ICICI Prudential: Street is pinning hopes on margin recovery

margin improved by 124 basis points (bps) year-on-year and 150 bps sequentially to 22.7%. (Image: Pixabay)")

- While annualized premium equivalent (APE) shrank in Q4FY25, ICICI Prudential’s margin recovery and disciplined cost control offered some relief. With valuations now attractive, the Street is watching closely for sustained gains in profitability.

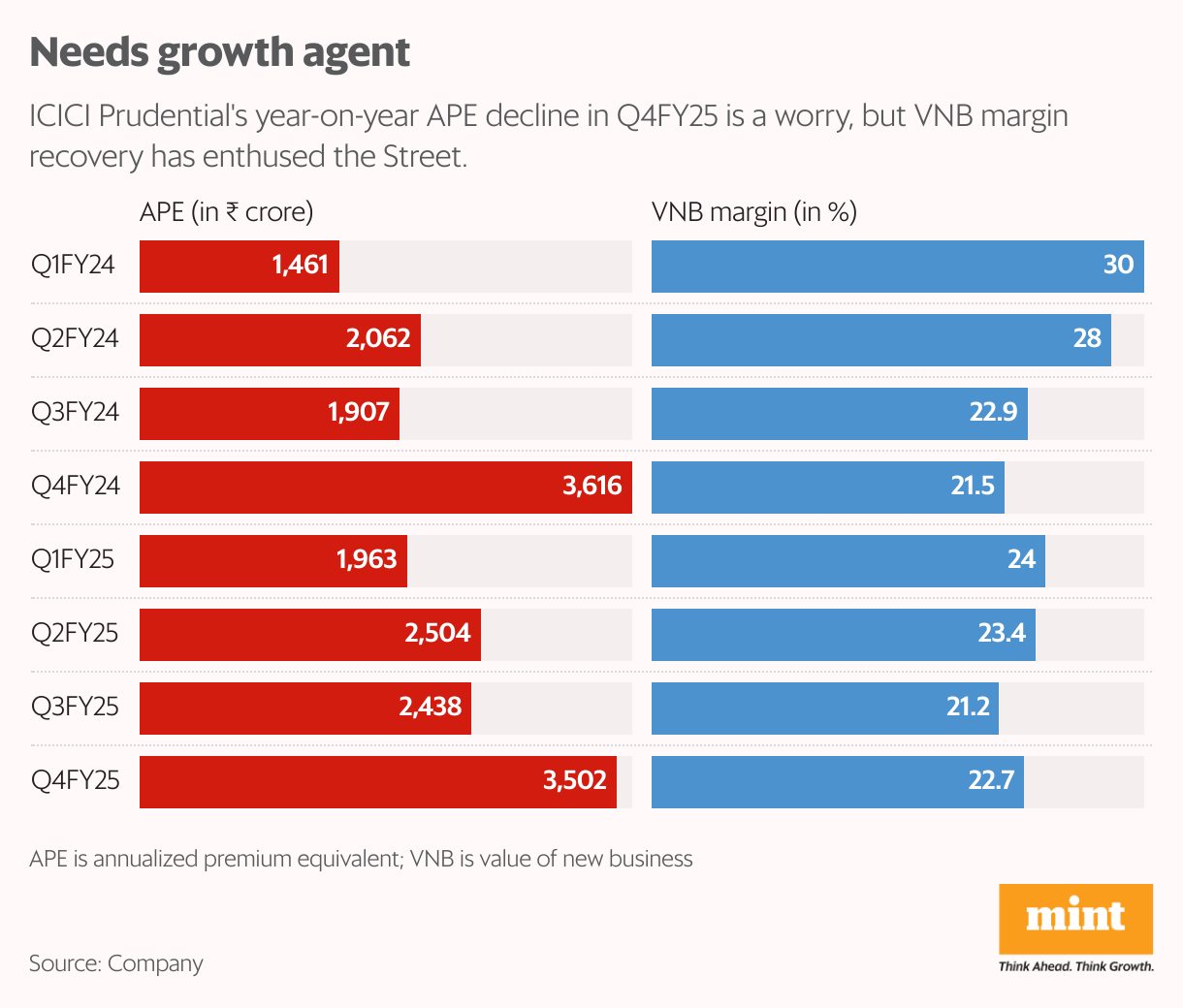

Shares of ICICI Prudential Life Insurance Co. Ltd rose nearly 3% to ₹583 apiece on Wednesday, reacting to its March quarter (Q4FY25) results. The performance, however, was lacklustre, with the annualized premium equivalent (APE) falling 3.2% year-on-year to ₹3,502 crore.

The stock’s gains were likely driven by two factors: margin expansion and attractive valuation. The value of new business (VNB) margin improved by 124 basis points (bps) year-on-year and 150 bps sequentially to 22.7%, perhaps helped by a better product mix.

The share of low-margin unit-linked insurance plans (ULIPs) declined, although they still accounted for 43% of APE. ULIPs saw strong demand earlier in the year amid a booming stock market but faced headwinds from weak equity performance in Q4.

Read this | LIC stock needs APE growth more than a steep valuation discount to private peers

Another driver of margin improvement was likely the revival in premium income from traditional non-linked savings policies, which rose 13.8% year-on-year. The company launched a non-participating guaranteed income product, ‘GIFT Select’, in Q4. That said, the full-year VNB margin contracted 180 bps to 22.8% in FY25 despite the rebound witnessed in Q4.

Coming to valuation, a popular tool for life insurance companies is the embedded value (EV) or modified form of book value that includes present value of future profits from existing business. ICICI Prudential’s EV per share is up from ₹294 in FY24 to ₹332 in FY25, but the stock price has dropped sharply from the peak of ₹796.8 apiece on 1 October. Thus, the price-to-EV multiple has shrunk from 2.4x at the peak to 1.8x based on the company’s FY25 reported EV.

The EV keeps growing unless there is a loss, which is rare in the life insurance business unless there is a pandemic or a calamity. This means that the price-to-EV multiple will look even cheaper based on FY26 forecast.

The company reported 15% APE growth in FY25, while operating expenses rose by a modest 13%, indicating that costs have been kept under control. On the earnings call, the management refrained from providing any guidance on APE growth for FY26, citing volatile market conditions. However, the conpany remains confident of outpacing the industry’s expected 13–15% growth over the medium term. It aims to grow VNB faster than APE, though it has not set a specific margin target.

Improving VNB margin remains a key focus for the insurer, through corrective pricing. One such example is the revised pricing in protection or term insurance segment. The segment accounted for just 15% of total APE for FY25, but is the most profitable one with the highest margin. The margin slipped to 55% in FY25 from 70% in FY24, but should move higher as the company increases the pricing of group term insurance plans.

ICICI Prudential has been walking away from businesses with negative/low margins. So, VNB growth would largely be a function of product mix. Hence, the endeavor would be to improve product level margins by extending the tenure, increasing sum assured, providing higher attachment/ riders, etc.

Also read | Insurers may get to sell related non-insurance value added products and services but not MFs

The Street would like to see VNB growth improve from 6.4% in FY25 even though valuation remains cheap. Just like the price-to-book value multiple is evaluated based on RoE, with higher RoE deserving a higher multiple, the price-to-embedded value multiple has to be seen in the context of return on embedded value (RoEV).

ICICI Prudential’s FY25 RoEV is healthy at 13.1%. Even after factoring an RoEV of 14.8%, Yes Securities has a target price of ₹650 for the stock based on 1.5x FY27 P/EV.