Delhivery part truckload business is on a higher margin path

")

For Delhivery shares, the key trigger remains the impending closure of Ecom Express acquisition and the resulting change in express parcel industry structure, per JM Financial

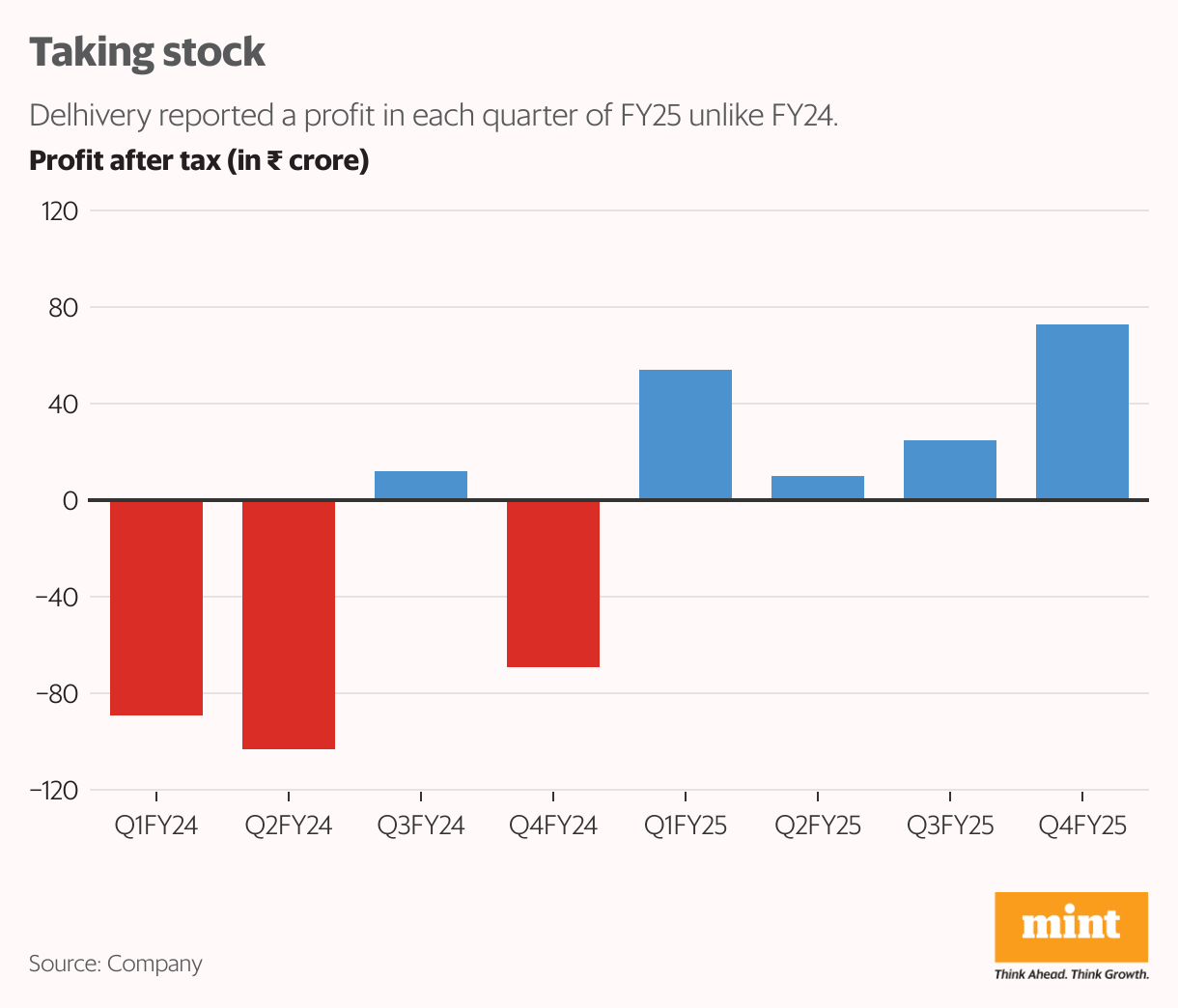

Delhivery Ltd shares have surged over 10% since its March quarter (Q4FY25) results were announced. The company posted its highest-ever quarterly profit, which means that FY25 was the first year in which all the quarters were net profit positive.

Despite a seasonally soft period, Q4 Ebitda margin rose to 5.4%, up 320 basis points year-on-year, led by margin expansion in its part truckload (PTL) business, a segment gaining significance in the portfolio. PTL service Ebitda margin jumpedto 10.8% in Q4 versus 3.8% in Q3 and 2.2% in Q4FY24, helped by better fleet utilisation, network productivity and price hikes that finally stuck. The management pointed out that scale and tech-led automation are now working in tandem. This can pave the way for PTL margin to eventually match that of Delhivery’s core segment: express parcel.

PTL revenue grew 24% in Q4, and freight tonnage climbed 19%. With 80% of the PTL industry still unorganised, the segment offers ample room for growth. On the other hand, the express parcel business saw muted shipment volumes, with revenue up 3.2% driven by 2.7% realizations jump. The business is still coping with pricing pressure, soft consumption trends and rising quick commerce and insourcing at Meesho.

Yet, management remains confident of a rebound in FY26, led by the proposed Ecom Express acquisition, where about 30% volume retention is expected. April and May volumes trending higher is encouraging. While service Ebitda margin at 15.9% still trails FY24 levels (18.4%), easing price pressure and incoming volumes could push margin higher in future, potentially lifting express parcel profitability post-integration.

Also Read: Delhivery expects consolidation wave with Ecom Express acquisition near completion

Meanwhile, Delhivery has launched rapid commerce with 18 dark stores, aiming to scale to 50 in FY26. Mature stores are handling 350-400 orders a day and can hit breakeven at 700-800 orders within 4-5 months.

Emkay Global Financial Services expects only a gradual recovery in B2C volumes with Meesho’s slated goal to continue insourcing. Baking in the Q4FY25 miss, Emkay has cut its FY26 and FY26 revenue estimates by 5% and 6%, respectively.

It helps that the company has cash and cash equivalents worth ₹5,493 crore and capital intensity down to 5.2% of revenue (from 7.5% earlier).

Despite recent gains, the stock has risen just 3% so far in 2025.“The key trigger remains the impending closure of Ecom Express acquisition and the resulting change in express parcel industry structure – a scaled 3PL player not just makes better service Ebitda but also provides the cheapest cost to its customers," said JM Financial Institutional Securities.

Also read | How does the Ecom Express buy position Delhivery for the future?