IT earnings: One eye on FY26 guidance, the other on midcaps

")

Summary

- As Indian IT firms brace for another muted quarter, all eyes are on FY26 guidance amid weak discretionary spending and trade headwinds. With tier-1 companies under pressure, midcaps could offer relative resilience—but not without risks.

Investors in Indian IT stocks have stepped into FY26 on an anxious note. The latest blow: newly announced reciprocal tariffs by the US, which threaten to further derail the sector’s already-stalled revenue growth recovery. Companies continue to battle the same headwinds—cautious clients, muted discretionary tech spending, and prolonged deal cycles—all of which are slowing revenue conversion and triggering another wave of earnings downgrades.

“We once again cut revenue and EPS estimates (after cuts in March 2025) for our coverage universe, baking in the reciprocal tariffs imposed by the US against many countries," said a Kotak Institutional Equities report on 4 April.

Read this | Can India dodge Trump’s trade tariff bullet? Depends on the sector and trade pact talks

A worry is that FY26 could possibly end up being worse than FY25 for some of the companies. The brokerage has lowered its FY2025-27 revenue growth estimates by 1.2–3.4% and Ebit margin projections by 10–50 basis points, resulting in a 1.6–5.8% cut in earnings per share forecasts.

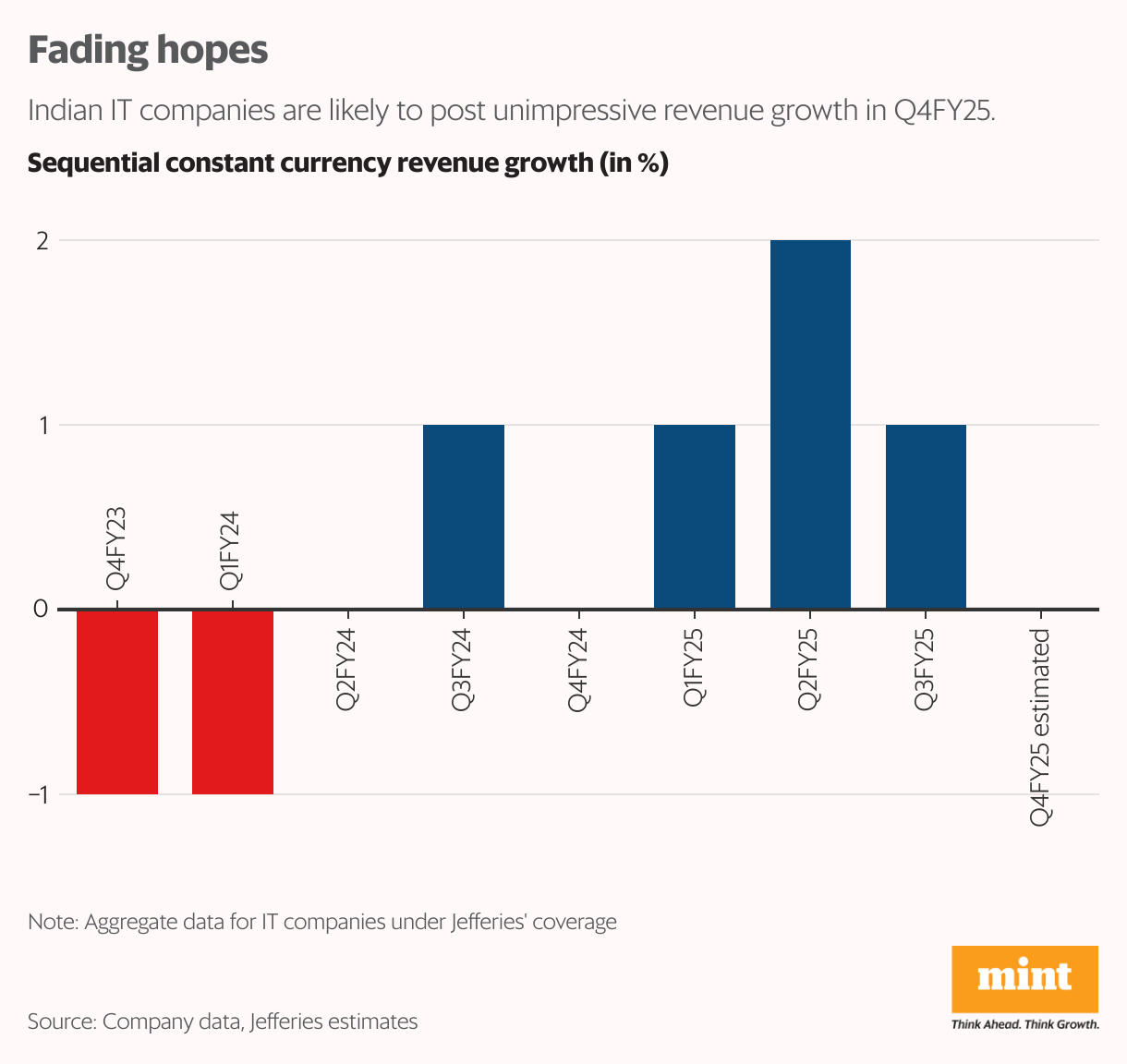

Tier-1 IT companies are likely to report a lacklustre Q4FY25, with revenues either flat or declining sequentially due to firm-specific challenges amid the broader slowdown.

Tata Consultancy Services Ltd (TCS), for instance, has been impacted by the Bharat Sanchar Nigam Ltd (BSNL) ramp-down, while HCL Technologies is dealing with seasonal softness in its software segment. By contrast, select mid-tier firms may outshine their larger peers.

“We expect aggregate revenues for our coverage to decline by -0.4% quarter-on-quarter constant currency (cc) (+4.3% year-on-year cc), " said a Jefferies India report dated 31 March.

"Among our coverage, we expect high divergence in growth, as we expect top-6 IT companies' revenue to grow at -1% to +0.3% QoQ cc, and +2.6% to +11% QoQ cc for mid-sized IT companies," it added.

In the mid-cap pack, L&T Technology Services is expected to lead growth, aided by seasonality in the SWC vertical and the Intelliswift acquisition. Persistent Systems Ltd and Coforge Ltd would likely report decent sequential revenue growth aided by ramp-up of earlier deals. But Tata Elxsi Ltd, Birlasoft Ltd, and Sonata Software Technology could be the laggards due to company-specific problems.

Read this | Emerging markets brace for impact of Trump's tariff wrath this earnings season

But what matters more than the upcoming March quarter (Q4FY25) results is FY26 revenue growth guidance demand outlook.

Latest management commentary from global IT giants—Accenture, Capgemini, and Cognizant—signal no material change in the demand environment compared to the same time last year with weak discretionary spending. Indian IT companies may opt to be conservative on FY26 guidance due to higher near-term uncertainty and lack of mega deal-driven revenues. But if some companies choose to defer giving guidance it could be an additional sentiment dampener.

Margins are expected to be a mixed bag, hinging on factors such as salary hikes, large-deal ramps, currency tailwinds, and easing supply-side constraints. Deal activity will likely remain focused on cost optimization and takeout initiatives, though win momentum may stay moderate.

Investors will also be watching closely for signs of sustained recovery in BFSI and any rebound in communication and manufacturing verticals—especially the auto segment, which remains weak.

Meanwhile, the Nifty IT index has declined by a whopping 23% in this calendar year so far, compared to the 5% decline in the Nifty50 index. Consequently, valuations have moderated further, but there could be more pain ahead.

Also read | Manufacturing PMI rebounds—but don’t celebrate just yet

A muted Q3FY25 followed by subdued Q4FY25 could disrupt the year-on-year revenue growth trajectory for the sector, which had been improving only lately. A BoB Capital Markets report points out that consensus estimates have now moved back from a 7-8% CC FY26 revenue growth to a low to mid-single digit number and this estimate is at risk of more deceleration.