For DMart, quick commerce threat comes to the fore

")

- Despite DMart chain's strong brand, Avenue Supermarts is struggling with rising costs and shifting consumer behavior. As competition from online grocery formats intensifies, will the company's fortunes revive?

Avenue Supermarts Ltd’s shares fell over 8% on Monday after its September quarter (Q2FY25) earnings missed expectations and concerns rose on growth prospects amid intensifying competition from quick commerce companies. Avenue runs the DMart supermarket chain.

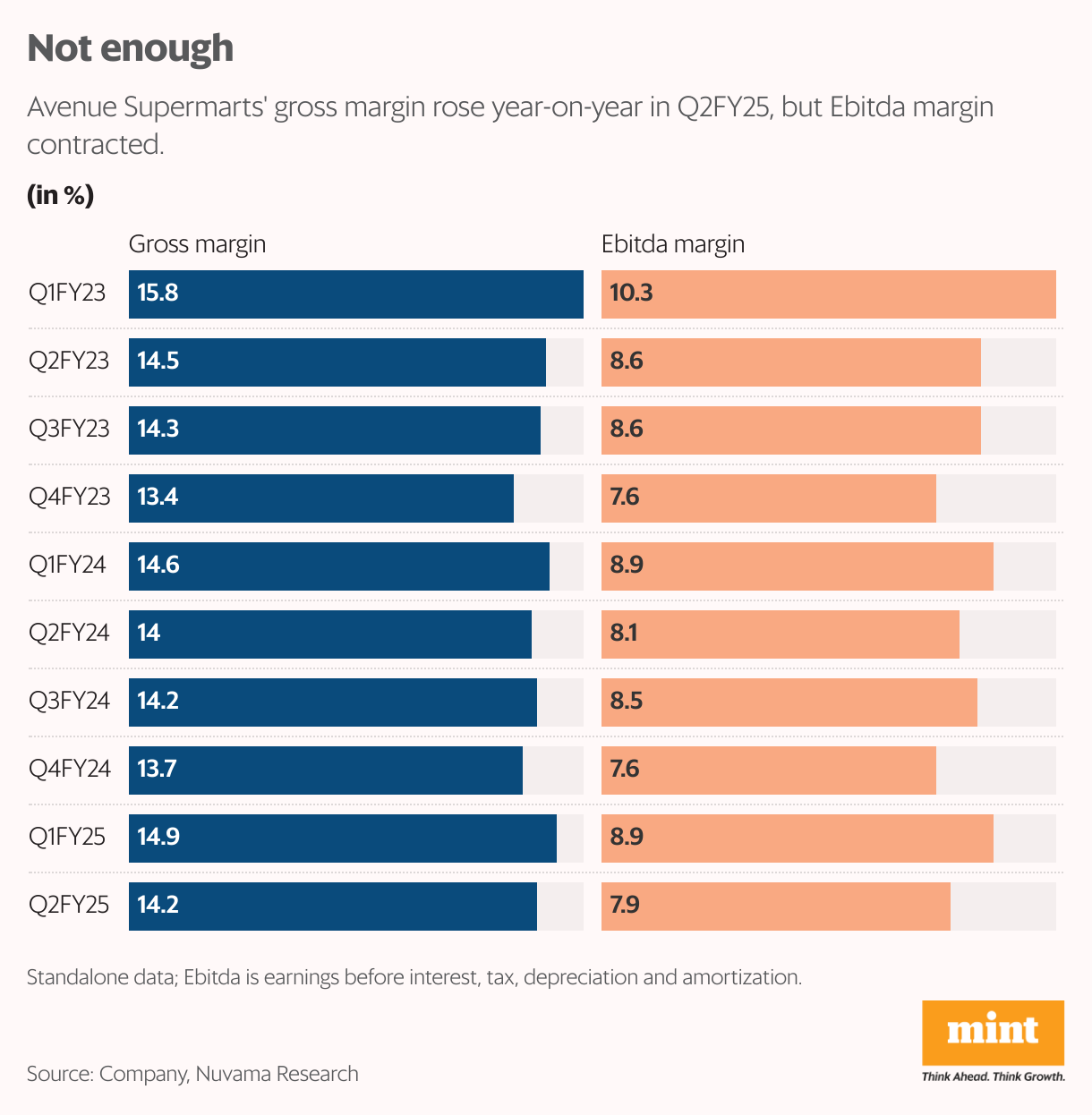

Standalone Ebitda margin in Q2 dropped 27 basis points year-on-year to 7.9%, which was below analysts’ estimates and comes at a time when gross margin expanded 21 bps to 14.2%. Gross margin increased aided by a small rise in the share of revenue from the high-margin general merchandise and apparel segment. However, staff costs and other expenses grew sharply, hurting Ebitda margin and leading to a relatively slower pace of Ebitda growth of 10% to ₹1,105 crore.

But that’s not all. Revenue growth has slowed down. For the first half of FY25, like-for-like revenue growth was 7.4% for stores that are two years and older. However, like-for-like revenue growth for the same cohort of stores was 5.5% in Q2FY25. The company acknowledged that it sees the impact of online grocery formats, including DMart Ready in large metro DMart stores which operate at a very high turnover per square feet of revenue.

Also Read: Small brands jazz up pitches in scramble to join quick commerce platforms

IIFL Securities believes that the impact could gradually spread to other stores too as convenience behaviour catches on and discounting by quick commerce players could increase given higher competition and improving business economics. “We believe that a new equilibrium would be set within the next about 12 months; downgrade risks persist till then," said IIFL’s analysts in a report on 14 October.

DMart Ready, which is Avenue’s online and multi-channel grocery retail business, grew by 22% in H1FY25. This growth by itself looks good, but appears weak when compared to quick commerce companies, said Jefferies India. The brokerage has cut Avenue's FY25-27 earnings per share estimates by 5-6%.

To be sure, the company has been finding it tough to boost sales growth for some time now, mainly due to muted demand conditions. Store additions are one way to push growth. Like last year, Avenue added 12 stores in the first half. Avenue typically adds more stores in the second half of the year.

The stock trades at nearly 70 times FY26 estimated earnings, showed Bloomberg data.Avenue’s valuations remain expensive even after the shares have now fallen by about 24% from their 52-week highs of ₹5,484.85 apiece seen on 24 September. Hereon, investors will watch the impact of disruption by quick commerce companies, along with the pace of store additions.

Also Read | Blinkit to deliver samosas and chai in 10 minutes, expand quick commerce play