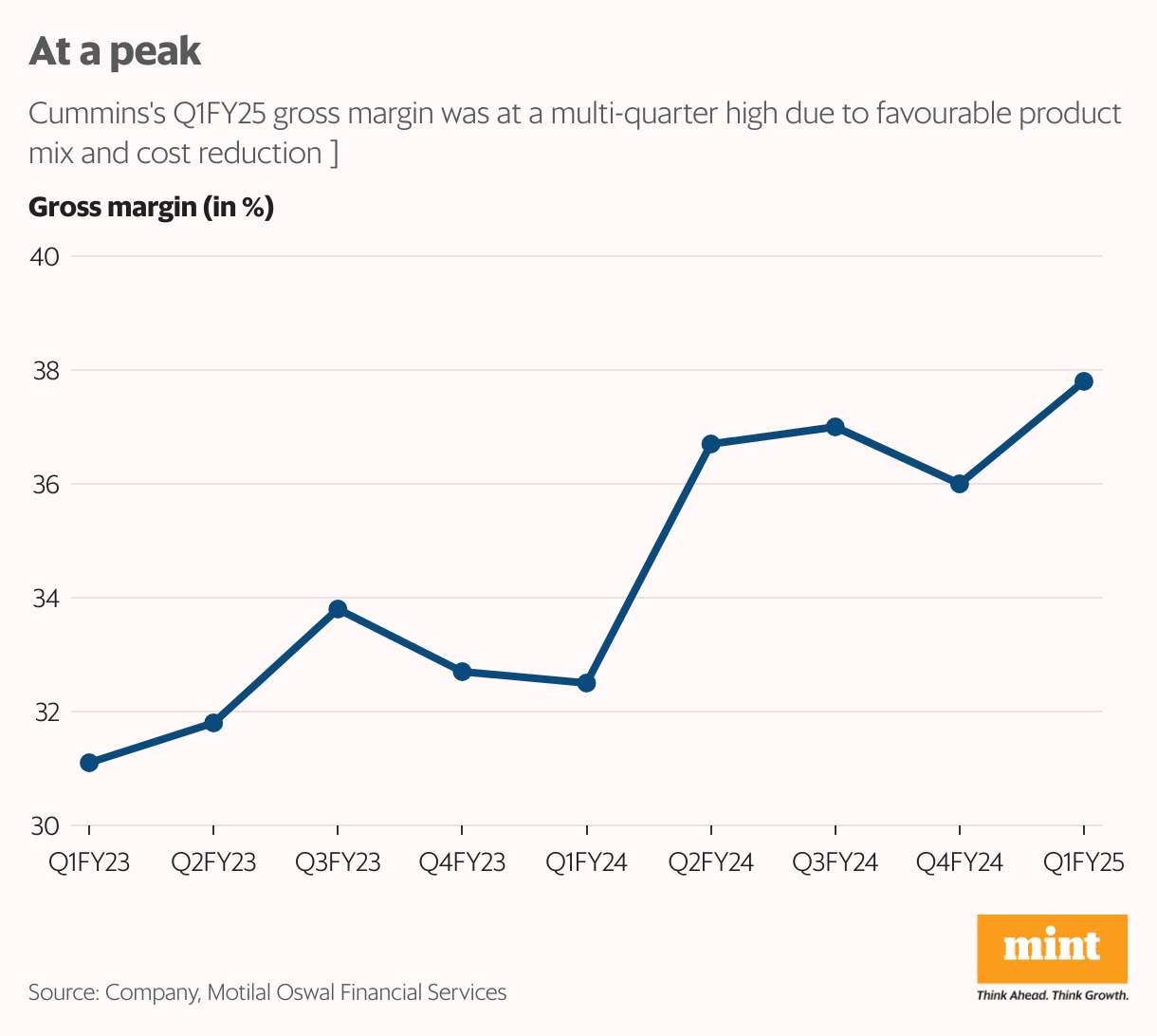

On profitability, gross margin touched a multi-quarter high of 37.8% in Q1FY25, led by favourable product mix and tapering commodity prices. Cost reduction initiatives rolled out in FY23 also aided the margin. Even so, such a high margin may not be sustainable amid an increase in commodity prices and competition. To mitigate this, Cummins is focusing on cost localisation, and aims to indigenise 75-80% of its CPCB IV+ product costs by FY26.

Also read: Hotels eye more room for growth with renovations

It is confident of growing at twice the rate of India’s GDP, which translates to 13-14% growth in FY25. Cummins’s shares have gained as much as 95% so far in 2024, suggesting investors are capturing the optimism adequately for now. The stock trades at 42 times estimated FY26 earnings, showed Bloomberg data.

Nonetheless, risks such as weaker-than-expected demand in key industries, rising commodity prices, stiff competition and a sluggish export recovery persist. “A key imponderable is whether the cyclicality of market growth in the powergen segment can start hurting on the downside and if other segments (including exports) can cover up in such a scenario," said Kotak Institutional Equities in Q1FY25 review report.