Markets

Markets

HCL Tech’s rich valuation clouds re-rating prospects

")

Summary

- Valuations are now almost at par with giants Tata Consultancy Services Ltd and Infosys Ltd

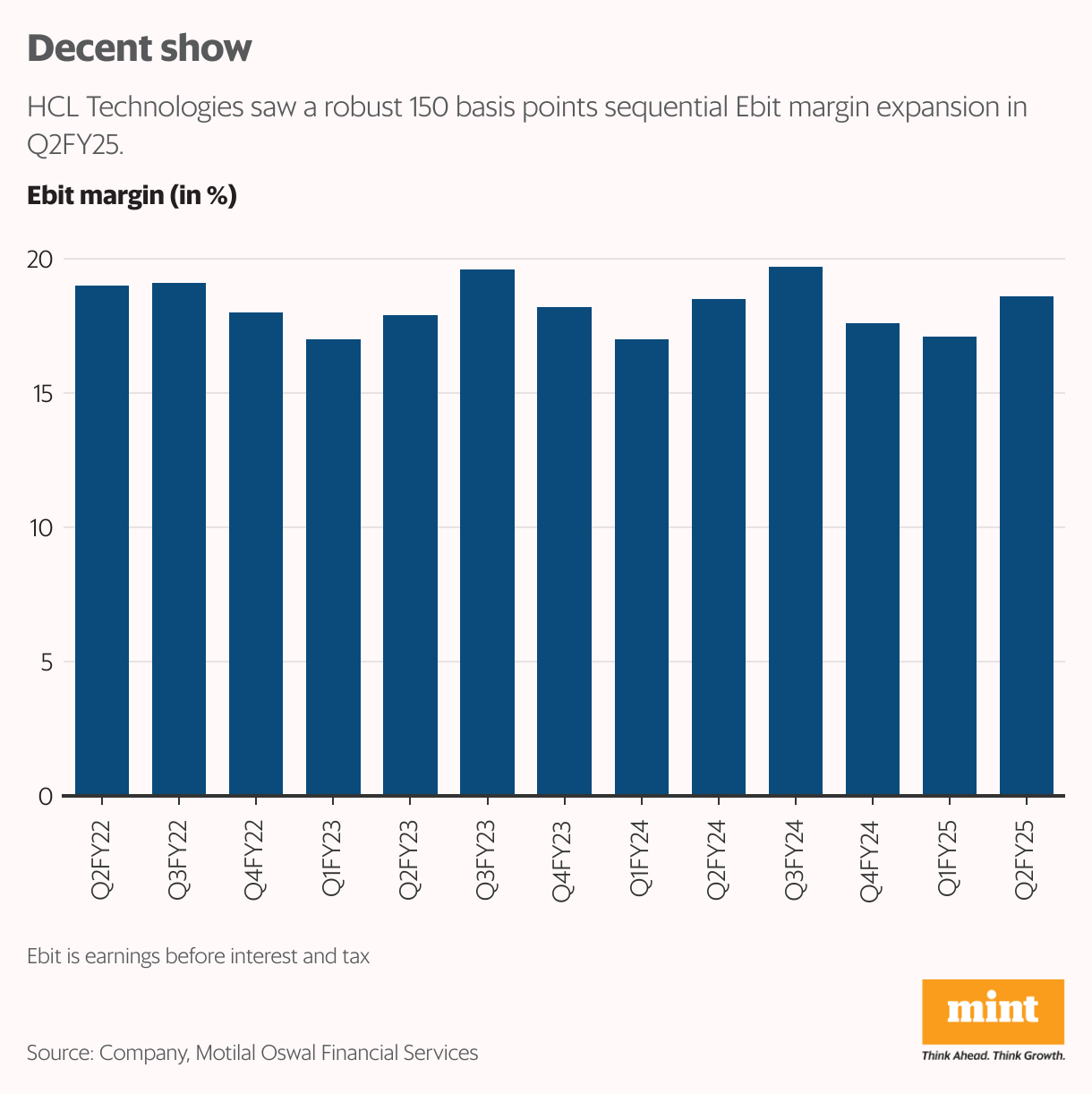

MUMBAI : HCL Technologies Ltd stock hit a new 52-week high of ₹1,882.75 on Tuesday in response to the decent September quarter (Q2FY25) earnings. Sequential constant currency (CC) revenue grew 1.6% ahead of Street’s 0.6% estimate.

Also, HCL raised the lower-end of FY25 revenue growth guidance to 3.5% from 3% earlier. Its FY25 CC revenue growth guidance now stands at 3.5-5% year-on-year. Earnings before interest and tax (Ebit) margin at 18.6%, rose 150 basis points sequentially, beating consensus expectations of 18%.

HCL retained FY25 margin guidance of 18-19%, which factors in the impact of wage hikes.

Also Read: Why Infosys and HCLTech have the longest running CEOs

Turbulence ahead

The earnings beat was largely driven by the products and platforms business, which grew 1.4% sequentially in a seasonally weak quarter. Here, revenue growth was aided by higher perpetual licence sales that could normalize in Q3FY25, said Kotak Institutional Equities report on 14 October. Perpetual licensing is when a software vendor charges a one-time fee for selling a licence to the user.

Total contract value of HCL’s new deal wins rose 13% sequentially to $2.2 billion in Q2FY25, but was down year-on-year due to the Verizon deal in base year. The visibility of mega deal-driven revenue is weak for FY26 currently and requires wins in H2FY25, added Kotak.

The December quarter is seasonally weak for the sector due to furloughs. But client-specific challenges in manufacturing (automotive & aerospace), could offset some positives for HCL such as strong Q3 seasonality of its software division and benefits from recently completed Zeenea acquisition, said HDFC Securities report on 15 October.

Also Read: Infosys resorted to this old hack to stem its top-level exodus: Promotions

Valuation concerns

Importantly, the stock’s steep rally of 25% in 2024, ahead of the Nifty IT’s returns, means valuations are now expensive. At FY26 price-to-earnings, the HCL stock is trading at a multiple of 26x, showed Bloomberg data. Valuations are now almost at par with giants Tata Consultancy Services Ltd and Infosys Ltd. In the past, HCL has traded at a discount to these competitors. In fact, HCL is now trading at a 5% discount to the Nifty IT versus a 20% discount historically, according to HDFC Securities.

From hereon, there is not much scope for a significant re-rating, especially considering that the sector is still grappling with demand blues. The HCL management is seeing green shoots of improvement in discretionary IT spending, but remains cautious of global macroeconomic environment and geopolitical tensions. So, it is not extrapolating incremental demand strength beyond December quarter and expects furloughs to be similar to last year.