Lower crude brings relief to Mahanagar Gas amid falling APM gas allocation

")

Any sudden government decision to cut APM gas allocation or a reversal in crude price trend, may hurt sentiments.

Mahanagar Gas Ltd (MGL) just got some cushion amid the falling share of cheaper administeredprice mechanism (APM) gas in its overall sourcing mix. Three things should help here: increase in price of compressed natural gas (CNG) and domestic piped natural gas, sustained volume growth, and lower crude oil prices.

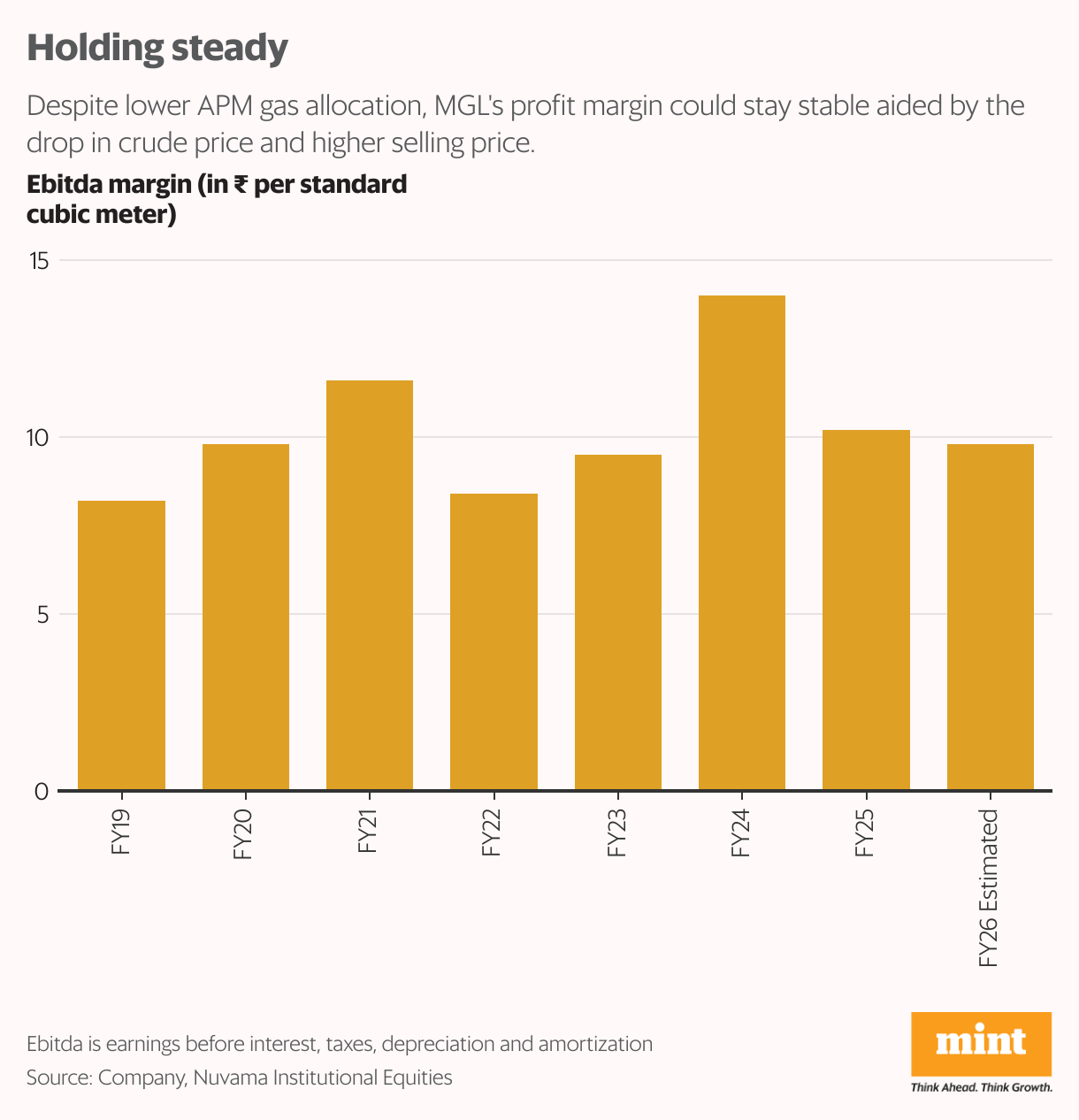

MGL’s cost of gas jumped in FY25 as the share of APM gas dropped to 56% from 70% in FY24. Thus, its Ebitdaper scm (standard cubic meter) fell sharply to ₹10.2 from ₹13.9 in FY24.At its recent investor meet, the city gas distributor guided for 10%+ volume growth over the next 2-3 years, along with Ebitda of ₹9-11 per scm despite lower APM allocation, down to 39% in FY26 so far. Ebitda is short for earnings before interest, taxes, depreciation, and amortization.

The APM gas is priced at 10% of domestic crude basket with a cap of $6.75 per mmBtu (million British thermal units), whichis being replaced by new wells gas (NWG), priced at 12.5% of domestic crude basket with no cap. The management projects 7-10% of APM gas to shift to NWG each year.

Also Read: Blue Star faces the heat in Q1 from a milder summer season

The lower gas allocation should be offset by the drop in crude price with Brent crude now at about $65 per barrel, down from average of $75.8 per barrel in Q4FY25 and over $80 a year ago. Motilal Oswal Financial Services projects Brent prices to average $65 per barrel in FY26 and FY27. The broking firm expects MGL’s Ebitda margin to cross ₹10 per scm, backed by the sales price revision done in April and declining crude.

Positive outlook

Volume growth is another trigger. FY25 volume growth was about 12%, up from 6% in FY24 led byindustrial and commercial (I/C) consumersand can sustain here. I/Cconsumers form15% of FY25 volumes andgrew 24% owing to addition of few large customers. I/C is expected to grow 20% in FY26.

The automotive segment, forming 70% of volumes, grew 11% in FY25. MGL plans to open 80 new CNG stations in FY26, taking the total to about 550.

Also Read: Realty firms are on a high after last year’s spending spree to buy land

Amid improving outlook, MGL’s shares have gained about 11% so far in 2025. The stock trades at 13x FY26 estimated earnings, shows Bloomberg data. While valuations don’t appear steep, any sudden government decision to cut APM gas allocation or a reversal in crude price trend, may hurt sentiments. Nuvama Research has retained its ‘Reduce’ rating on sector multiples’ de-rating due to ad-hoc government policies causing uncertainty (similar to OMCs, which trade at a sizeable discount).