Markets

Markets

LIC stock is available at a discount. So why aren’t investors piling in?

Summary

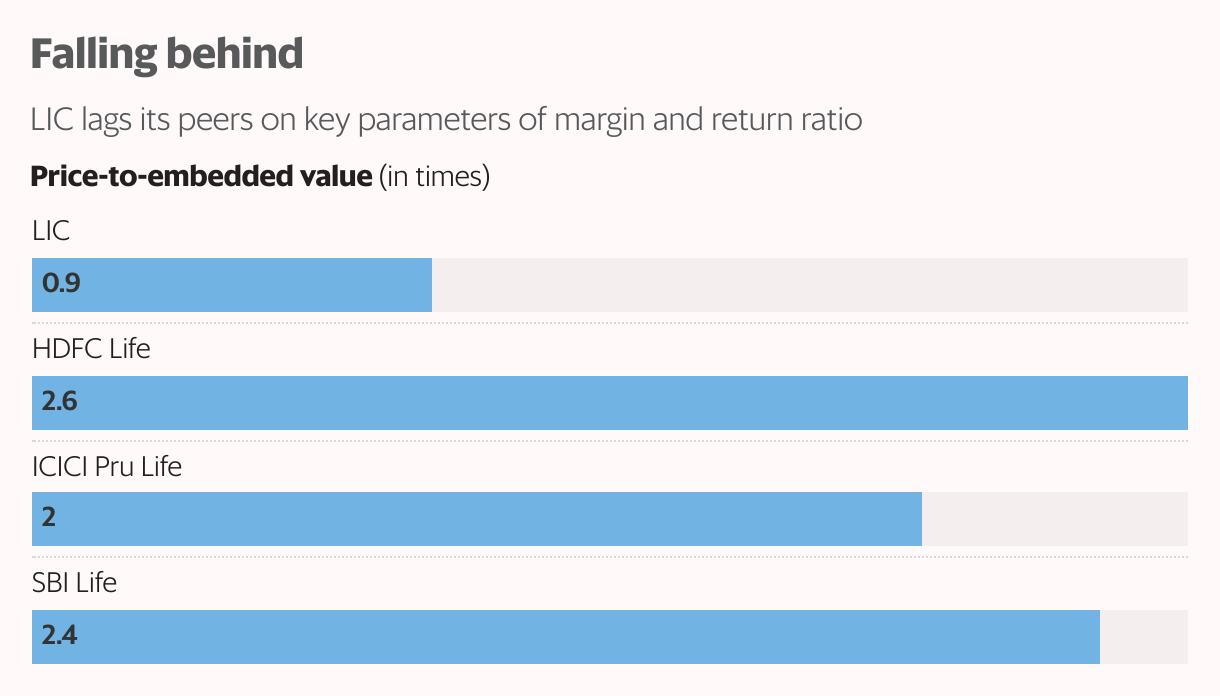

- LIC has a market-capitalisation-to-embedded-value of just 0.9 as against 2 to 2.6 for HDFC Life Insurance, ICICI Prudential Life Insurance, and SBI Life Insurance. While there is scope for the valuation discount to narrow, the process could be gradual at best.

An impressive highlight of Life Insurance Corporation of India’s (LIC’s) FY24 performance was the big 330 basis points (bps) jump in the individual segment net value of new business (VNB) margin to 18.8%, even as the segment’s annualised premium equivalent (APE) remained almost flat at ₹38,433 crore.

This was possible because non-participating business as a percentage of total individual APE doubled year-on-year to 18% in FY24. For insurance companies, APE is a measure of sales growth and VNB a profitability parameter. Non-participating policies are more profitable for life insurance companies, as these policy holders do not enjoy any benefits in terms of dividend/bonus from the company’s profits.

Also read: Opportunity cost vs premium loss: When to surrender your policies

The far-superior profitability of non-participating policies is evident from its net VNB margin of 60.7% as against 9.4% for participating policies during FY24. Notably, participating policies still accounted for 82% of the individual business, which meant at an aggregate level, the gain in VNB margin was only 60 bps to 16.8%.

The other reason for the diluted growth in aggregate VNB was a sharp deterioration in the profitability of the group insurance business. During the earnings call, concerns were raised about LIC’s decision to increase the benefits payable under group schemes despite its dominant position in the business with a 72% market share. Consequently, the VNB margin of group schemes crashed from 17.6% to 12.6%.

Attractive valuation

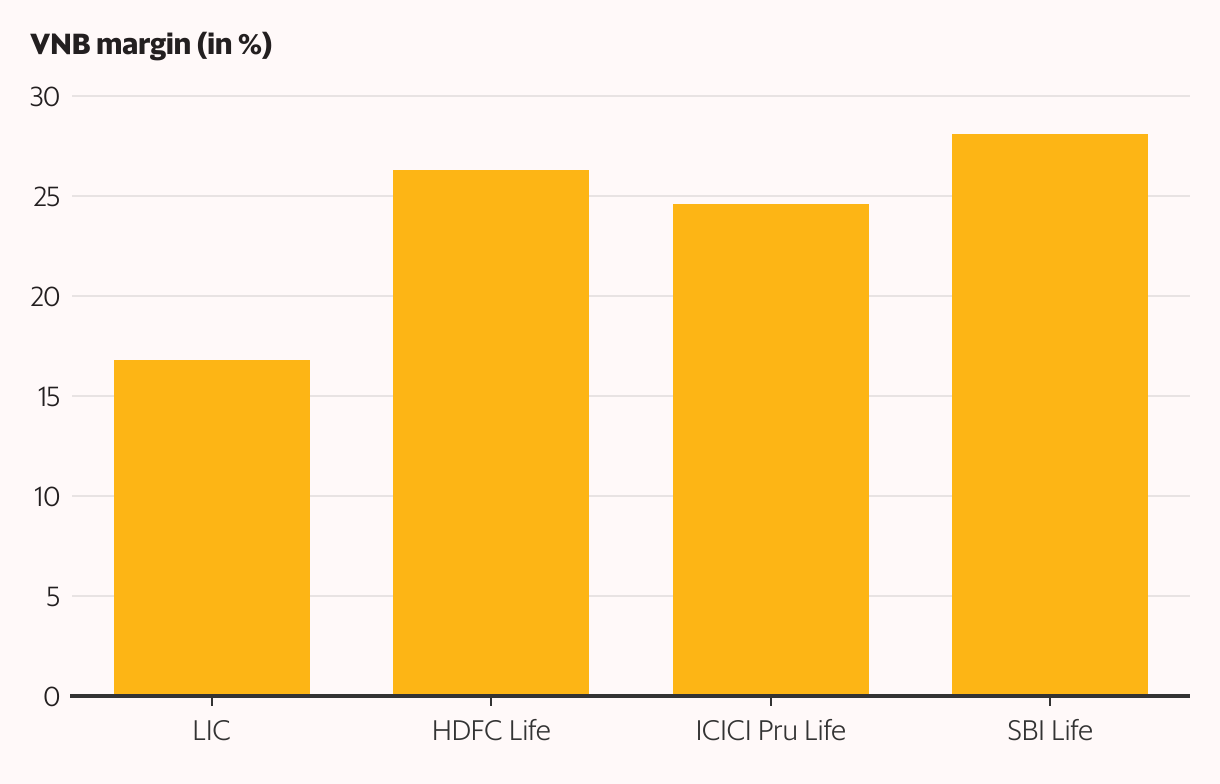

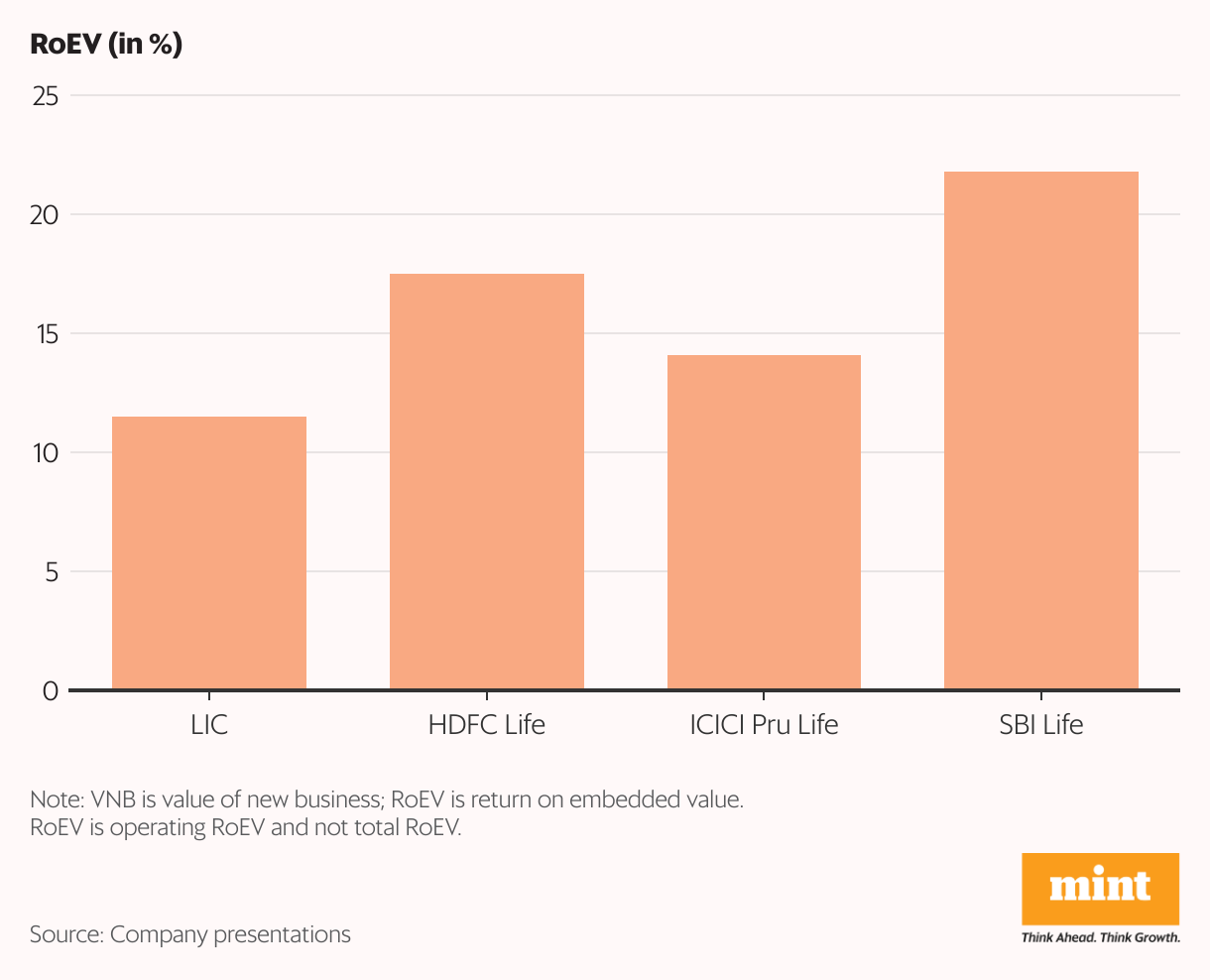

LIC’s overall VNB margin is much lower than those of its key rivals such as HDFC Life Insurance Co (26%), ICICI Prudential Life Insurance Co (25%) and SBI Life Insurance Co (28%). LIC also has the lowest operating return on embedded value (RoEV) among peers at 11.5%, against 17.5% for HDFC Life Insurance, 14.1% for ICICI Prudential Life Insurance and 21.8% for SBI Life Insurance.

LIC therefore has a market-capitalisation-to-embedded-value (P/EV) of just 0.9x as against 2 to 2.6 for the other three companies. RoEV for insurance companies can be seen as similar to RoE for companies. Going by this, LIC’s valuation discount seems rather steep, notwithstanding the lower VNB margin and RoEV.

Also read: Take loan to avoid tax: A new loophole in insurance town

With a gradual recovery in margin in FY24, aided by the shift towards more profitable products, there is scope for the valuation discount to narrow, but this process could be gradual at best.

Note that agents account for over 90% of LIC’s new business premium but less than 30% at private companies. LIC is keen on increasing its focus on bancassurance, but it’s unlikely to be material in the context of overall mix in the near future and might increase from 4% to 5-6%.

Govt gets more time to sell shares

Management alleviated some concerns during the earnings call, clarifying the company may only enter the health-insurance segment of general insurance as there are synergies in life insurance and health insurance. They added, though, that the move is still at a preliminary stage. Management also ruled out a merger with any public-sector general insurance company, but said LIC could pick up a strategic stake in a general insurance company.

Also read: Why ‘regular pay’ is better for life insurance premiums

The other overhang for LIC’s stock was the additional supply of shares owing to a likely sale by the government of India that would reduce its stake from 96.5% to 90% or less. However, Sebi clarified this month it would give the government another three years to reduce its shareholding.

Unfortunately for investors, LIC’s stock has gained just 7% since it was listed almost two years ago. Despite the undemanding valuation, investors don’t seem to be in a hurry to buy the stock, going by the subdued post-results reaction on Tuesday.