Markets

Markets

KEC International's prospects shine, but margin recovery remains crucial

Summary

- Ebitda margin has been gradually improving and strategic project bidding is in place, but sustained margin recovery is essential for future stability.

KEC International Ltd's steep 55% rally in the stock over the past year has been vindicated by the positive business outlook shared by its management at the recent RP Goenka group investor conference. In fact, the capital goods company’s shares are hovering close to all-time highs.

Interestingly, despite this impressive rally, KEC has underperformed the 74% gain of the BSE Capital Goods index and trades at a discount to the sector valuation. The company’s one-year forward price-to-earnings multiple, based on Bloomberg consensus, is 28x versus 35x for the sectoral index.

KEC’s relatively low Ebitda (earnings before interest, taxes, depreciation, and amortization) margin and high net working capital requirements could explain the stock's lagged performance. The company’s management is actively addressing these issues by selectively bidding for new projects.

Read This: Can BHEL reclaim its crown?

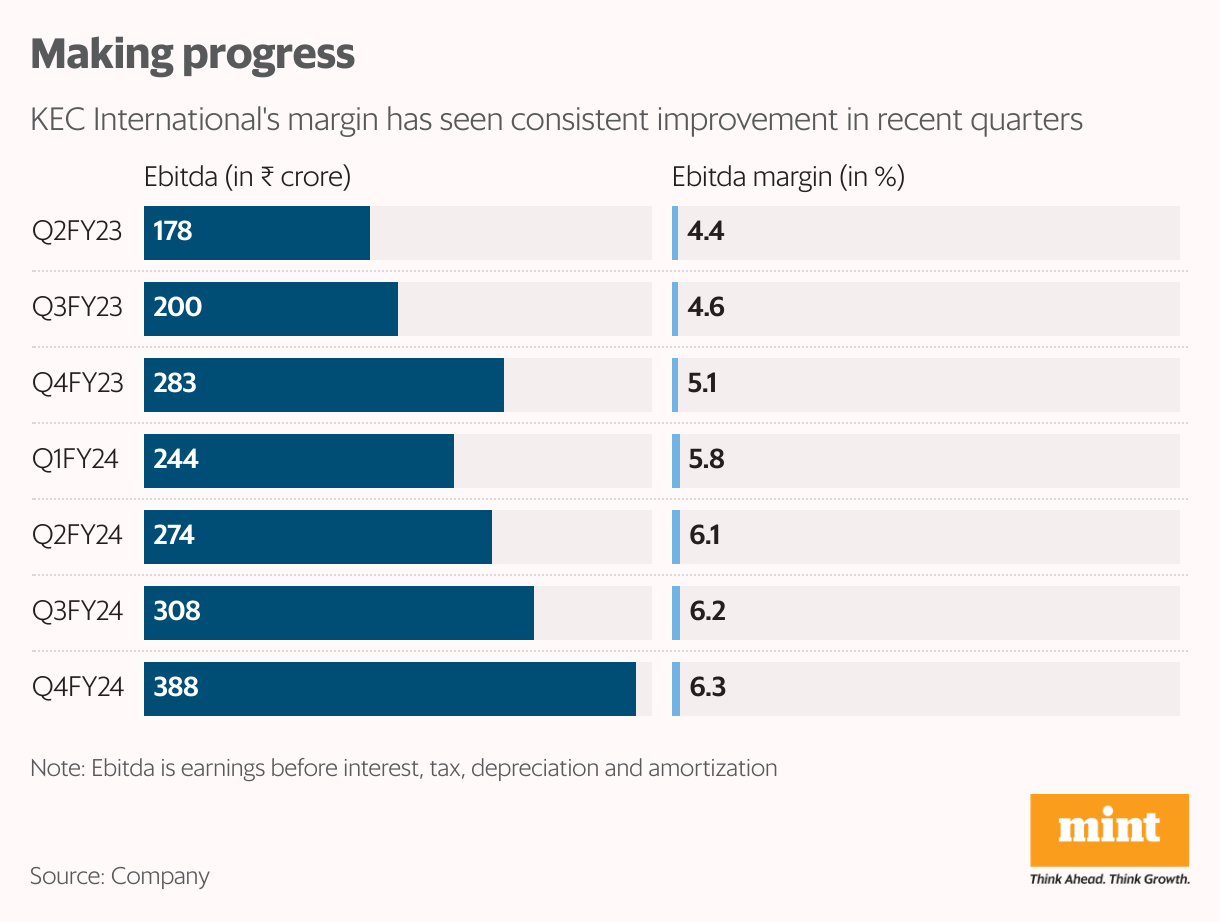

The efforts are bearing fruit, with Ebitda margin consistently improving over the past six quarters from 4.4% in Q2FY23 to 6.3% in Q4FY24. The management expects the margin to improve to 7.5% in FY25 and reach 9-10% by FY26.

Transmission & Distribution: Growth driver

Further Ebitda margin expansion is expected to be driven by the transmission and distribution (T&D) segment, due to lower competitive intensity in higher-value projects.

The T&D segment accounts for nearly 60% of the order book plus L1 – the most preferred bidder based on the tenders submitted – while civil works, the second-largest segment, contributes 28%. The overall order book, including L1 positions, stands at ₹38,000 crore, almost double the FY24 sales, ensuring revenue visibility for the next two years.

Notably, KEC’s net working capital days reduced to 112 as of March from a peak of 133 days in September. Lower working capital requirements helped keep net debt almost flat at ₹5,000 crore, despite a 15% year-on-year revenue growth to ₹19,914 crore in FY24. The management is targeting another 15% revenue growth for FY25 and does not expect net debt to rise. With Ebitda improving, investors can expect KEC’s high net debt-to-Ebitda ratio to drop from the high level of 4.2 times at March-end.

And This: NTPC powers ahead with plans for expansion, renewable energy business

In India, the power sector is set for promising growth with transmission infrastructure planned for major renewable energy potential zones to support the target of achieving 500 GW of non-fossil fuel power by 2030. While this represents an opportunity for Power Grid Corp. of India Ltd, on-the-ground execution companies such as KEC would also benefit.

To be sure, how margin recovery pans out in the coming years remains key. Further, the non-T&D segment has been a sore spot mainly due to execution challenges and weakness in the railways segment. Investors must closely watch these variables as they can provide further triggers to the stock.