Indian cement stocks become dearer than some global peers

Despite elevated valuations, India's cement sector faces challenges with poor earnings and a 5%-6% price drop in FY25. Optimism stems from expected government infrastructure spending and a return of pricing discipline.

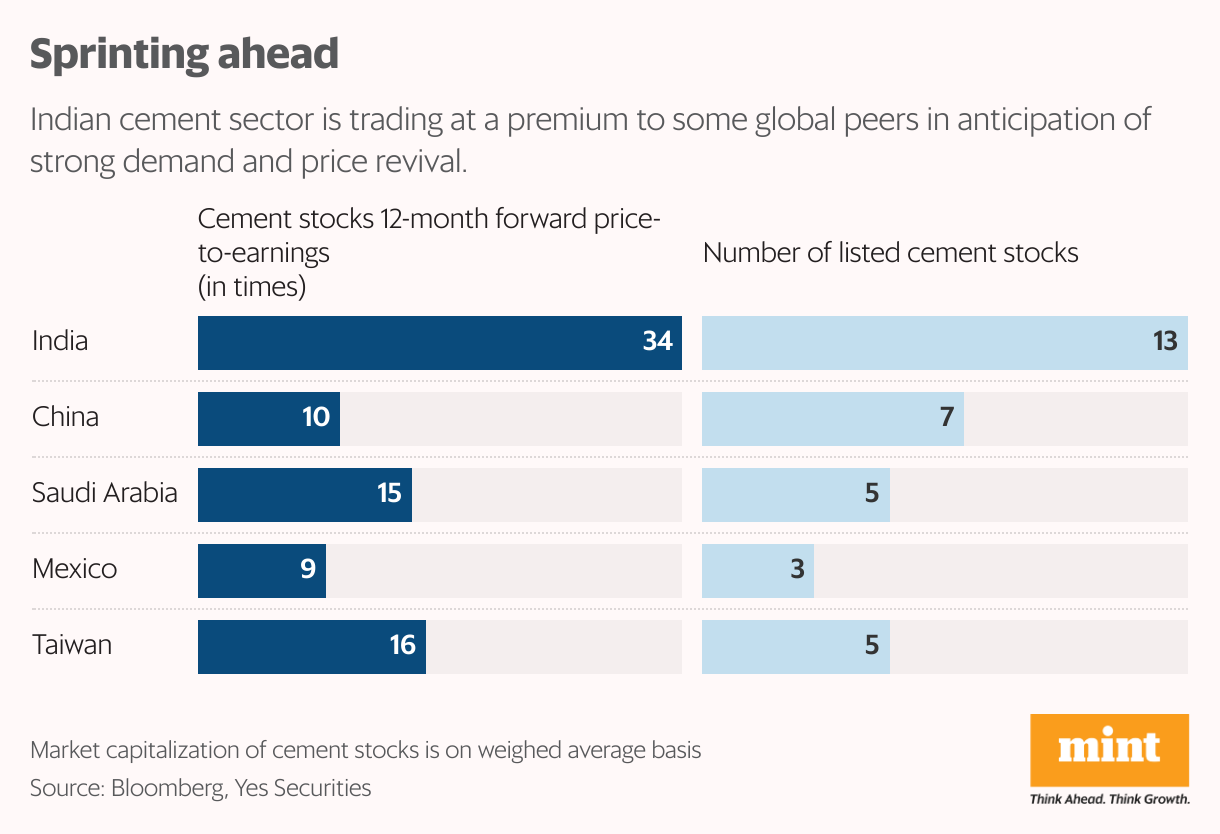

India’s cement sector is not a cheap bet on an absolute or relative basis. It trades at a one-year forward price-to-earnings multiple of 34x – a steep premium to some global counterparts.

The reading is higher than the sector's long-term average. The problem is that stocks of Indian cement makers have elevated valuation multiples despite subdued earnings.

In fact, the Indian cement sector has seen large downgrades to consensus Ebitda and earnings per share estimates every year for the past 10 years, says Kotak Institutional Equities.

So, what is keeping valuations lofty? Two key narratives seem to fuel optimism.

A pick-up in government spending on infrastructure and allied activities in FY26 after a muted FY25 due to state and general elections would buoy cement demand. Additionally, the home building segment is also likely to push demand after real estate launches were weak in FY25 due to delayed approvals.

Also Read | Cost pinch is coming for cement companies in Q1

Secondly, pricing discipline, which has been absent lately amid an intensifying fight for market share, will return. Consolidation in the sector, with larger companies acquiring smaller ones, is said to be at its fag end now. So, as demand outpaces supply, cement prices would recover and thus, realisations and profitability.

Latest company management commentaries are upbeat, with demand and pricing outlook poised to pick up in the seasonally strong second-half of the year. But the dent in prices has been severe.

Price drop

According to India Ratings and Research, cement prices fell 5%-6% in FY25, the sharpest annual drop in the past 20 years. The most pronounced price contraction was in south India due to oversupply, followed by the eastern region, it said in a note dated 17 June.

Also Read | Is the cement sector consolidation at its fag end?

So, repairing realisations may not be easy if demand fails to improve as anticipated amid the recent spate of capacity addition. This would also keep the sector's utilisation levels capped.

The return ratios have been poor. Sectors such as cement with a low fixed asset turnover ratio (long-term average of 1x) and mediocre financial returns with return on equity/cash return on capital invested modestly higher than cost of equity/weighted average cost of capital should not have a very high multiple, as per Kotak.

On a one-year forward EV/Ebitda basis, the sector trades at a multiple of 21x, higher than the long-term average of 16x. Clearly, unless one of these narratives materialises and leads to earnings upgrades, valuations don’t seem justified.