Godrej Properties has to make room for either capex or debt

- Going ahead, the focus for Godrej Properties would be on generating higher operating cash flows. But the company would need to invest in buying land parcels to drive pre-sales growth

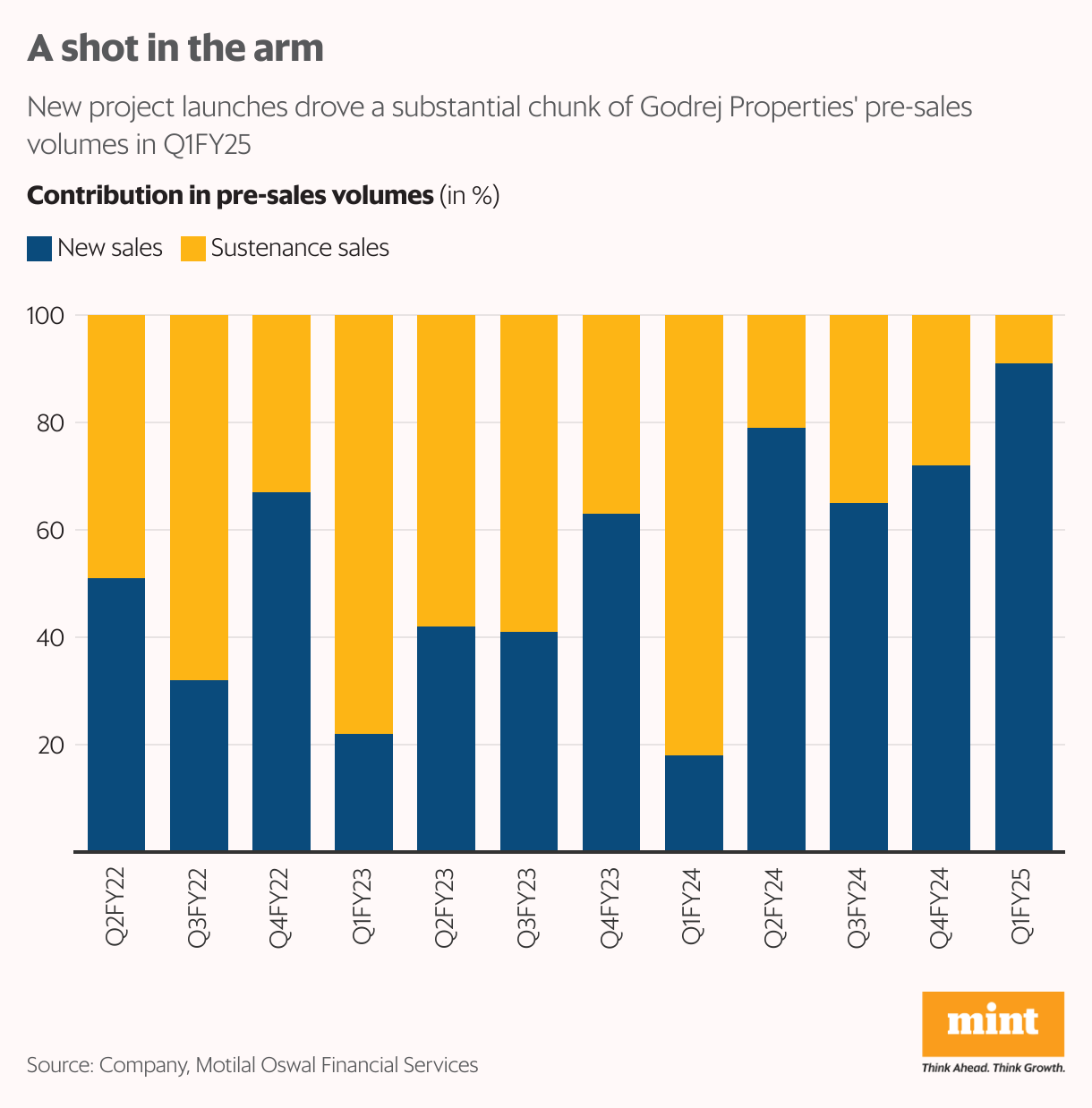

Godrej Properties Ltd has started FY25 on a strong note with pre-sales or bookings in the June quarter rising 283% year-on-year to ₹8,637 crore, aided by the sale of 8.99 million square feet (msf) of area. This marks the company’s highest-ever quarterly sales for Q1.

A spate of new launches of projects worth ₹8,600 crore spanning across 9.8 msf in markets including Bengaluru and National Capital Region (NCR), gave pre-sales a boost during the quarter (Q1FY25).

The management is upbeat on demand for housing units sustaining and is confident of achieving FY25 guidance of ₹27,000 crore for pre-sales and ₹30,000 crore for launches.

Godrej Properties aims to launch around 22 msf of projects/phases in FY25. Here, the company’s diversification efforts are seen working in its favour as they reduce geographical concentration risk unlike for some of its peers.

Five major regions – Ahmedabad, Mumbai, Pune, Bengaluru, and NCR – account for 10–24% of the development pipeline and this is likely to ensure steady growth for the company even if it faces a slowdown in any individual market, said a Nuvama Research report dated 31 July.

Collections in Q1FY25 were a bit softer sequentially at ₹3,010 crore, but the management is confident of meeting its target of ₹15,000 crore in FY25. On the business development front, it added two new projects with gross development value of ₹3,000 crore. The management has guided for ₹20,000 crore of business development in FY25.

Also Read: The Godrej split holds valuable lessons for family businesses

Some sour points for investors, however, are the company’s patchy operating cash flows and higher net debt, given its elevated land acquisition spending. Its net debt in Q1FY25 rose to ₹7,430 crore and net debt-to-equity ratio inched up to 0.71 times. Plus, average borrowing cost also increased to 7.90%. So, concerns are building on its free cash flow outlook.

The management is comfortable with net-debt-to-equity ratio of 0.5-1.1 times. Going ahead, the focus would be on generating higher operating cash flows, which will help in paring debt, the management said. But the company would need to invest in buying land parcels to drive pre-sales growth to meet FY25 target. In that case, striking a balance between maintaining net debt and land capital expenditure can be challenging.

Still the Godrej Properties stock has rallied by 60% so far in 2024, , in the backdrop of improving pre-sales lately. “Despite the marked improvement in performance, the stock performance has been ahead of business performance, with implied valuations of 14X EV/Ebitda trading at a premium to the peer set," said Kotak Institutional Equities report dated 1 August.

Also Read: Removing indexation on real estate will benefit almost nobody. Here's proof.