Markets

Markets

IT companies' revenue revival seen delayed to FY26

Summary

- Muted discretionary IT spending amid a weak global macro-economic situation and slower client decision-making have also made it difficult to predict a revenue recovery for the IT sector

For Indian information technology (IT) companies, the narrative has barely changed. FY24 was a forgettable year at best because the revenue recovery expectations failed to materialize.

There is little to suggest a marked improvement in FY25. Muted discretionary IT spending amid a weak global macro-economic situation is also seen as the villain in FY25.

Focus on cost-efficiency programmes and slower client decision-making have also made it difficult to predict the IT sector's revenue recovery.

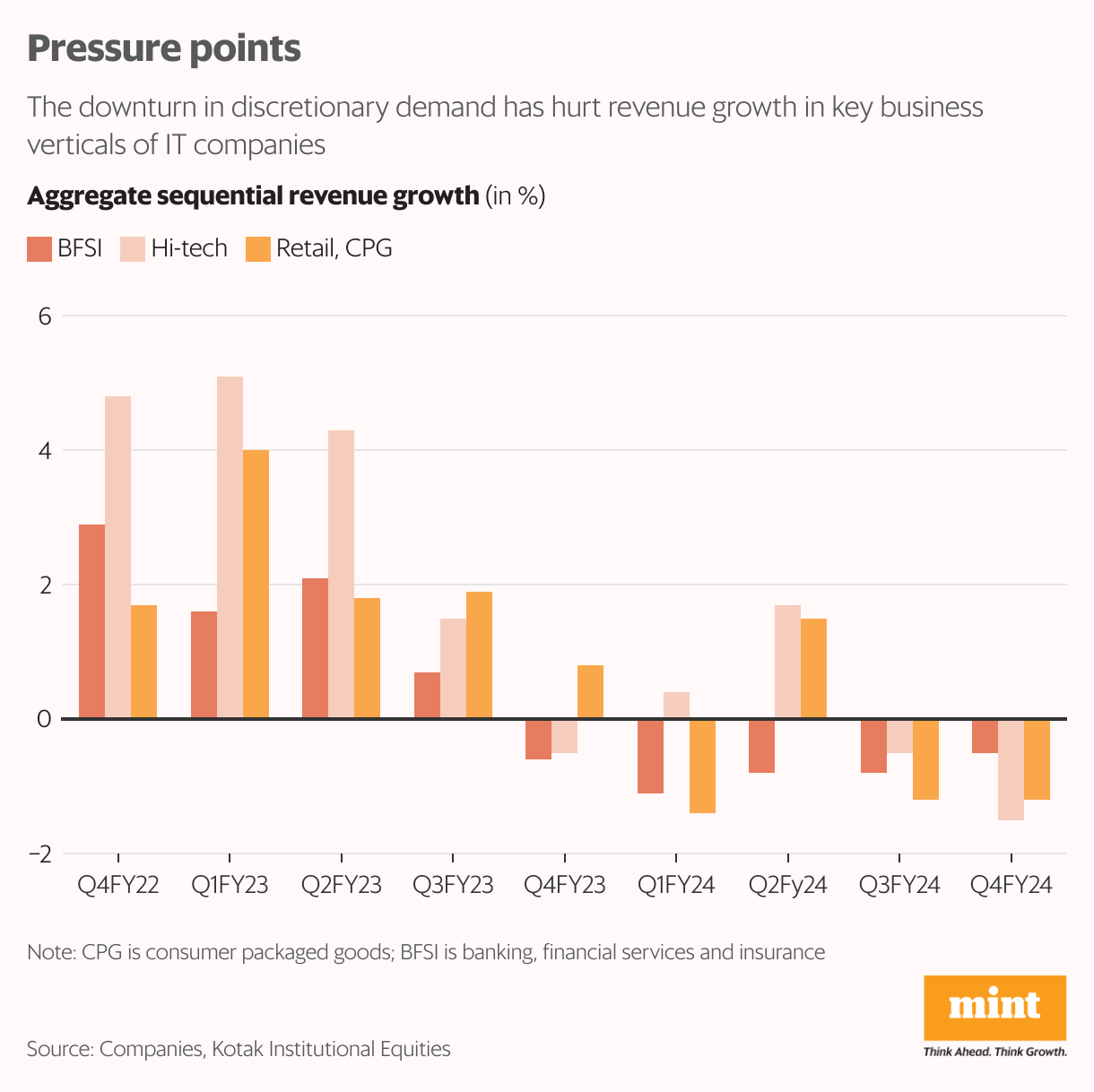

While deal wins in the March quarter (Q4FY24) were robust, this does not help much in giving direction to investors. The conversion or translation of deal wins into revenue growth still lags meaningfully. Also, the crucial verticals of BFSI, hi-tech, and retail continue to be sluggish. Among key geographies, developed markets, the US, and Europe remained under pressure last quarter.

The technology spending projections of six large US banks in 2024 does not appear inspiring vis-à-vis 2023.“Spending growth in Mar-24 quarter on a year-on-yearbasis is reasonably good overall, considering the macro environment," said a report by Kotak Institutional Equities.

“However, CY2024 Bloomberg projections for tech spending indicates considerable deceleration ingrowth compared to CY2023 across Citi, Wells Fargo, Goldman Sachs and Morgan Stanley, with JPMbeing the outlier with strong growth acceleration," added the report.

Also Read: Wipro, Infosys March quarter results paint gloomy outlook for FY25

Growth rates in CY24 do not look encouraging, especially with CY23 being a bitter year for IndianIT despite largely healthy growth in tech spends last year.

As such, the cautious mood is captured well in FY25 guidance, which fell short of analysts’ expectations, thus failing to rekindle lost investor confidence.

To give a quick recap, tier-1 IT companyInfosys Ltd guided forconstant currency revenue year-on-year growth of1-3% in FY25.

Peer HCL Technologies Ltd saw robust Q4 exit, but guided for 3-5% growth in FY25. While the tier-2 pack continued to fare better than tier-1 on revenue growth in Q4FY24, concerns on outlook persists. For instance,Coforge Ltd’s gave a broad FY25 revenue growth guidance of at best 10%, without any specific numbers.Cyient Ltd cut its expectation to high single-digit growth from double-digit.

Lowersub-contracting costs due to muted demand and better utilization aided Q4FY24 margins. True, there are levers for margin expansion in FY25 with the ongoing focus of IT companies on cost rationalization. But that has not helped contain earnings downgrades.Putting everything together, a significant turnaround in revenue growth is not expected before FY26.

“Most of the companies are banking on growth in H2FY25E thereby pushing growth expectation to FY26E. Consequently, we have cut our Revenue and earnings per share estimates by 4% & 3% for FY25E in large cap and by 3% & 7% for FY25E in midcaps," said IDBI Capital Markets report.

Comfort for investors

Amid this gloom, can anything bring comfort to investors? Interest rate cuts by the US Federal Reserve can offer some respite. Expectations are that a loose monetary policy would come as a boost to clients in the BFSI sector giving them confidence about macro stability and inflation trajectory. This, in turn, wouldbring back discretionary IT demand as clients become more willing to spend on technology projects and upgrading.

The European Central Bank recently cut the key policy rate by 25 basis points. Additionally, the USpresidentialelections, likely towards the end of 2024, are worth tracking, mainly for any changes in H1-B visa rules.

Meanwhile, so far in 2024, the Nifty IT index has declined by nearly 3%, lagging the 7% gain in the Nifty 50. In effect, valuation multiples of tier-1 and tier-2 companies have further cooled-off. But with lingering uncertainties, is that enticing enough?

Also Read: Mint Explainer: Why we need a new competition law for big tech companies