Markets

Markets

L&T Tech has outlined an ambitious growth plan. But it's off to a slow start.

services.")

Summary

- L&T Tech aims to be a top ER&D services company with $2 billion revenue. The focus is on mobility, sustainability, and tech, but lacks a timeline. Analysts see potential but caution against ambitious targets and slow deal conversions.

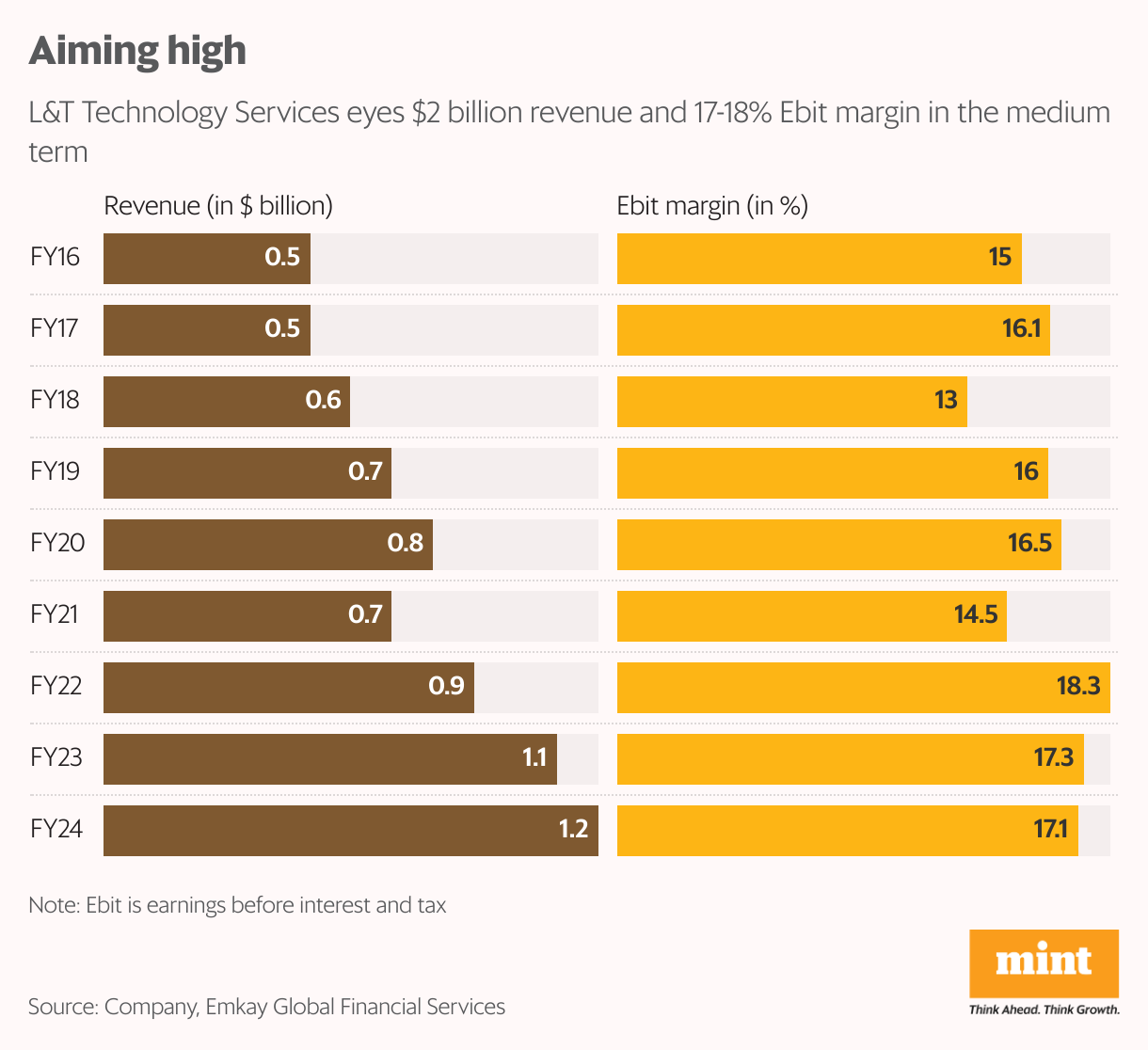

L&T Technology Services Ltd’s revamped growth strategy has the Street excited, leading to a nearly 5% rise in the stock over the past two days. The tier-2 IT company aims to be among the top five engineering, research and development (ER&D) services companies globally, and is targeting $2 billion in revenue in the medium-term.

At its Investors Day meet on Tuesday, L&T Tech’s management laid out its ‘Go deeper to Scale’ strategy with a focus on three key business segments: mobility, sustainability, and tech. It outlined a plan for each of these segments to achieve $1 billion in revenue eventually—three times their current revenue—with some margin improvement.

That said, the company has not specified a timeline for these ambitions, which could dampen investors’ confidence.

The company’s targeting a margin of 17-18% on its earnings before interest and tax (Ebit) by improving employee productivity, securing more overseas contracts, hiring more freshers, and optimising costs. But for 2024-25, L&T Tech has projected an ebit margin of 16%, down from 17.1% in 2023-24.

Are these measures enough for a turnaround in the stock’s performance? (Over the past year, the stock—LTTS—has gained about 32%, but has underperformed the Nifty IT index, which has given about 38% returns in the same span.)

The answer lies in the bold pace of execution planned. According toMotilal Oswal Financial Services, L&T Tech’s new strategy may not alter its growth path in the short term, but it could open up new avenues for growth, especially in hitherto weak areas such as mobility—a fast-growing segment for its peers.

Too ambitious?

Against this backdrop, the company’s renewed strategy is a step in the right direction. However, the targets seem ambitious.

L&T Tech’s management is gung-ho on ER&D services and expects the onset of a rate-cut cycle in the US to boost demand in this space. India-based sourcing of global ER&D spending grew at a 16% compound annual growth rate over 2014-23 and would likely grow at a 17-22% CAGR over 2023-30, the management said.

But the company has some catching up to do before it can benefit from the potential rise in ER&D services demand. “LTTS’ progress in scaling accounts in the $20-30 million range has been middling despite a broad set of capabilities. In comparison, Indian pure-play ERD peers have at least one $75 million+ account," Kotak Institutional Equities said in a report.

The broking firm stated that while L&T Tech’s strategy has the key tenets to scale the business at a healthy rate, the extent of these aspirations might be aggressive.

Also, given the ongoing slowdown in the US and the European Union on discretionary spending, it is better to temper expectations of a sharp revival in the ER&D budgets of clients, according to analysts.

L&T Tech’s management said that while the company’s near-term large deal pipeline is double that of last year’s, deal conversions were taking longer than usual to become confirmed orders.

A slow start

L&T Tech expects to exit 2024-25 with revenue of $1.5 billion, up from $1.16 billion in FY24. For this, the management reiterated its focus on inorganic growth, stating that it would explore mergers and acquisitions in the $50-150 million range in three key areas—mobility (in the EU region), software services, and medtech (both in North America regions).

So far this financial year, L&T Tech has not announced any acquisition plans. Since M&A is a crucial component in the company’s plan for FY25 revenue growth, the timing and scale of acquisitions is worth tracking.

But a dull start to FY25 raises the risk of earnings downgrades if revenue growth fails to meet expectations. “For FY25, the company has guided for organic growth of 8-10% year-on-year in constant currency, which we believe is aggressive given weak start and a steep ask (4.2% - 5.4% CQGR)," PhillipCapital (India) said in a report.

What is also not sitting well with analysts is the stock’s expensive valuation, which is higher than its large-cap peers. At FY26 price-to-earnings, the stock is trading at multiple of around 38 times, showed Bloomberg data. This is despite underwhelming returns so far in 2024: the L&T Tech stock has risen 9% compared to the Nifty IT index’s 19% gain.