Hyundai IPO: Parent’s Kia stake a sore spot

- Hyundai’s parent company holds a 34% stake in Kia Motors, which raises a question of conflict of interest. Also, the Sebi regulation mandates 25% non-promoter holding. So, there is a technical overhang of further supply of shares as the promoter stake in Hyundai India post the OFS will be 82.5%.

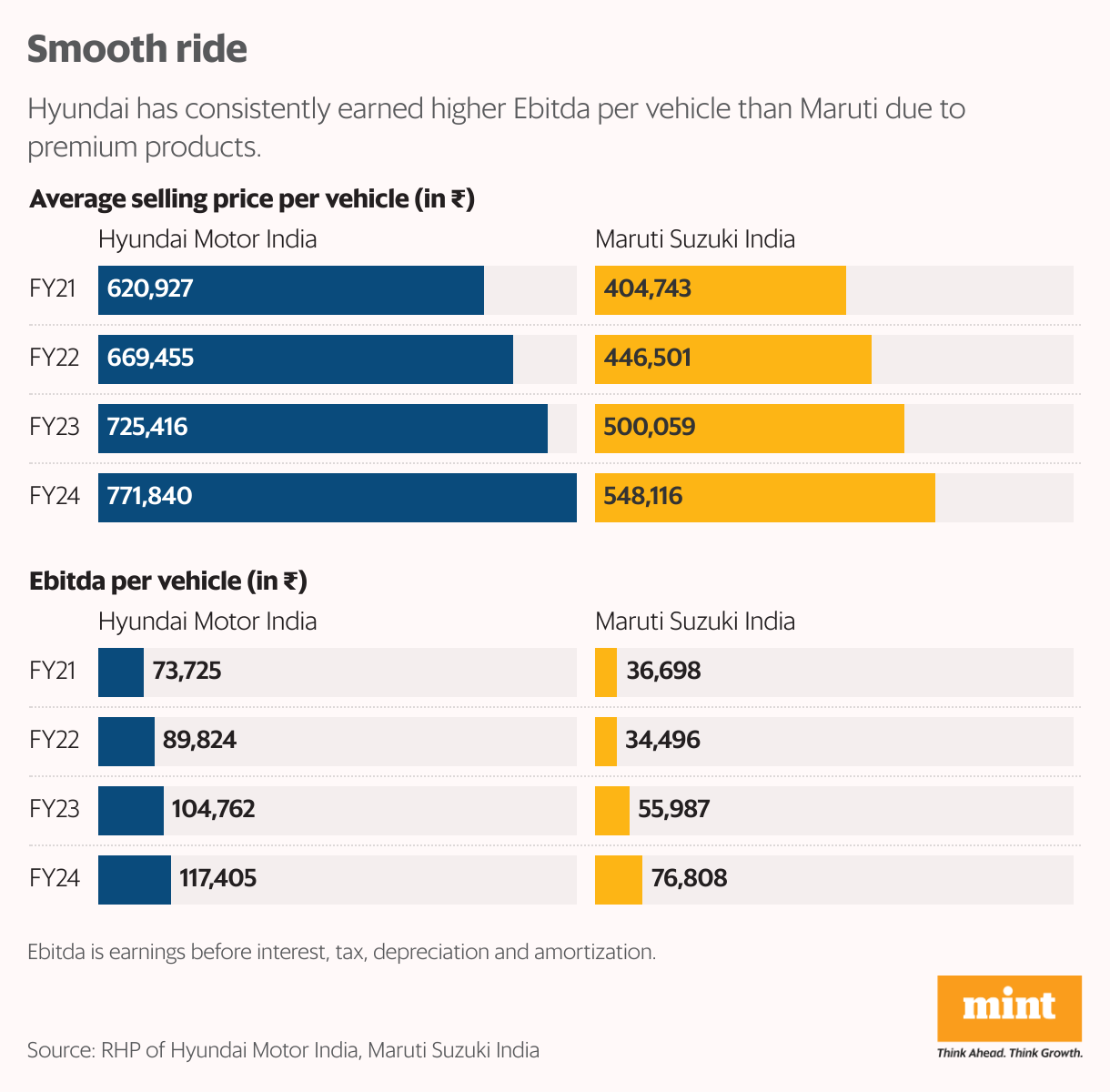

Hyundai Motor India Ltd, the largest passenger vehicle company in India after Maruti Suzuki India Ltd, will list itself on the bourses. While they are the top two companies, it must be also noted that the gap between both is huge. For instance, Hyundai’s total sales volume at 7.8 lakh during FY24 was only 36% of vehicles sold by Maruti.

Sure, both the companies have seen a 13% sales volume CAGR during the two years to FY24. But the catch is that Hyundai’s average selling price during FY24 at ₹7.7 lakh is much higher than Maruti’s ₹5.5 lakh, indicating a premium product portfolio. Hyundai has a strong presence in the fast-growing, higher-priced SUVs with taller ride height. Its SUV sales-to-total sales has been higher for the last two fiscal years at 63% and 52% versus the industry’s 51% and 41%, respectively. Unsurprisingly, Hyundai earned a higher Ebitda per vehicle of ₹1,17,000 in FY24 vis-à-vis ₹77,000 of Maruti. With more profit per vehicle, Hyundai’s profit growth should be faster than its top rival.

Hyundai’s South Korean parent company is selling 17.5% of its stake at a price band of ₹1,865-1,960 in an offer for sale (OFS). At the upper end, it is valued at ₹1.6 trillion and is cheaper than Maruti both in terms of EV/Ebitda at 17x versus 21x and a price-to-earnings multiple of 26x versus 30x based on FY24 financials.

Hyundai’s return-on-net-worth (RoNW) at 57% for FY24 appears much higher than that of Maruti at 17%. This is because the Korean parent took out cash from Hyundai via a special dividend of ₹10,800 crore in FY24 whereas Maruti holds cash of nearly ₹50,000 crore.

While post listing, Hyundai India could account for about 40% of the parent’s market capitalization, Maruti’s mcap is more than twice its parent’s mcap. Hyundai’s Korean parent company is quoting at a price-to-earnings multiple of about 6x based on 2023 financials vis-à-vis 11x of Maruti’s parent company.

Read more: India Inc’s increasingly important growth driver: The subsidiaries

But such comparisons hardly help in making investment decisions as valuation is a function of expected long-term macro and company level growth rates. So, investors keen to participate in India and specifically in Hyundai’s growth story may avoid buying the parent company’s shares even if they are cheaper. As such, the entry barriers for car imports in India are high with import duties of 60% for vehicles costing less than $40,000 and 100% for vehicles costing above that. Hence, the passenger vehicle industry has been dominated by a few local companies like Maruti, Hyundai and Tata Motors.

One challenge for all auto companies is to constantly keep up with the changes in technology across conventional and non-conventional vehicles besides having a good network for sales & service. While Hyundai paid royalty at nearly 3% of its FY24 revenue, it is in line with Maruti and other MNCs.

Hyundai’s parent company also holds a 34% stake in Kia Motors, which raises a question of conflict of interest. Also, the Sebi regulation mandates 25% non-promoter holding. So, there is a technical overhang of further supply of shares as the promoter stake in Hyundai India post the OFS will be 82.5%. These factors may cap huge near-term gains on listing the shares.