Frothy valuations: Reality check for Indian investors

")

Summary

- Investors will closely monitor the timing and the extent of interest rate easing, both in India and globally.

Last week, US Federal Reserve chairman Jerome Powell hinted that interest rate cuts might not be far off if inflation indicators align, though he refrained from giving a timeline. Nonetheless, given the stock market’s ongoing selective bias, the Street seems to be banking on a potential positive outcome. No wonder, Indian equity markets soared to new highs.

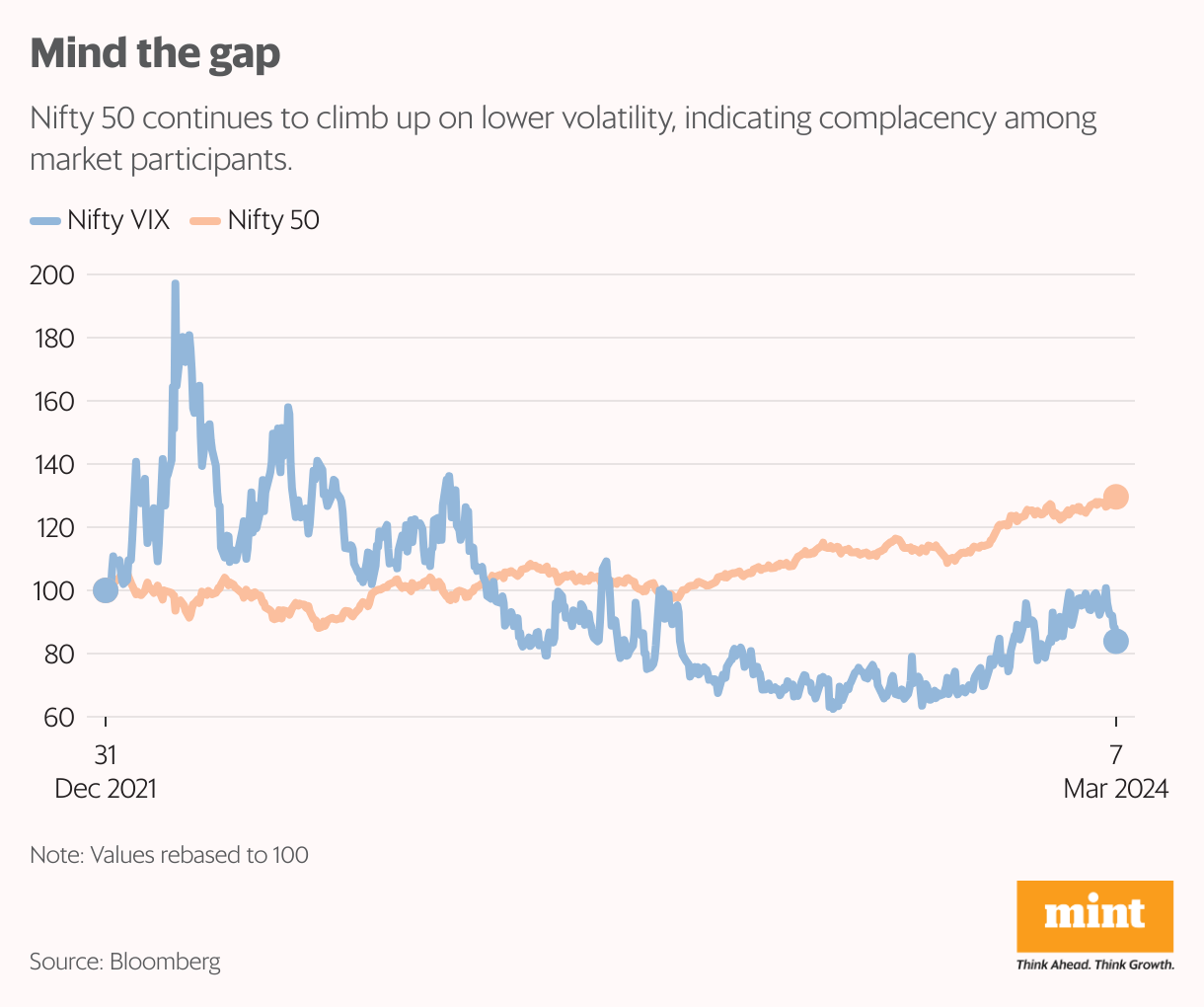

On Thursday, the Nifty50 and S&P BSE Sensex indices rose to all-time record levels of 22,525 and 74,245, respectively. Fear gauge, the Nifty volatility index eased by nearly 5% to end at 13.61. The Indian equity market was closed on Friday for Mahashivratri, but the sentiment in other key Asian markets was upbeat.

A crucial near-term event for Indian investors is the general elections. The probability of political uncertainty is minimal. The incumbent Bharatiya Janata Party’s performance in the recent state elections suggests a favourable outcome for the stock market. But not all is hunky dory. In February, the Nifty50 rose by a mere 1.2%, underperforming most of its global peers. According to Kotak Securities Ltd, this underperformance is due to looming concerns over valuation, outflows by foreign institutional investors and expectations of no major policy decision in the near-term due to general elections.

Foreign portfolio investors were net sellers in Indian stocks in January. They turned buyers in February, but only to the tune of $483 million, showed NSDL data. On the other hand, domestic institutional investors continued to do the heavy-lifting. Strong domestic participation meant an influx of funds into mid- and small-cap counters, irrespective of their fundamentals. This has translated into mid- and small-caps faring better than large-caps lately, making the former’s valuations frothy.

Overall, India’s relative valuation is expensive. The MSCI India index is trading at a one-year forward price-to-earnings multiple of 20 times, a steep premium over MSCI Asia Ex-Japan and MSCI Emerging Markets, showed Bloomberg data. This high valuation persists despite some lingering concerns.

For instance, the December quarter (Q3FY24) earnings of Indian corporates indicated weak consumption demand for staples and discretionary items, as rural demand was impacted by the overall high inflation level, dampening their purchasing power. The outlook on rural demand is mixed amid expectations of an election-led boost, but that would be temporary at best. The trajectory of retail inflation and the monsoon continues to be the medium-term drivers of rural demand. Also, with operating margin tailwinds behind, a meaningful catch-up in revenue growth is crucial.

Meanwhile, the recently published Q3 official gross domestic product (GDP) data also points to some caution. “The robust 8.4% real GDP growth print for Q3 contrasts the grim reality of household consumption and income situation," said a Systematix Shares and Stocks (India) report. “It is thus reasonable to assume that private capex would have remained languid, thereby signifying the continued overreliance on government capital expenditure." Private capex revival is awaited.

Sure, India is viewed as comparatively better placed than emerging market counterparts, but it is not immune to global growth woes. UBS Securities India said India is likely to remain one of the fastest growing global economies. But UBS expects GDP growth to moderate (in FY25 and FY26) due to global (weak growth) and local factors (softness in public capex).

Investors will also closely monitor the timing and the extent of interest rate easing, both in India and globally. Until then, volatility is expected to persist. “After a strong run up of Indian equities, some profit taking in the near term cannot be ruled out as economic and geopolitical risks remain elevated," UBS said in the report dated 7 March.