JK Cement beats peers on a critical parameter, but watch out for party poopers

JK Cement's grey cement volumes surged 15% in Q4 FY25, driven by strategic capacity additions. The company anticipates doubling capacity by FY30, with improved cost management leading to a 35% rise in Q4 EBITDA. However, pricing pressures and competition pose challenges in certain segments.

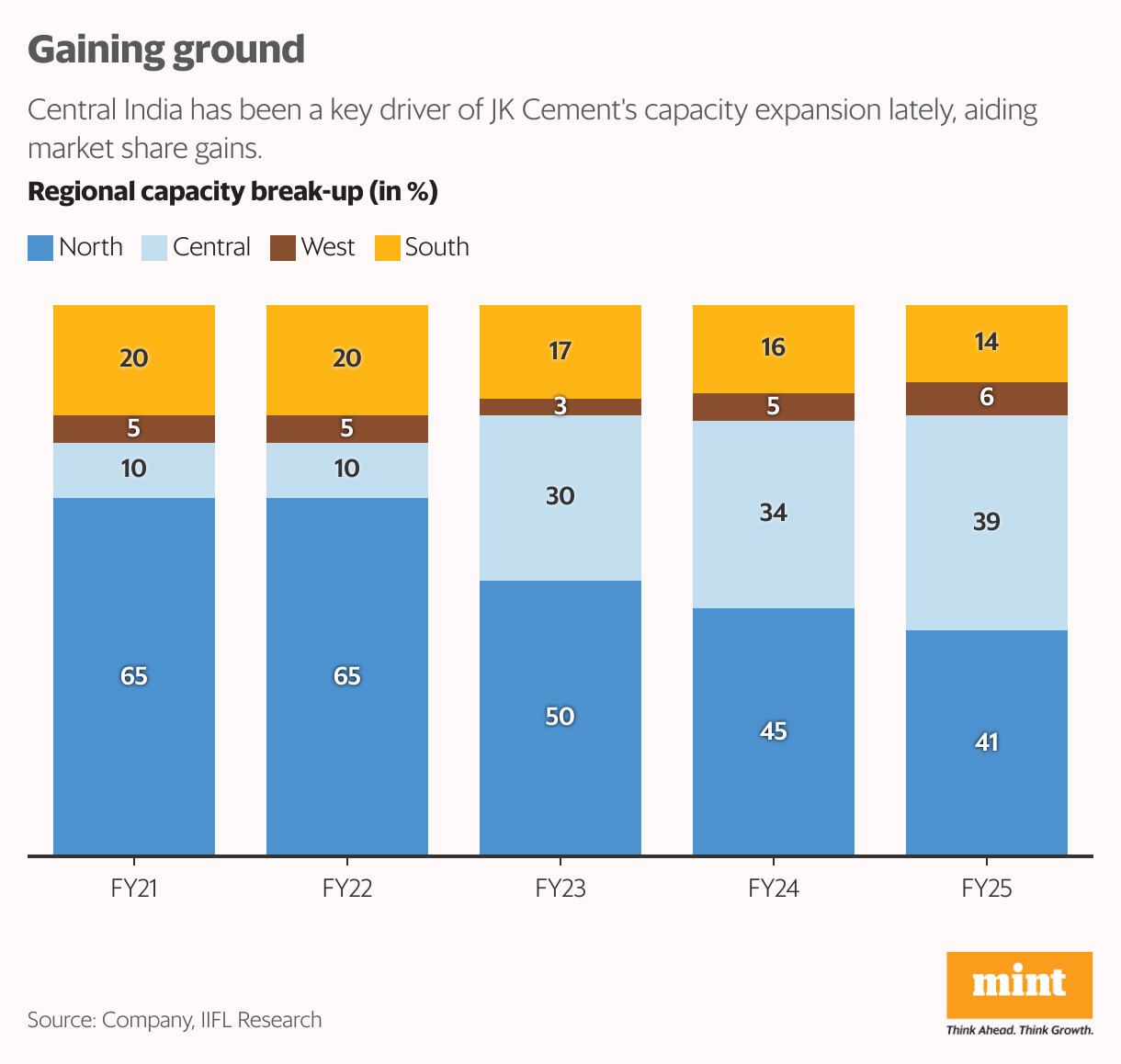

JK Cement Ltd’s timely capacity additions and solid execution are giving it an edge over midcap peers that are battling muted volume growth after the recent wave of industry consolidation.

JK’s grey cement volumes rose 15% year-on-year in the March quarter (Q4 of FY25) to 5.39 million tonnes (mt). This implies market share gains in north and central India as peers operating in these areas reported volume growth in the 3-8% range, Emkay Global Financial Services said in a report dated 25 May. JK also outpaced the industry’s estimated volume growth of 4-5% in Q4.

Government spending and pent-up demand in its key market of central India, where it is adding capacity, buoyed volume growth in the last quarter. The ramp-up of a new grinding unit in Prayagraj (Uttar Pradesh), commissioned in FY25, also contributed. The company projects grey cement volumes will increase to 20 mt in FY26 from about 18 mt in FY25.

Grey cement capacity is likely to double to 50 mtpa by FY30 from the current 24.34 mtpa, which brings long-term volume growth visibility. To achieve this, brownfield and greenfield expansion is likely at Jaisalmer, Muddapur, Panna and Odisha.

Also Read | A catalyst for Ramco Cements stock is set to play out. But is that enough?

Expansion of the clinker unit at Panna and grinding units at Panna, Hamirpur and Prayagraj are on track and expected to be commissioned by December. The grinding unit in Bihar, a market it recently entered, would be complete by December.

“After adding 15 mt capacity in the last six years, JK is now targeting 20-25 mt in the next five years," said IIFL Securities Ltd. “Given the aggressive capacity addition plans – the capex intensity is likely to sustain at ₹1,800-2,000 crore per annum."

JK incurred capital expenditure of ₹1,720 crore in FY25 and has guided for ₹1,800-2,000 crore capex in FY26.

Among the best

On operating costs, the fuel consumption cost/kcal dropped to ₹1.41 in Q4 from ₹1.50 in Q3 and ₹1.80 in Q4 of FY24. Operating cost is likely to reduce by ₹150-200/tonne over the next two-three years, backed by various initiatives. JK achieved an average cost reduction of ₹40/tonne in FY25 and targets incremental savings of ₹25/tonne in FY26.

Robust volumes and easing cost pressures led to better-than-expected profitability. Standalone Q4 Ebitda rose 35% year-on-year to ₹7,364 crore. According to ICICI Securities, JK’s grey cement Ebitda/tonne – at about ₹1,210 in Q4 – was among the best in the industry. Additionally, the turnaround in its UAE subsidiary bodes well for profitability outlook.

Also Read | UltraTech Cement set for higher volumes, tighter grip on costs

JK’s shares hit a new 52-week high of ₹5,645 on Monday. A sharp rally of 33% in the past one year has meant an expensive valuation multiple of 16x FY26 estimated EV/Ebitda, Bloomberg data showed.

While outperformance versus peers can help sustain rich valuations, steep near-term upsides may be curbed. Further re-rating hereon would depend on the progress of the next leg of expansion.

Moreover, there is discomfort on prices. Cement prices in the southern region are up by 5-7% and up by 1% in the northern and central regions versus the average Q4 price, the management said. Price and demand trends in central India are key for JK as it expects the region to be a major volume growth enabler.

JK remains in the red in the paints venture with an operating loss of ₹45 crore in FY25. Amid elevated competition, it offers higher dealer discounts than its peers. An Ebitda breakeven for the paints business is likely in FY27.

Also Read | Is the cement sector consolidation at its fag end?

Headwinds are expected in the white cement and putty business due to rising competition, leading to subdued volumes in these categories in FY26, the management said.